提示:文章写完后,目录可以自动生成,如何生成可参考右边的帮助文档

数据分析项目-合集-day01

需求:股票分析

-

使用tushare包获取某支股票历史行情数据。

-

输出该股票所有收盘比开盘上涨3%的日期。

-

输出该股票所有开盘比上日收盘跌幅超过2%的日期

-

假如我从2010年开始,每月第一个交易日买入1手股票,每年最后一个交易日卖出所有股票,到今天为止,我的收益如何?

-

tushare财经数据接口包

-

pip install tushare

import tushare as ts

import pandas as pd

from pandas import DataFrame,Series

import numpy as np

获取某只股票的历史行情数据

#code 字符串形式的股票代码

df=ts.get_k_data(code="600519",start="2000-01-01")

df

运行结果:

date open close high low volume code

0 2001-08-27 -91.359 -91.174 -90.778 -91.654 406318.00 600519

1 2001-08-28 -91.274 -90.941 -90.916 -91.341 129647.79 600519

2 2001-08-29 -90.920 -91.027 -90.916 -91.076 53252.75 600519

3 2001-08-30 -91.044 -90.899 -90.826 -91.094 48013.06 600519

4 2001-08-31 -90.890 -90.915 -90.806 -90.952 23231.48 600519

... ... ... ... ... ... ... ...

4939 2022-04-27 1767.120 1794.920 1810.000 1767.120 57402.00 600519

4940 2022-04-28 1793.000 1835.000 1845.000 1786.500 44010.00 600519

4941 2022-04-29 1836.000 1828.380 1849.000 1810.980 34885.00 600519

4942 2022-05-05 1830.000 1837.000 1870.000 1828.980 33661.00 600519

4943 2022-05-06 1814.990 1793.000 1819.000 1781.000 28596.00 600519

4944 rows × 7 columns

将互联网上获取的股票数据存储到本地

#调用to_xxx方法将df中的数据写入到本地进行存储

df.to_csv("./maotai.csv")

#将本地存储的数据读入到df

df=pd.read_csv("./maotai.csv")

df.head()

运行结果:

Unnamed: 0 date open close high low volume code

0 0 2001-08-27 -91.359 -91.174 -90.778 -91.654 406318.00 600519

1 1 2001-08-28 -91.274 -90.941 -90.916 -91.341 129647.79 600519

2 2 2001-08-29 -90.920 -91.027 -90.916 -91.076 53252.75 600519

3 3 2001-08-30 -91.044 -90.899 -90.826 -91.094 48013.06 600519

4 4 2001-08-31 -90.890 -90.915 -90.806 -90.952 23231.48 600519

需要对读取出来的数据进行相关的处理

删除df中指定的一列

axis输入0代表列,1代表行。但是对drop方法而言,正好是相反的

df.drop(labels="Unnamed: 0",axis=1,inplace=True)

df.head()

运行结果:

date open close high low volume code

0 2001-08-27 -91.359 -91.174 -90.778 -91.654 406318.00 600519

1 2001-08-28 -91.274 -90.941 -90.916 -91.341 129647.79 600519

2 2001-08-29 -90.920 -91.027 -90.916 -91.076 53252.75 600519

3 2001-08-30 -91.044 -90.899 -90.826 -91.094 48013.06 600519

4 2001-08-31 -90.890 -90.915 -90.806 -90.952 23231.48 600519

查看每一列数据类型

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 4944 entries, 0 to 4943

Data columns (total 7 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 4944 non-null object

1 open 4944 non-null float64

2 close 4944 non-null float64

3 high 4944 non-null float64

4 low 4944 non-null float64

5 volume 4944 non-null float64

6 code 4944 non-null int64

dtypes: float64(5), int64(1), object(1)

memory usage: 270.5+ KB

将date列转为时间序列类型

#由于后续很多操作需要用到日期

df["date"]=pd.to_datetime(df["date"])

#将date列作为源数据的行索引

df.set_index("date",inplace=True)

df.head()

运行结果:

open close high low volume code

date

2001-08-27 -91.359 -91.174 -90.778 -91.654 406318.00 600519

2001-08-28 -91.274 -90.941 -90.916 -91.341 129647.79 600519

2001-08-29 -90.920 -91.027 -90.916 -91.076 53252.75 600519

2001-08-30 -91.044 -90.899 -90.826 -91.094 48013.06 600519

2001-08-31 -90.890 -90.915 -90.806 -90.952 23231.48 600519

输出该股票所有收盘比开盘上涨3%的日期。

#伪代码: (收盘-开盘)/开盘 >0.03

(df["close"]-df["open"])/df["open"]>0.03

#在分析过程中产生的布尔值,则下一步马上将布尔运算作为源数据的行索引

#如果布尔值作为df的行索引,则可以取出true对应的行数据,忽略false对应的行数据

df.loc[(df["close"]-df["open"])/df["open"]>0.03]#获取了True对应的行数据

df.loc[(df["close"]-df["open"])/df["open"]>0.03].index #df的行数据

运行结果:

DatetimeIndex(['2006-05-25', '2006-06-02', '2006-12-19', '2006-12-21',

'2006-12-22', '2007-01-04', '2007-01-08', '2007-01-16',

'2007-01-23', '2007-01-31',

...

