文章目录

Montecarlo Methods

1 原理介绍

- key: to estimate the expected values of dependent variables.

1.1 Pseudo-Code 介绍原理

- We do so by drawing a random sample of 𝑛 random numbers, 𝑥1,𝑥2,…,𝑥𝑛, from the specified distribution.

- We map these values onto a sample of the dependent variable 𝑌: 𝑓(𝑥1),𝑓(𝑥2),…,𝑓(𝑥𝑛).

- We can use the sample mean y ˉ \bar{y} yˉ=∑𝑛𝑖=1𝑓(𝑥𝑖)/𝑛 to estimate 𝐄[𝑌].

- Provided that 𝑛 is sufficiently large, our estimate will be accurate by the law of large numbers.

- y ˉ \bar{y} yˉ is called the Monte-Carlo estimator.

sample = []

for i in range(n):

x = draw_random_value(distribution)

y = f(x)

sample.append(y)

result = mean(sample)

- We can write this more concisely using a comprehension:

inputs = draw_random_value(distribution, size=n)

result = mean([f(x) for x in inputs])

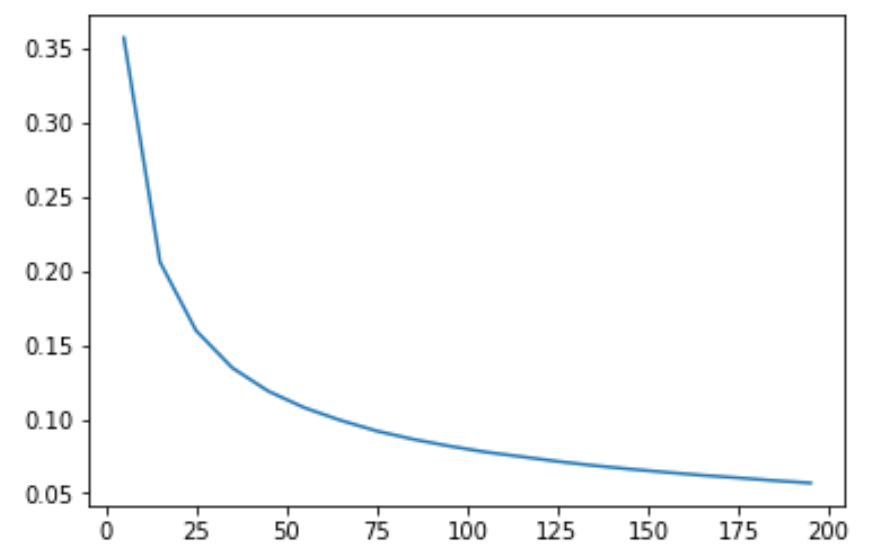

1.2 模拟误差

### 均值误差

mu = 0

def sampling_error(n):

errors = [np.abs(np.mean(np.random.normal(size=n))- mu) \

for i in range(100000)]

return np.mean(errors)

sampling_error(5)

检验误差和样本数的关系

import matplotlib.pyplot as plt

%matplotlib inline

n = np.arange(5, 200, 10)

plt.plot(n, np.vectorize(sampling_error)(n))

2 模拟应用

2.1 估计 π \pi π

import numpy as np

def f(x, y):

if x*x + y*y < 1:

return 1.

else:

return 0.

n = 1000000

X = np.random.random(size=n)

Y = np.random.random(size=n)

pi_approx = 4 * np.mean([f(x, y) for (x, y) in zip(X,Y)])

print("Pi is approximately %f" % pi_approx)

2.2 结合 map-reduce 估计 π \pi π

samples = 10000

def f(x,y):

if x**2 + y**2 < 1:

return 1

else:

return 0

def sample(p):

return f(np.random.random(),np.random.random())

reduce(lambda x,y:x+y,(map(sample,[1]*samples)))/samples * 4

2.2 欧式看涨期权-European call option

- 看涨期权:以固定价格(strike price 𝐾)在到期日(maturity date 𝑇)购进一种资产(该资产价格为 S t S_t St)的权利。一般来说,当证券价格 S t S_t St 小于行使价格 𝐾 时,

- S 0 S_0 S0 :初始价格 Initial price level of the security .

- 𝐾 𝐾 K: 行使价格 strike price

- 𝑇 𝑇 T: 到期日 maturity date(time to maturity)

- σ \sigma σ: 底层资产波动率 Volatility of the security.

- r r r:risk-free interest rate.

- payoff = m a x { S T − K , 0 } max\{S_T -K,0\} max{ST−K,0}

S T = S 0 e x p { ( r − σ 2 2 ) T + σ ϕ T } S_T = S_0 exp\{ (r-\frac{\sigma^2}{2})T + \sigma \phi \sqrt{T} \} ST=S0exp{(r−2σ2)T+σϕT}

### European Call Option

### non-path-dependent- 一步随机,没有累积过程,直接用参数计算S_T

from numpy import sqrt, exp, cumsum, sum, maximum, mean

from numpy.random import standard_normal

# Parameters

S0 = 100.; K = 105.

T = 1.0

r = 0.02; sigma = 0.1

I = 100000

# Simulate I outcomes

S = S0 * exp((r - 0.5 * sigma ** 2) * T + sigma * sqrt(T) *

standard_normal(I))

# Calculate the Monte Carlo estimator

C0 = exp(-r * T) * mean(maximum(S - K, 0))

print("Estimated present value is %f" % C0)

2.3 亚式看涨期权-Asian (Average Value) Call Option

- 看涨期权:以固定价格(strike price 𝐾)在到期日(maturity date 𝑇)购进一种资产(该资产价格为 S t S_t St)的权利。一般来说,当证券价格 S t S_t St 小于行使价格 𝐾 时,可以理解成不行权,价值为0

- S 0 S_0 S0:初始价格 Initial price level of the security.

- K K K: 行使价格 strike price

- 𝑇 𝑇 T: 到期日 maturity date(time to maturity)

- M M M: GBM 步数(number of time steps)

- Δ \Delta Δ: 时间间隔 (dt), Δ = T / M \Delta = T/M Δ=T/M

- σ \sigma σ: 底层资产波动率 Volatility of the security.

- I I I : I I I 种 GBM 可能的路径(number of independent realisations): I = 1 0 5 I=10^5 I=105 .

- r r r: risk-free interest rate.

- payoff = m a x { S T − K , 0 } max\{S_T -K,0\} max{ST−K,0}

思想:

- To simulate GBM at 𝑀 evenly spaced time intervals 𝑡𝑖 with Δ=𝑇/𝑀 :

### Asian (Average Value) Call Option -- neet to know values at every time point

### path-dependent - 需要积累,要算均值

from numpy import sqrt, exp, cumsum, sum, maximum, mean

from numpy.random import standard_normal

import numpy as np

# Parameters

S0 = 100.; T = 1.0; K = 50; r = 0.02; sigma = 0.1

M = 200; dt = T / M; I = 100000

def inner_value(S):

# Intrinsic value for a fixed-strike Asian call option

# This uses a list comprehension (though there is probably a faster, vectorised way possible)

return np.array([max(V - K,0) for V in mean(S, axis=0)])

# Simulate I paths with M time steps

S = S0 * exp(cumsum((r - 0.5 * sigma ** 2) * dt + sigma * sqrt(dt) *

standard_normal((M, I)), axis=0))

# Calculate the Monte Carlo estimator

C0 = exp(-r * T) * mean(inner_value(S))

print("Estimated present value is %f" % C0)

2769

2769

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言