用于股票价格预测的神经网络

题目:

Neural networks for stock price prediction

作者:

Yue-Gang Song, Yu-Long Zhou, Ren-Jie Han

来源:

Statistical Finance

Machine Learning (cs.LG)

Submitted on 29 May 201

文档链接:

https://arxiv.org/pdf/1703.04691v5.pdf

代码链接:

https://github.com/atharvacc/SigmaNewsProject

摘要

由于金融市场极不稳定,人们普遍认为股票价格预测是一项充满挑战的任务。然而,为了获取利润或了解股票市场的本质,众多市场参与者或研究人员尝试使用各种统计,计量经济学甚至神经网络模型来预测股票价格。在这项工作中,我们调查和比较了五种神经网络模型的预测能力,即反向传播(BP)神经网络,径向基函数(RBF)神经网络,广义回归神经网络(GRNN),支持向量机回归(SVMR) ),最小二乘支持向量机回归(LS-SVMR)。我们应用这五种模型对三种个股进行价格预测,即中国银行,万科A和贵州茅台。

要点

1 Introduction

2 Methods

2.1 BP neural networks

2.2 Radial basis function networks

2.3 General regression neural networks

2.4 Support vector regression

2.5 Least squares SVM

3 Data, Results and Discussions

3.1 Data description

3.2 Hyper-Parameters

3.3 Results

3.4 Two more discussions: stability of BP and market inefficiency

4 Conclusion

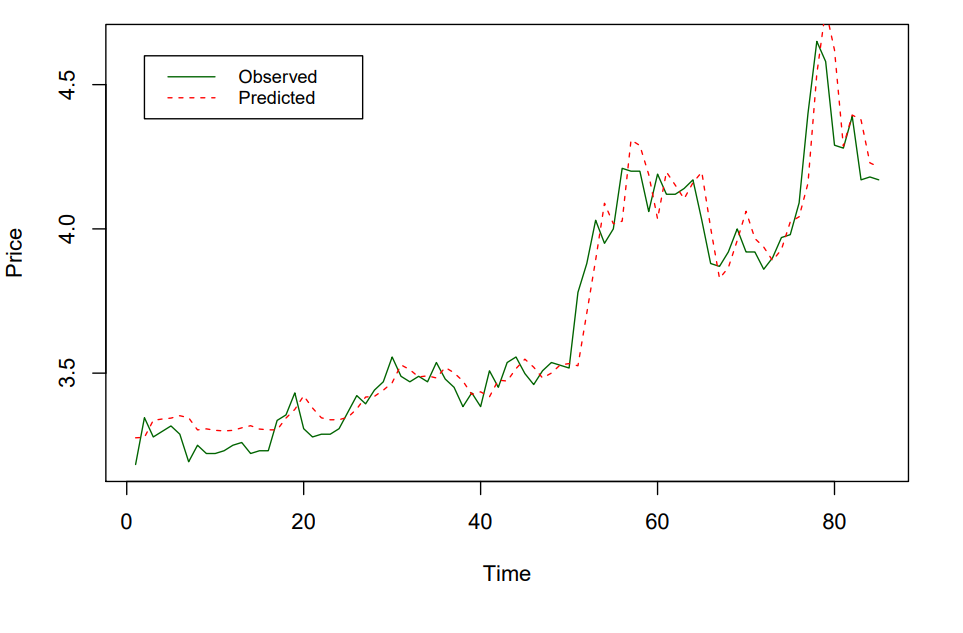

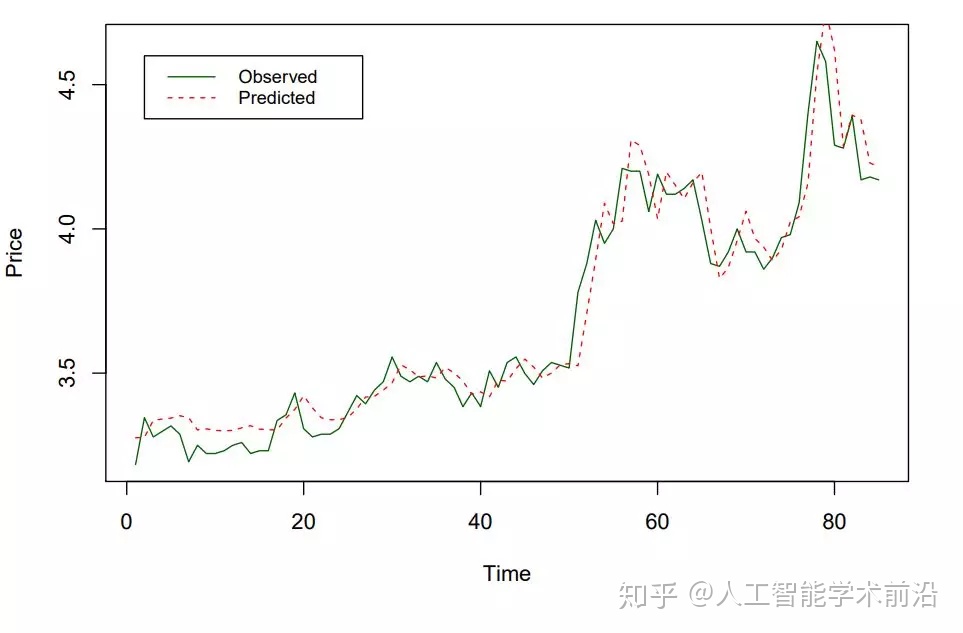

表1给出了五种神经网络模型的性能。由此可见,这五种模型都具有一定的预测能力。即使是最坏的GRNN。MAPE不超过5%,考虑到我们预测的是股价而不是波动率,这是非常令人满意的。在所有三支股票中,MSE和MAPE都是如此。BP神经网络优于其他四种模型。SVMR在这三支股票中始终排名第二。然而,无论是MSE还是MAPE, SVMR的结果都比BP至少大10%。此外,根据中国银行(Bank of China)和万科A.的预测,在这两种标准下,BP神经网络在两项指标中都比SVMR高20%。

图1为中国银行的观察价格和预测价格。可以看出,预测值与实测值吻合较好。并对拐点进行了较为及时的预测。当实际价格有变化趋势时,预测值也随之变化。

英文原文

Due to the extremely volatile nature of financial markets, it is commonly accepted that stock price prediction is a task full of challenge. However in order to make profits or understand the essence of equity market, numerous market participants or researchers try to forecast stock price using various statistical, econometric or even neural network models. In this work, we survey and compare the predictive power of five neural network models, namely, back propagation (BP) neural network, radial basis function (RBF) neural network, general regression neural network (GRNN), support vector machine regression (SVMR), least squares support vector machine regresssion (LS-SVMR). We apply the five models to make price prediction of three individual stocks, namely, Bank of China, Vanke A and Kweichou Moutai. Adopting mean square error and average absolute percentage error as criteria, we find BP neural network consistently and robustly outperforms the other four models.

708

708

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言