'2021-09-01', '2021-09-17', '2021-09-24', '2021-09-27',

'2021-10-13', '2021-12-08', '2021-12-23', '2022-02-09',

'2022-03-01', '2022-04-12'],

dtype='datetime64[ns]', name='date', length=748, freq=None)

输出该股票所有开盘比上日收盘跌幅超过2%的日期

#伪代码: (开盘-前日收盘)/前日收盘 < -0.02

(df["open"]-df["close"].shift(1))/df["close"].shift(1)<-0.02

#将布尔值作为源数据的行索引取出True对应的行数据

df.loc[(df["open"]-df["close"].shift(1))/df["close"].shift(1)<-0.02]

#根据index取出满足条件的日期

df.loc[(df["open"]-df["close"].shift(1))/df["close"].shift(1)<-0.02].index

运行结果:

DatetimeIndex(['2006-02-13', '2006-04-17', '2006-04-18', '2006-04-19',

'2006-04-20', '2006-05-25', '2006-05-30', '2006-12-27',

'2007-01-04', '2007-01-22',

...

'2020-03-23', '2020-10-26', '2021-02-26', '2021-03-04',

'2021-04-28', '2021-08-20', '2021-11-01', '2022-03-14',

'2022-03-15', '2022-03-28'],

dtype='datetime64[ns]', name='date', length=378, freq=None)

- 需求:假如我从2010年开始,每月第一个交易日买入1手股票,每年最后一个交易日卖出所有股票,到今天为止,我的收益如何?

- 分析:

- 时间节点:2010-2022

- 一手股票:100支股票

- 买:

- 一个完整的年需要买入1200支股票

- 卖:

- 一个完整的年需要卖出1200支股票

- 买卖股票的单价:

- 开盘价

new_df=df["2010-01":"2022-04"]

new_df

运行结果:

open close high low volume code

date

2010-01-04 35.594 34.047 35.594 33.573 44304.88 600519

2010-01-05 34.835 33.671 35.219 33.340 31513.18 600519

2010-01-06 33.333 31.657 33.716 31.319 39889.03 600519

2010-01-07 31.657 29.373 31.980 27.991 48825.55 600519

2010-01-08 29.584 28.081 29.584 26.654 36702.09 600519

... ... ... ... ... ... ...

2022-04-25 1750.000 1708.000 1776.500 1702.000 53658.00 600519

2022-04-26 1703.330 1732.480 1748.980 1700.000 44564.00 600519

2022-04-27 1767.120 1794.920 1810.000 1767.120 57402.00 600519

2022-04-28 1793.000 1835.000 1845.000 1786.500 44010.00 600519

2022-04-29 1836.000 1828.380 1849.000 1810.980 34885.00 600519

2988 rows × 6 columns

买股票:找到每个月的第一个交易日对应的行数据(捕获到开盘价)==>>每月的第一行数据

#根据月份从原始数据中提取指定的数据

#每月第一个交易日对应的行数据

df_monthly=new_df.resample("M").first()#数据的重写取样

df_monthly

运行结果:

open close high low volume code

date

2010-01-31 35.594 34.047 35.594 33.573 44304.88 600519

2010-02-28 33.250 33.258 33.776 31.845 29655.94 600519

2010-03-31 31.424 31.267 32.176 31.079 21734.74 600519

2010-04-30 25.662 26.624 26.954 25.647 23980.83 600519

2010-05-31 2.529 3.017 3.708 1.702 23975.16 600519

... ... ... ... ... ... ...

