谷歌团队在平安金融中心

It’s time to rethink the relationship of the large tech companies to financial services.

现在该重新考虑大型科技公司与金融服务之间的关系了。

I used to echo that the Western tech companies are powering the “attention economy”, pulling in users into a walled garden that competes for hours in the day with other tech companies. The core of this thesis is that media consumption is the hook into people’s lives, and that addiction to techno-dopamine keeps them engaged with Instagram, WhatsApp, and TikTok. Thus Trump swiping at TikTok in a nationalist zeal.

我曾经回覆过,西方科技公司正在推动“ 注意力经济 ”发展,将用户吸引到一个围墙的花园中,该花园每天与其他科技公司竞争数小时。 本论文的核心是媒体消费是人们生活的纽带,对技术多巴胺的沉迷使他们与Instagram,WhatsApp和TikTok保持联系。 因此,特朗普以民族主义的热情朝着提克·托克(TikTok)轻扫。

The core chart for the thesis is below:

论文的核心图表如下:

It says, welcome to your smartphone for 4 hours a day. More than television consumption, and certainly far beyond radio or gaming.

它说,欢迎您每天使用智能手机4个小时。 不仅是电视消费,而且肯定超出广播或游戏。

But I don’t think it’s right anymore to say that media is how we drive commerce. It is a drug in the mix for sure, but it is not the main cocktail.

但是我认为说媒体是我们推动贸易的方式已经不对了。 当然,它是一种药物,但不是主要的鸡尾酒。

What we learn from Eastern tech companies is that finance can be at the center. Is Tencent, the owner of TikTok (almost banned in the US) and WeChat (banned in India), a video gaming company, a social media company, or a payments company? Or a digital yuen company? Or a national blockchain infrastructure provider company? The same can be asked of Alibaba, Tencent’s alpha competitor.

我们从东方科技公司那里了解到,金融可以成为中心。 是TikTok(几乎在美国被禁止)和WeChat(在印度被禁止)的所有者腾讯,视频游戏公司,社交媒体公司或支付公司吗? 还是数字园公司? 还是国家区块链基础设施提供商公司? 腾讯的阿尔法竞争对手阿里巴巴也可以问同样的问题。

While there are plenty of drugs — in the form of games and speculation — in these Eastern systems, they are underpinned by other themes. Those can be commerce and shopping, like Amazon. Or they can be payments, like Square and PayPal. Or micro-credit and business lending, like Affirm. And further, they can be wrapped into the geopolitical narrative of de-dollarization that has now become a necessary survival tactic. See below for an example of Russian/Chinese trade settlement decreasing form 90% USD-based settlement in 2015 to <50% by 2020. The CBDC efforts we see China exploring are reportedly part of the same economic logic.

在这些东方体系中,尽管有大量毒品(包括游戏和投机形式),但它们受到其他主题的支持。 这些可以是商业和购物,例如亚马逊。 或者它们可以是付款,例如Square和PayPal。 或者像Affirm这样的小额信贷和商业贷款。 而且,它们可以被纳入去美元化的地缘政治叙事中,而这已成为一种必要的生存策略。 参见下面的示例,俄罗斯/中国的贸易结算将从2015年基于90%的美元结算下降到2020年的<50%。据报道,我们看到中国在探索的CBDC努力是同一经济逻辑的一部分。

Ok. So it isn’t about “attention economy”, per se, if you can recreate the massive tech growth on the basis of financial and economic services. Maybe it is about platforms, data, and the network effects that accrue to building multi-sided marketplaces? As you have more users, you can generate demand for more products, which then attracts more service providers, which increases the quality of goods, and therefore attracts more users, and more adjacent products, until you are Amazon.

