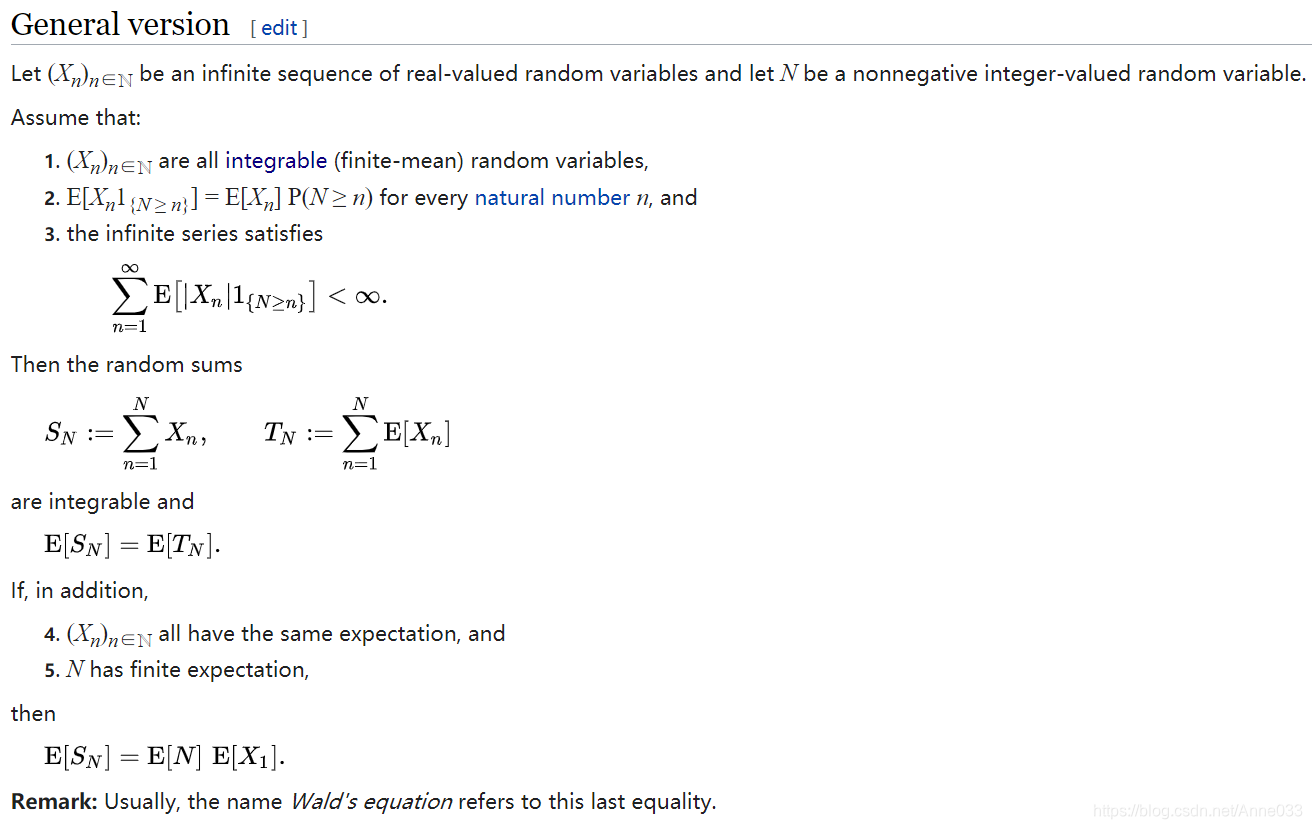

1. Wald’s equation

Let

(

X

n

)

n

∈

N

(X_n)_{n∈ℕ}

(Xn)n∈N be a sequence of real-valued, independent and identically distributed (i.i.d.) random variables and let

N

N

N be a nonnegative integer-value random variable that is independent of the sequence

(

X

n

)

n

∈

N

(X_n)_{n∈ℕ}

(Xn)n∈N. Suppose that

N

N

N and the

X

n

X_n

Xn have finite expectations. Then

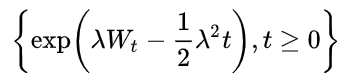

2. Wald’s martingale

In probability theory Wald’s martingale, named after Abraham Wald and more commonly known as the geometric Brownian motion, is a stochastic process of the form

for any real value λ where Wt is a Wiener process. The process is a martingale.