2021-12-31 1950.000 1932.990 1959.950 1919.020 26254.00 600519

2022-01-31 2055.000 2051.230 2068.950 2014.000 33843.00 600519

2022-02-28 1900.990 1867.960 1913.560 1850.000 35150.00 600519

2022-03-31 1802.000 1858.480 1863.570 1802.000 47379.00 600519

2022-04-30 1729.940 1780.010 1793.000 1721.690 44862.00 600519

148 rows × 6 columns

#买入股票花费的总金额

cost=df_monthly["open"].sum()*100

cost

运行结果:

7779065.1

卖出股票到手的钱

#特殊情况:2022年买入的股票卖不出去

new_df.resample("A").last()

#将2022年最后一行切出去

df_yearly=new_df.resample("A").last()[:-1]

df_yearly

运行结果:

open close high low volume code

date

2010-12-31 43.847 45.440 45.711 43.284 46084.0 600519

2011-12-31 68.243 68.739 70.044 66.011 29460.0 600519

2012-12-31 88.579 85.034 89.810 82.827 51914.0 600519

2013-12-31 20.074 23.694 24.463 18.834 57546.0 600519

2014-12-31 89.937 93.591 93.937 89.391 46269.0 600519

2015-12-31 143.406 143.376 144.686 143.006 19673.0 600519

2016-12-31 257.967 265.507 266.647 257.967 34687.0 600519

2017-12-31 656.144 635.634 664.644 629.744 76038.0 600519

2018-12-31 512.443 539.153 545.543 509.143 63678.0 600519

2019-12-31 1146.682 1146.682 1151.682 1140.192 22588.0 600519

2020-12-31 1921.707 1978.707 1979.687 1919.707 38860.0 600519

2021-12-31 2070.000 2050.000 2072.980 2028.000 29665.0 600519

卖出股票到手的钱

resv=df_yearly["open"].sum()*1200

resv

运行结果:

8422834.8

#最后手中剩余的股票需要估算其价值计算到总收益中

#使用昨天的收盘价作为剩余股票的单价

last_money=400*new_df["close"][-1]

last_money

运行结果:

731352.0

#计算总收益

resv+last_money-cost

运行结果:

1375121.7000000011

需求:双均线策略制定

使用tushare包获取某股票的历史行情数据

df=pd.read_csv('./maotai.csv').drop(labels="Unnamed: 0",axis=1)

df

运行结果:

date open close high low volume code

0 2001-08-27 -91.359 -91.174 -90.778 -91.654 406318.00 600519

1 2001-08-28 -91.274 -90.941 -90.916 -91.341 129647.79 600519

2 2001-08-29 -90.920 -91.027 -90.916 -91.076 53252.75 600519

3 2001-08-30 -91.044 -90.899 -90.826 -91.094 48013.06 600519

4 2001-08-31 -90.890 -90.915 -90.806 -90.952 23231.48 600519

... ... ... ... ... ... ... ...

4939 2022-04-27 1767.120 1794.920 1810.000 1767.120 57402.00 600519

4940 2022-04-28 1793.000 1835.000 1845.000 1786.500 44010.00 600519

4941 2022-04-29 1836.000 1828.380 1849.000 1810.980 34885.00 600519

4942 2022-05-05 1830.000 1837.000 1870.000 1828.980 33661.00 600519

4943 2022-05-06 1814.990 1793.000 1819.000 1781.000 28596.00 600519

4944 rows × 7 columns

#将date列转为时间序列且将其作为源数据的行索引

df["date"]=pd.to_datetime(df["date"])

df.set_index("date",inplace=True)

df.head()

运行结果:

open close high low volume code

date

2001-08-27 -91.359 -91.174 -90.778 -91.654 406318.00 600519

2001-08-28 -91.274 -90.941 -90.916 -91.341 129647.79 600519

2001-08-29 -90.920 -91.027 -90.916 -91.076 53252.75 600519

2001-08-30 -91.044 -90.899 -90.826 -91.094 48013.06 600519

2001-08-31 -90.890 -90.915 -90.806 -90.952 23231.48 600519

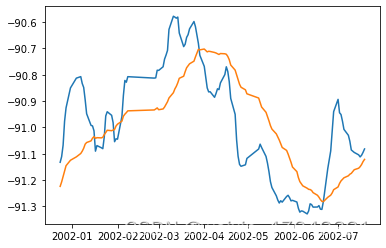

- 计算该股票的历史数据的5日均线和30日均线

- 什么是均线

对于每一个交易日,都可以计算出前N天的移动平均值,然后把这些移动平均值连起来,成为一条线,

就叫做N日移动平均线。移动平均线常用线有5天,10天,30天,60天,120天和240天的指标。

- 5天和10天的是短线操作的参照指标,叫日均线指标

- 30天和60天的是中期指标,叫季均线指标

- 120天和240天的是长期均线指标,叫年均线指标- 均线计算方法:MA=(C1+C2+C3+…+Cn)/N , C:某日收盘价, N:移动平均周期(天数)

ma5=df["close"].rolling(5).mean()

ma30=df["close"].rolling(30).mean()

import matplotlib.pyplot as plt

%matplotlib inline

plt.plot(ma5[50:180])

plt.plot(ma30[50:180])