好。 因此,如果您可以在金融和经济服务的基础上重新创造大规模的技术增长,那么与“注意力经济”本身无关。 可能与建立多面市场有关的平台,数据和网络效应有关? 随着您拥有更多用户,您可以产生对更多产品的需求,从而吸引更多服务提供商,从而提高商品质量,从而吸引更多用户和更多相邻产品,直到您成为亚马逊。

For technology, this is often packaged as aggregation theory, canonized by Ben Thompson. The theory suggests that marketplaces will expand to all goods, period, and the hard problem is actually of curation rather than supply/demand generation. Note the illustration below implies cross-industry monopoly, with vertical integration having become far less important for industry players. Instead, the question is how you get some good into a platform, and then get it ranked higher by the algorithm. The answer for the ranking question is to get lots and lots of personal data, and then use machine learning to personalize at scale for things that people click on.

对于技术,这通常被打包为聚集理论 ,由Ben Thompson规范。 该理论表明,市场将扩展到所有商品,所有时期,而最棘手的问题实际上是策展而不是供应/需求产生。 请注意,以下插图暗示了跨行业的垄断,而垂直整合对于行业参与者而言已变得不那么重要。 相反,问题是如何在平台上获得一些好处,然后再通过算法将其排名更高。 排名问题的答案是获取大量个人数据,然后使用机器学习对人们单击的内容进行大规模个性化。

But it has always been hard for tech companies to aggregate financial services products, and deliver them to consumers. Instead, they have sold Fintech mobile apps.

但是,对于科技公司而言,聚合金融服务产品并将其交付给消费者一直很困难。 相反,他们出售了Fintech移动应用程序。

It is not a coincidence that Thompson’s stream of products looks like an iPhone home screen full of logos. If you do consider apps as products, Apple has been a finance re-seller for ages.

汤普森的产品流看起来像是充满徽标的iPhone主屏幕,这并非巧合。 如果您确实将应用程序视为产品,那么Apple多年来一直是金融经销商。

But when people say “Oh no, tech companies are getting into Finance!” they don’t really mean that there are a bunch of apps in an operating system. What they mean is that the app itself is manufactured by the tech company, and that this app is better than the one made by Wells Fargo or Goldman Sachs or whoever, and that rational people will stop banking with financial incumbents and start banking with Google.

但是,当人们说“哦,不,科技公司正在涉足金融业!” 它们并不是真的意味着操作系统中有很多应用程序。 他们的意思是,该应用程序本身是由科技公司生产的,并且比Wells Fargo或Goldman Sachs或其他任何人生产的应用程序都要好,而且理性的人会停止向金融业者提供银行服务,而开始向Google提供银行服务。

What they really mean is when Google starts offering bank accounts through Google Pay, layering on top financial insights, budgeting tools, and payments functionality (click for source). Google becomes the bank to the consumer, and the actual depository institution becomes the extension of a core banking system into a licensing regime. Reminder, the core banking systems will also run on Google cloud and eventually be subsumed from underneath.

他们真正的意思是Google在开始通过Google Pay提供银行帐户时,将其置于最重要的财务见解,预算工具和付款功能之上(单击源代码) 。 Google成为消费者的银行,而实际的存款机构成为核心银行系统向许可制度的延伸。 提醒一下,核心银行系统也将在Google云上运行,并最终被包含在底层。

What they mean is when Apple puts down $100 million to buy Mobeewave, a company that turns any phone into a point of sale payments system, which can be turned into a native iPhone feature. Today, FIS and Fiserv are $50–100 billion market capitalization companies, while Apple and Google are each worth over $1.5 trillion. That’s a nice snack for Apple to digest and integrate. Hungry hungry hippo!

他们的意思是,当苹果斥资1亿美元收购Mobeewave时 ,该公司将任何手机转变为销售点支付系统,可以将其转变为本地iPhone功能。 如今,FIS和Fiserv的市值为500-1000亿美元,而Apple和Google的市值均超过1.5万亿美元。 对于苹果来说,这是一个很好的消化和整合的零食。 饿了饿河马!