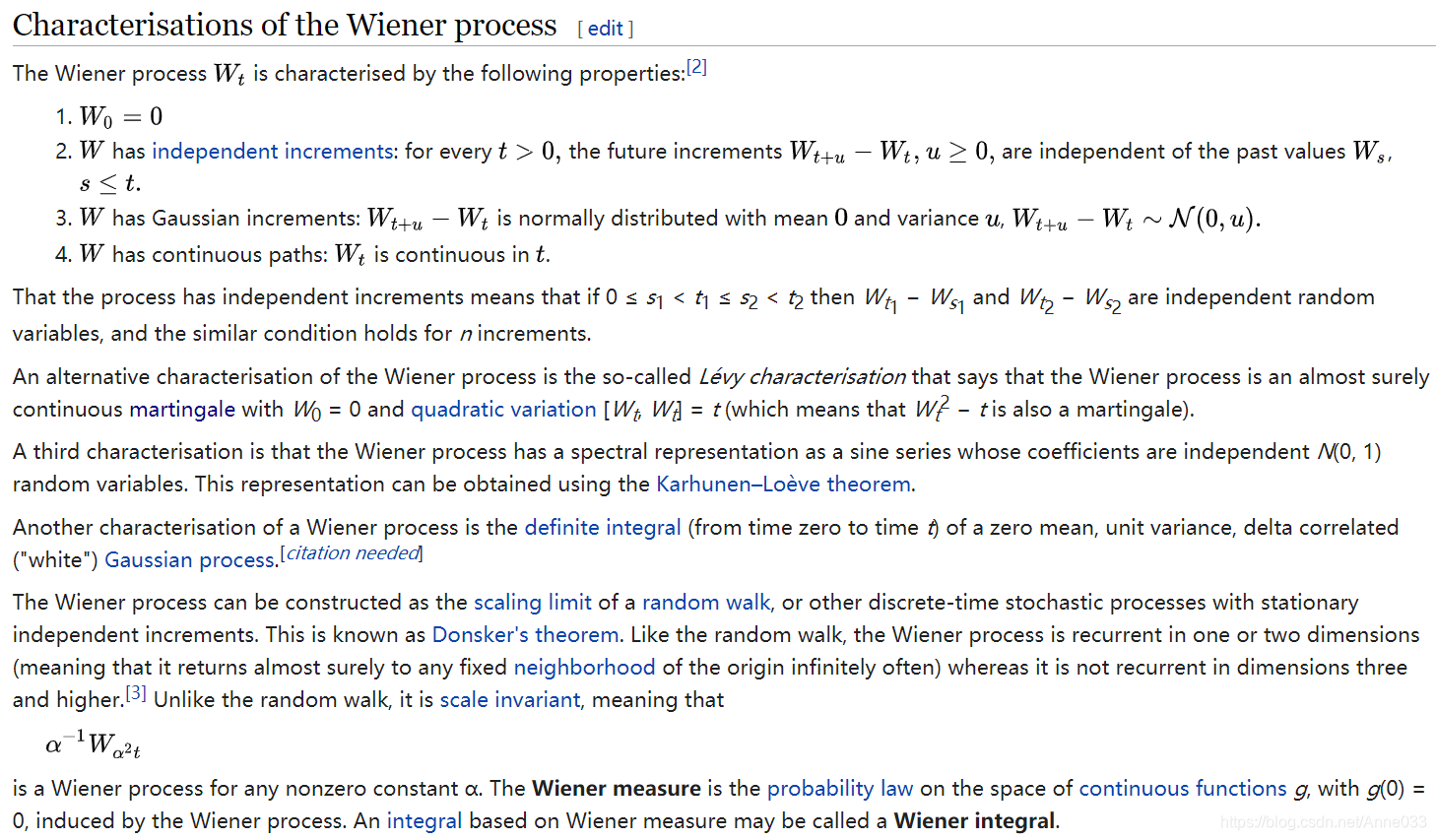

2.1 Wiener process

In mathematics, the Wiener process is a real valued continuous-time stochastic process named in honor of American mathematician Norbert Wiener for his investigations on the mathematical properties of the one-dimensional Brownian motion.[1] It is often also called Brownian motion due to its historical connection with the physical process of the same name originally observed by Scottish botanist Robert Brown. It is one of the best known Lévy processes (càdlàg stochastic processes with stationary independent increments) and occurs frequently in pure and applied mathematics, economics, quantitative finance, evolutionary biology, and physics.

The Wiener process plays an important role in both pure and applied mathematics. In pure mathematics, the Wiener process gave rise to the study of continuous time martingales. It is a key process in terms of which more complicated stochastic processes can be described. As such, it plays a vital role in stochastic calculus, diffusion processes and even potential theory. It is the driving process of Schramm–Loewner evolution. In applied mathematics, the Wiener process is used to represent the integral of a white noise Gaussian process, and so is useful as a model of noise in electronics engineering (see Brownian noise), instrument errors in filtering theory and disturbances in control theory.

The Wiener process has applications throughout the mathematical sciences. In physics it is used to study Brownian motion, the diffusion of minute particles suspended in fluid, and other types of diffusion via the Fokker–Planck and Langevin equations. It also forms the basis for the rigorous path integral formulation of quantum mechanics (by the Feynman–Kac formula, a solution to the Schrödinger equation can be represented in terms of the Wiener process) and the study of eternal inflation in physical cosmology. It is also prominent in the mathematical theory of finance, in particular the Black–Scholes option pricing model.

3. wald定理

wald定理:

设

{

X

n

,

n

≥

1

}

\{X_n,n\geq 1\}

{Xn,n≥1}为i.i.d.随机变量序列,

E

[

X

1

]

<

+

∞

E[X_1]<+∞

E[X1]<+∞,r为一取正整数值的随机变量,

E

r

<

+

∞

Er<+∞

Er<+∞,且对一切

n

≥

1

,

r

=

n

n\geq 1,{r=n}

n≥1,r=n与

{

X

n

+

1

,

X

n

+

2

…

…

}

\{X_{n+1},X_{n+2}……\}

{Xn+1,Xn+2……}相互独立,则

E

∑

r

n

=

1

X

n

l

<

+

∞

E\sum_r n=1 Xnl<+∞

E∑rn=1Xnl<+∞,且

E

[

X

1

+

X

2

+

…

+

X

r

l

]

=

E

r

E

x

1

E[X_1+X_2+…+Xrl]=ErEx1

E[X1+X2+…+Xrl]=ErEx1

https://en.wikipedia.org/wiki/Wald%27s_equation

https://en.wikipedia.org/wiki/Wiener_process#Brownian_martingales

https://zh.wikipedia.org/wiki/%E7%BB%B4%E7%BA%B3%E8%BF%87%E7%A8%8B

960

960

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言