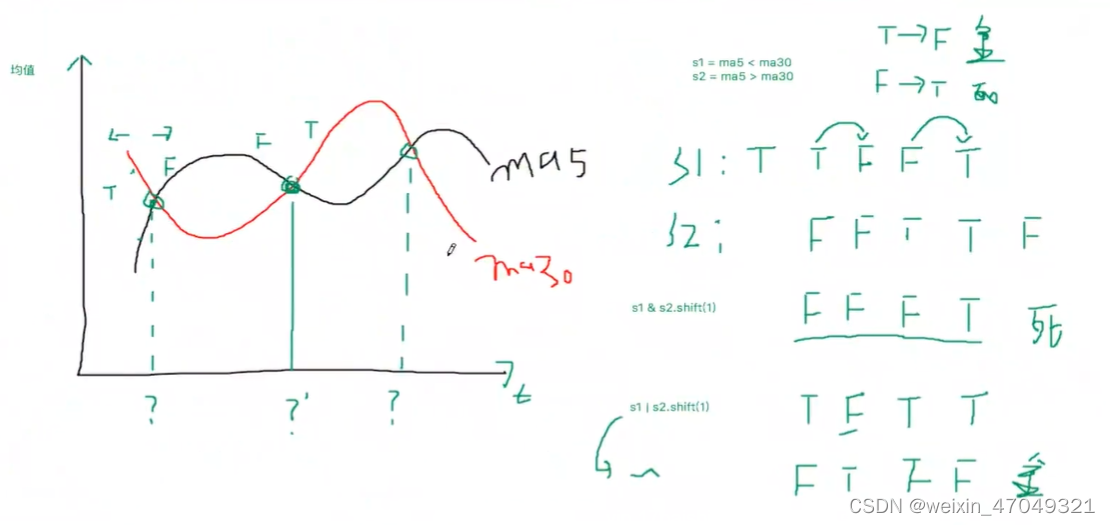

- 分析输出所有的金叉日期和死叉日期

- 股票分析技术中的金叉和死叉,可以解释为:

- 分析指标中的两根线,一根为短时间内的指标线,另一根为较长时间的指标线

- 如果短时间的指标线方向拐头向上,并且穿过了较长时间的指标线,这种状态叫“金叉”

- 如果短时间的指标线方向拐头向下,并且穿过了较长时间的指标线,这种状态叫“死叉”

- 一般情况下,出现金叉后,操作趋向买入;死叉则趋向卖出。当然,金叉和死叉是分析的指标之一,

要和其他很多指标配合使用,才能增加操作的正确性

# 删除ma5和ma30列中的NaN值,前30个.

# 同时df为了和ma5和ma30时间索引相同,也从后30个开始数

ma5=ma5[30:]

ma30=ma30[30:]

df=df[30:]

s1=ma5<ma30

s2=ma5>ma30

#s1从True变为False为金叉,s1从False变为True为死叉

death_ex=s1&s2.shift(1) #判定死叉的条件,(s1 与 “s2.向下移动1行”)

df.loc[death_ex] #死叉对应的行数据

death_date= df.loc[death_ex].index

death_date

运行结果:

DatetimeIndex(['2002-01-17', '2002-01-30', '2002-03-29', '2002-07-29',

'2002-12-27', '2003-03-17', '2003-04-22', '2003-06-20',

'2003-06-30', '2003-08-04',

...

'2020-03-18', '2020-08-10', '2020-09-21', '2020-10-27',

'2021-03-01', '2021-04-15', '2021-05-06', '2021-06-22',

'2021-11-04', '2022-01-06'],

dtype='datetime64[ns]', name='date', length=104, freq=None)

golden_ex=~s1|s2.shift(1) #判定金叉的条件(s1 或 “s2.向下移动1行”)

golden_date=df.loc[golden_ex].index

golden_date

运行结果:

DatetimeIndex(['2001-11-22', '2001-11-23', '2001-11-26', '2001-11-27',

'2001-11-28', '2001-11-29', '2001-11-30', '2001-12-03',

'2001-12-04', '2001-12-05',

...

'2022-04-20', '2022-04-21', '2022-04-22', '2022-04-25',

'2022-04-26', '2022-04-27', '2022-04-28', '2022-04-29',

'2022-05-05', '2022-05-06'],

dtype='datetime64[ns]', name='date', length=2983, freq=None)

3163

3163

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言