You can extend this logic to when Amazon offers auto insurance, or when Facebook launches a digital currency, or when WhatsApp offers lending products, and so on. This isn’t just the curation problem of aggregation theory.

您可以将此逻辑扩展到亚马逊提供汽车保险,Facebook启动数字货币或WhatsApp提供贷款产品的时间等。 这不仅仅是聚集理论的策划问题。

This is the vertical integration of the financial industry into the tech industry value chain.

这是金融业与技术产业价值链的垂直整合。

我们对数字化偏好的重新定位 (A reorientation of our preferences to digital)

What I think is really going on with the tech companies actually has less and less to do with the tech companies themselves, or the platforms they’ve built. It has more to do with what is going on with us as a species, as humanity.

我认为与技术公司之间真正发生的事情实际上与技术公司本身或所构建平台的关系越来越少。 它与人类作为一个物种正在发生的事情更多有关。

We are shifting from the physical world to the digital one, and as we do this re-orientation, we are reformatting our brains and livelihood.

我们正在从物理世界转变为数字世界,并且随着这种重新定位,我们正在重新格式化我们的大脑和生计。

The transition from farm life to factory life wasn’t a walk in the park. It was not a ten year “innovation cycle”. It was a global grinder, throwing flesh and bone into industry by the millions. It built massive cities, melted down nations, and birthed two atrocious World Wars. And boy, did we industrialize!

从农场生活到工厂生活的转变并不是在公园里散步。 这不是十年的“创新周期”。 这是一个全球性的磨床,将成千上万的肉和骨头投入了工业。 它建造了庞大的城市,摧毁了各个国家,并诞生了两次残酷的世界大战。 和男孩,我们工业化了!

Look at what COVID has done to expectations of work, play, and commerce. We have been atomized into home offices behind a Zoom panopticon, turning this into the new normal.

查看COVID在工作,娱乐和商务方面的期望。 我们被雾化成Zoom Panopticon背后的家庭办公室,将其转变为新常态。

In this abstracted, virtual world, of course TikTok is a key political asset! It’s the collection of all 1980s malls turned into one giant robot superstore full of teenagers. This is where we hang out. This is where we transact. This is where we socialize. Why would you ever buy something anywhere else?

在这个抽象的虚拟世界中,TikTok当然是关键的政治资产! 这是1980年代所有购物中心的集合,变成了一个充满青少年的巨型机器人大型超市。 我们在这里闲逛。 这是我们进行交易的地方。 这是我们社交的地方。 你为什么要在其他地方买东西?

It is then no surprise that the technology sector has been completely dominating the rest of the S&P 500. At the end of last year, tech companies constituted 23% of all public market sectors, up from less than 10% in 1995. The next largest sector was at 14%.

因此,毫无疑问,科技行业已经完全统治了标普500指数的其余部分。 去年年底,科技公司占所有公共市场行业的23%,而1995年不到10% 。 第二大行业是14%。

This is happening not just because these companies have network effects or superior business models or cheaper ways of doing things, but because we are all turning into the types of people that ONLY shop from our phones, and ONLY order from Amazon, and get mad at anyone without a good mobile app.

之所以发生这种情况,不仅是因为这些公司具有网络效应,卓越的商业模式或廉价的做事方式,而且还因为我们都变成了只从我们的手机购物,仅从亚马逊订购并发火的人。没有良好的移动应用程序的任何人。

