普通线性回归

1.最小二乘线性模型

> dat=read.csv("https://raw.githubusercontent.com/happyrabbit/DataScientistR/master/Data/SegData.csv")

> dat=subset(dat,store_exp >0&online_exp >0)

> modeldat=dat[,grep("Q",names(dat))]

> modeldat$total_exp=dat$store_exp+dat$online_exp

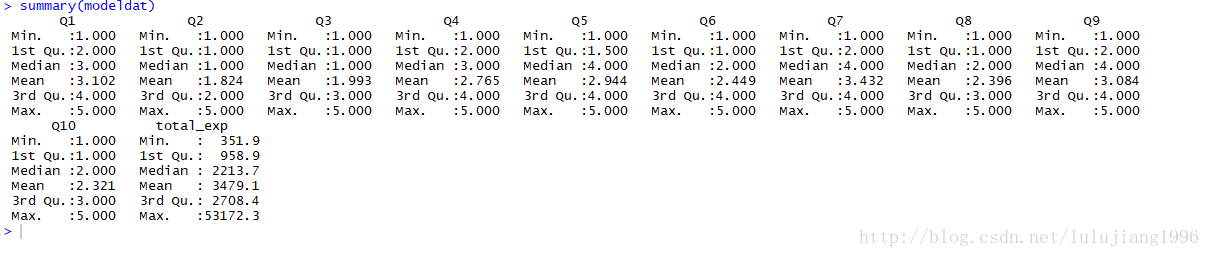

下面展示输出结果,看哈数据是否有缺失值或离群点

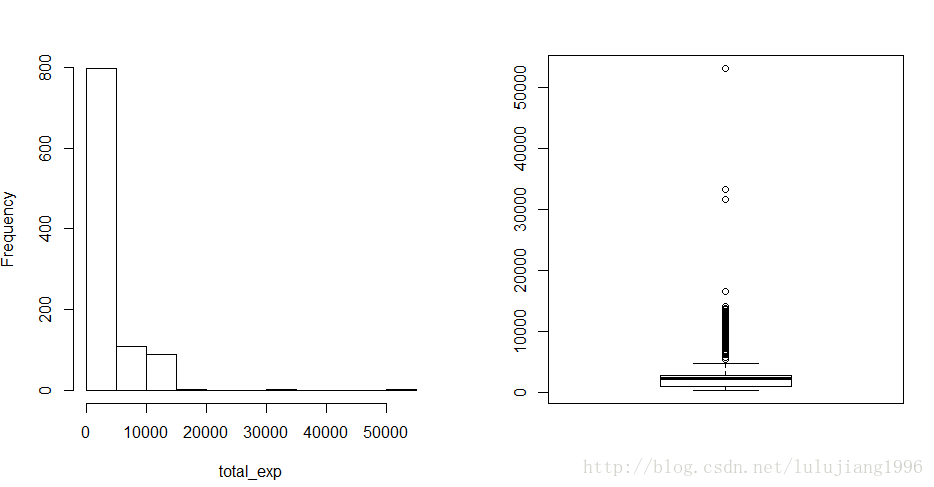

> par(mfrow=c(1,2))

> hist(modeldat$total_exp,main="",xlab="total_exp")

> boxplot(modeldat$total_exp)

>

如上,数据集modeldat中没有缺失值,但是明显有离群点,而且因变量total_exp分布明显偏离正太。

我们需要删除离群点,然后对因变量进行对数变换

我们用Z分值的方法查找并删除离群点。

> y=modeldat$total_exp

#求z分值

> zs=(y-mean(y))/mad(y)

#找到z分值大于3.5的离群点,删除这些观测

> modeldat=modeldat[-which(zs>3.5),]

> 接下来检查变量的共线性

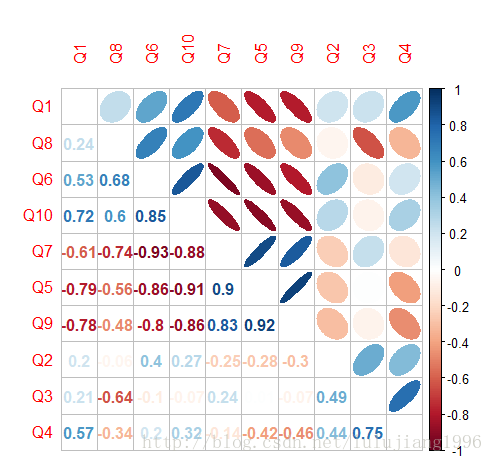

> library(corrplot)

corrplot 0.84 loaded

Warning message:

程辑包‘corrplot’是用R版本3.4.3 来建造的

> correlation=cor(modeldat[,grep("Q",names(modeldat))])

> corrplot.mixed(correlation,order="hclust",tl.pos="lt",upper="ellipse")

由上图可以看出,变量之间有很强的相关性。

我们需要删除高度相关变量的算法,设置阈值为0.75

> library(caret)

载入需要的程辑包:lattice

载入需要的程辑包:ggplot2

Warning messages:

1: 程辑包‘caret’是用R版本3.4.3 来建造的

2: 程辑包‘lattice’是用R版本3.4.3 来建造的

3: 程辑包‘ggplot2’是用R版本3.4.3 来建造的

> highcor=findCorrelation(correlation,cutoff=.75)

> modeldat=modeldat[,-highcor]

现在我们可以拟合线性模型。“.“表示数据集modeldat中除了因变量外所有的变量都被当做自变量,这里我们没有考虑交互效应。

且我们对原始变量进行了对数变换

> limfit=lm(log(total_exp)~.,data=modeldat)

> summary(lmfit)

Error in summary(lmfit) : object 'lmfit' not found

> summary(limfit)

Call:

lm(formula = log(total_exp) ~ ., data = modeldat)

Residuals:

Min 1Q Median 3Q Max

-1.17494 -0.13719 0.01284 0.14163 0.56227

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 8.098314 0.054286 149.177 < 2e-16 ***

Q1 -0.145340 0.008823 -16.474 < 2e-16 ***

Q2 0.102275 0.019492 5.247 1.98e-07 ***

Q3 0.254450 0.018348 13.868 < 2e-16 ***

Q6 -0.227684 0.011520 -19.764 < 2e-16 ***

Q8 -0.090706 0.016497 -5.498 5.15e-08 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.2262 on 805 degrees of freedom

Multiple R-squared: 0.8542, Adjusted R-squared: 0.8533

F-statistic: 943.4 on 5 and 805 DF, p-value:  最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

1万+

1万+

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言