干预分析模型 - GDP预测

加载pandas、matplotlib等包,处理时间序列

import pandas as pd

import numpy as np

import matplotlib.pylab as plt

%matplotlib inline

plt.rcParams['axes.unicode_minus'] = False

plt.rcParams['font.sans-serif'] = ['Simhei']

from matplotlib.pylab import rcParams

rcParams['figure.figsize'] = 15, 6

import warnings

warnings.filterwarnings("ignore")

读入数据

data = pd.read_csv('China GDP 1980-2016.csv')

data.head()

|

Year |

GDP |

| 0 |

2016 |

743585.5 |

| 1 |

2015 |

689052.1 |

| 2 |

2014 |

643974.0 |

| 3 |

2013 |

595244.4 |

| 4 |

2012 |

540367.4 |

data.dtypes

Year int64

GDP float64

dtype: object

data.columns

Index(['Year', 'GDP'], dtype='object')

Year 是int64类型,在时间序列分析中,我们需要现将数据转化为时间序列

dateparse = lambda dates: pd.datetime.strptime(dates, '%Y')

dateparse('1962')

datetime.datetime(1962, 1, 1, 0, 0)

df = pd.read_csv('China GDP 1980-2016.csv', parse_dates=['Year'], index_col='Year', date_parser=dateparse)

df.head()

|

GDP |

| Year |

|

| 2016-01-01 |

743585.5 |

| 2015-01-01 |

689052.1 |

| 2014-01-01 |

643974.0 |

| 2013-01-01 |

595244.4 |

| 2012-01-01 |

540367.4 |

df.index

DatetimeIndex(['2016-01-01', '2015-01-01', '2014-01-01', '2013-01-01',

'2012-01-01', '2011-01-01', '2010-01-01', '2009-01-01',

'2008-01-01', '2007-01-01', '2006-01-01', '2005-01-01',

'2004-01-01', '2003-01-01', '2002-01-01', '2001-01-01',

'2000-01-01', '1999-01-01', '1998-01-01', '1997-01-01',

'1996-01-01', '1995-01-01', '1994-01-01', '1993-01-01',

'1992-01-01', '1991-01-01', '1990-01-01', '1989-01-01',

'1988-01-01', '1987-01-01', '1986-01-01', '1985-01-01',

'1984-01-01', '1983-01-01', '1982-01-01', '1981-01-01',

'1980-01-01'],

dtype='datetime64[ns]', name='Year', freq=None)

ts = df['GDP'].sort_index()

ts.head()

Year

1980-01-01 4587.6

1981-01-01 4935.8

1982-01-01 5373.4

1983-01-01 6020.9

1984-01-01 7278.5

Name: GDP, dtype: float64

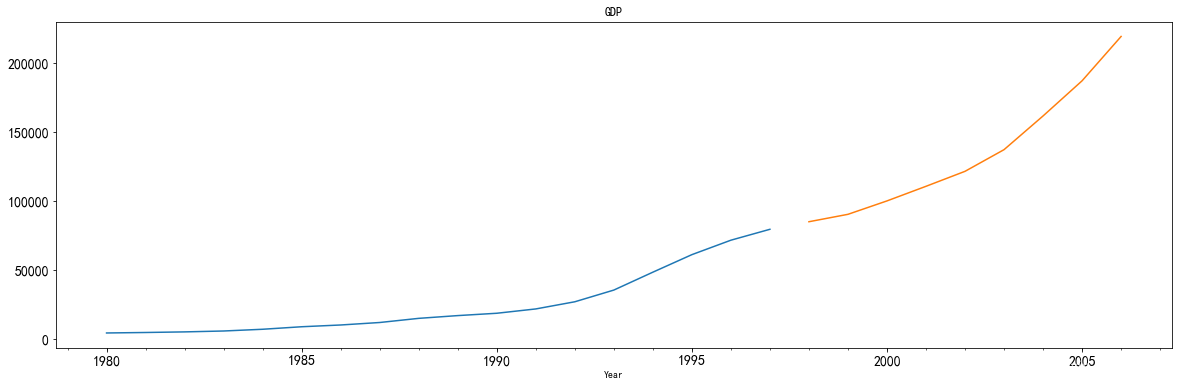

拆分数据为训练集和测试集

min(ts.index), max(ts.index)

(Timestamp('1980-01-01 00:00:00'), Timestamp('2016-01-01 00:00:00'))

train = ts['1980':'1997']

test = ts['1998':'2006']

平稳性检验

绘制时序图

train.plot(figsize=(20,6), fontsize=14, label="train")

test.plot(figsize=(20,6), title= 'GDP', fontsize=14, label="test")

plt.show()

[外链图片转存 (img-xLpGUy3F-1562729294200)(output_16_0.png)]

(img-xLpGUy3F-1562729294200)(output_16_0.png)]

平稳性检验

from statsmodels.tsa.stattools import adfuller

def test_stationarity(timeseries):

print('Results of Dickey-Fuller Test:')

dftest = adfuller(timeseries, autolag='AIC')

dfoutput = pd.Series(dftest[0:4], index=['Test Statistic','p-value','#Lags Used','Number of Observations Used'])

for key,value in dftest[4].items():

dfoutput['Critical Value ({})'.

这篇博客探讨了如何运用干预分析模型预测中国的GDP。首先,通过加载pandas和matplotlib等库处理时间序列数据,并将Year字段转化为时间序列。接着,数据被划分为训练集和测试集。在平稳性检验中,发现原始序列非平稳,因此进行了指数变换和差分处理。随后,使用ARMA模型进行拟合,并将预测值还原为指数变换前的形式。最后,对比了AR模型的预测效果。

这篇博客探讨了如何运用干预分析模型预测中国的GDP。首先,通过加载pandas和matplotlib等库处理时间序列数据,并将Year字段转化为时间序列。接着,数据被划分为训练集和测试集。在平稳性检验中,发现原始序列非平稳,因此进行了指数变换和差分处理。随后,使用ARMA模型进行拟合,并将预测值还原为指数变换前的形式。最后,对比了AR模型的预测效果。

最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

4245

4245

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言