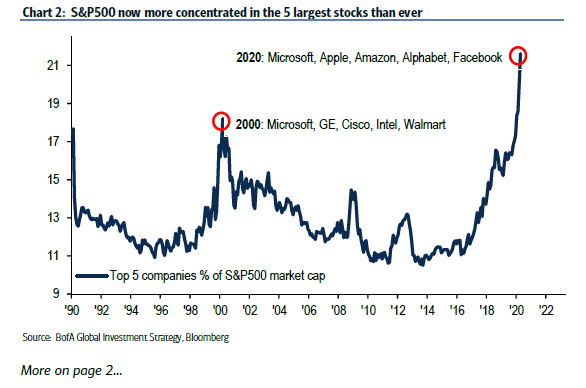

When you look at the concentration of marketcap share for the top 5 companies, it gets even more nuts. Well into 2020, Microsoft, Apple, Amazon, Alphabet, and Facebook now have 21% of the S&P500. That’s more than the entire Energy, Materials, Utilities, Real Estate, and Telecom sectors combined. Given the state of the world, we all continue to be in some form of Kafkaesque lock-down. This is turn reinforces the digital way of life.

当您查看排名前五位的公司的市值份额时, 就会发现更多的误解。 到2020年,微软,苹果,亚马逊,Alphabet和Facebook现在拥有标准普尔500指数的21%。 这超过了整个能源,材料,公用事业,房地产和电信行业的总和。 考虑到世界状况,我们所有人都继续处于某种形式的卡夫卡式禁闭状态。 从而强化了数字生活方式。

One last general point. We often hear the comment that finance is an institutional industry. However, our economy, and that of many other countries, is primarily driven by consumer spending as you can see below. For the US, continental Europe, the UK, Japan, India, and Brazil, retail spending is what disproportionately matters for GDP. Consumer preferences can re-form the wholesale value-chains that inevitably exist to serve them (e.g., a pension fund still has an end-client).

最后一点。 我们经常听到这样的评论,即金融是一个机构产业。 但是,我们的经济以及其他许多国家的经济主要由消费者支出驱动,如下所示。 对于美国,欧洲大陆,英国,日本,印度和巴西,零售支出对GDP的影响不成比例。 消费者的偏好可以重新形成为它们服务的批发价值链(例如,养老基金仍然有最终客户)。

Furthermore, consumers are the employees of the institutional industry, and bring expectations from their personal life into the work environment. See, for example, the consumerization of enterprise software.

此外,消费者是机构行业的雇员,并将个人生活的期望带入工作环境。 例如,参见企业软件的消费化 。

Let’s take the data points discussed so far. Google is launching an aggregator for bank accounts native to its operating system. Apple dominates American mobile proximity payments, making up 5% of global card transactions. Amazon has about 5% of all retail in the US, and 50% of all e-Commerce.

让我们来讨论到目前为止的数据点。 Google正在为其操作系统固有的银行帐户启动一个聚合器。 苹果公司主导着美国的移动近距离支付,占全球卡交易的5%。 亚马逊在美国的零售总额中约占5%,在所有电子商务中占50%。

We are in still in the very beginning of the digital shift. These trillion dollar companies have far more than 5% of our attention, and they will work to expand and monetize until everything is incorporated. Alternately, we will make them do it and pay them for the privilege.

我们仍处于数字化转型的初期。 这些万亿美元的公司所吸引的注意力远远超过了我们的5%,并且它们将努力扩大规模并从中获利,直到一切合并。 或者,我们将让他们这样做并向他们支付特权。

对财务的影响 (Implications for Finance)

The tech companies will become the storefront to absolutely everything.

高科技公司将成为绝对一切的店面 。

There is no Internet, there is only Google.

没有互联网,只有谷歌。

There is no commerce, there is only Amazon.

没有贸易,只有亚马逊。

There is no finance, there is only WeChat / Tencent?

没有金融,只有微信/腾讯?

I don’t know about you, but I cannot pay for anything in cash in London anymore. COVID has made the city go cashless. For China, QR codes have long replaced the need for paper money. And if there is no cash, what is the point of ATMs, and ATM fees, and bank branches, and bank branch staff? Financial firms no longer need to be the place where you shop for financial product.

我不认识你,但是我再也无法在伦敦用现金支付任何东西了。 COVID使这座城市变得无现金。 对于中国来说,QR码早已取代了对纸币的需求。 如果没有现金,自动柜员机,自动柜员机收费,银行分行和银行分行工作人员的目的是什么? 金融公司不再需要成为您购买金融产品的地方。

Financial firms do still need to manufacture the financial products. They do need to deploy balance sheet and lend it out, or choose investments to package into a fund, or underwrite insurance. And then they need to fight really hard to make sure that the tech company algorithms rank highly whatever it is that they have to sell.

金融公司仍然确实需要制造金融产品。 他们确实需要部署资产负债表并将其借出,或者选择投资打包成基金,或者承保保险。 然后,他们需要非常努力地进行工作,以确保技术公司的算法在其必须出售的产品中排名很高。

This leaves us to consider fintech and crypto firms. First, what are Robinhood and Revolut? Which flank should they protect — manufacturing or distribution? On distribution, they can effortlessly get squeezed by the tech incumbents. To acquire a customer, the fintech firm pays a fee to the tech company for advertising, hosting, and many other pleasures.

这使我们可以考虑金融科技和加密货币公司。 首先,什么是Robinhood和Revolut? 他们应保护哪个侧面-生产或分销? 在发行方面,他们可以毫不费力地受到技术在位者的挤压。 为了获得客户,这家金融科技公司向该科技公司支付了广告,托管和许多其他娱乐活动的费用。

On manufacturing, the licensed handling of money is the entire business model. The reason Robinhood can get paid hundreds of million of dollars in trade order flow is because it is a broker/dealer. If you rent your regulated infrastructure — for banking or payments — there are barely any economics left in the business.

在制造业中,许可的金钱处理是整个商业模式。 Robinhood之所以可以从贸易订单流中获得数亿美元的报酬,是因为它是经纪人/经销商。 如果您租用受监管的基础设施(用于银行业务或付款),则业务中几乎没有任何经济效益。

Crypto firms, on the other hand, have some advantages. First, they are much earlier in the market adoption lifecycle, and as a result the probability spread of outcomes is broader. There is a high possibility of being worth nothing at all, but also a reasonable chance of carving out a new, defensible footprint.

另一方面,加密货币公司具有一些优势。 首先,它们在市场采用生命周期中要早得多,因此结果的概率分布范围更大。 根本一文不值的可能性很高,但也有合理的机会创造出新的,可辩护的足迹。

No company building the internet of value (e.g., Web3, blockchain-based finance) has an impenetrable network effect yet. And further, entrepreneurs are much more oriented towards open-source solutions and the prevention of Internet monopoly outcomes.

尚无建立价值互联网的公司(例如,Web3,基于区块链的金融)具有不可渗透的网络效应。 而且,企业家更加注重开源解决方案和防止互联网垄断成果。

As an example, the most valuable blockchain technology today — Ethereum — is an entirely open, decentralized protocol beyond singular ownership. This implies that if value accrues to the network, it can accrue to the token holders broadly, and to the builders that make the network better.

例如,当今最有价值的区块链技术-以太坊(Ethereum)-是一种完全开放的,分散的协议,超越了单一所有权。 这意味着,如果价值积累到网络中,它就可以广泛地积累到代币持有者以及使网络变得更好的建设者身上。

For crypto companies to leapfrog banking incumbents, the right partner is the large tech firm to provide distribution to the consumer market. Some companies, like Coinbase, have built this footprint organically. But there is much more to come.

对于加密货币公司而言,要超越银行业老大,合适的合作伙伴是向消费者市场提供分销的大型科技公司。 一些公司,例如Coinbase,已经有机地建立了这个足迹。 但是还有更多。

For more analysis parsing 12 frontier technology developments every week, a podcast conversation on operating fintechs, and novel food-for-thought essays

如需每周分析12项前沿技术发展的更多分析, 关于运营金融 技术的播客对话以及新颖的,有思想的饮食文章

— > become a Blueprint member here.

谷歌团队在平安金融中心

176

176

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言