Prophet Quick Start

数据格式

Prophet 的输入必须包含两列的数据框:ds 和 y 。

- ds 列必须包含日期(YYYY-MM-DD)或者是具体的时间点(YYYY-MM-DD HH:MM:SS)。

- y 列必须是数值变量,表示我们希望去预测的量。

example_wp_log_peyton_manning.csv下载地址:

import pandas as pd

from prophet import Prophet

# 读入数据集

df = pd.read_csv('data/example_wp_log_peyton_manning.csv')

print(df.tail(5))

"""

ds y

2900 2016-01-16 7.817223

2901 2016-01-17 9.273878

2902 2016-01-18 10.333775

2903 2016-01-19 9.125871

2904 2016-01-20 8.891374

"""

建模流程

通过使用辅助的方法 Prophet.make_future_dataframe 来将未来的日期扩展指定的天数,得到一个合规的数据框。

m = Prophet()

m.fit(df)

# 构建待预测日期数据框,periods = 365 代表除历史数据的日期外再往后推 365 天

horizon = 365

future = m.make_future_dataframe(periods=horizon)

future.tail(5)

"""

ds

3265 2017-01-15

3266 2017-01-16

3267 2017-01-17

3268 2017-01-18

3269 2017-01-19

"""

# 预测

forecast = m.predict(future)

# 通过 Prophet.plot 方法传入预测得到的数据框,可以对预测的效果进行绘图。

fig1 = m.plot(forecast)

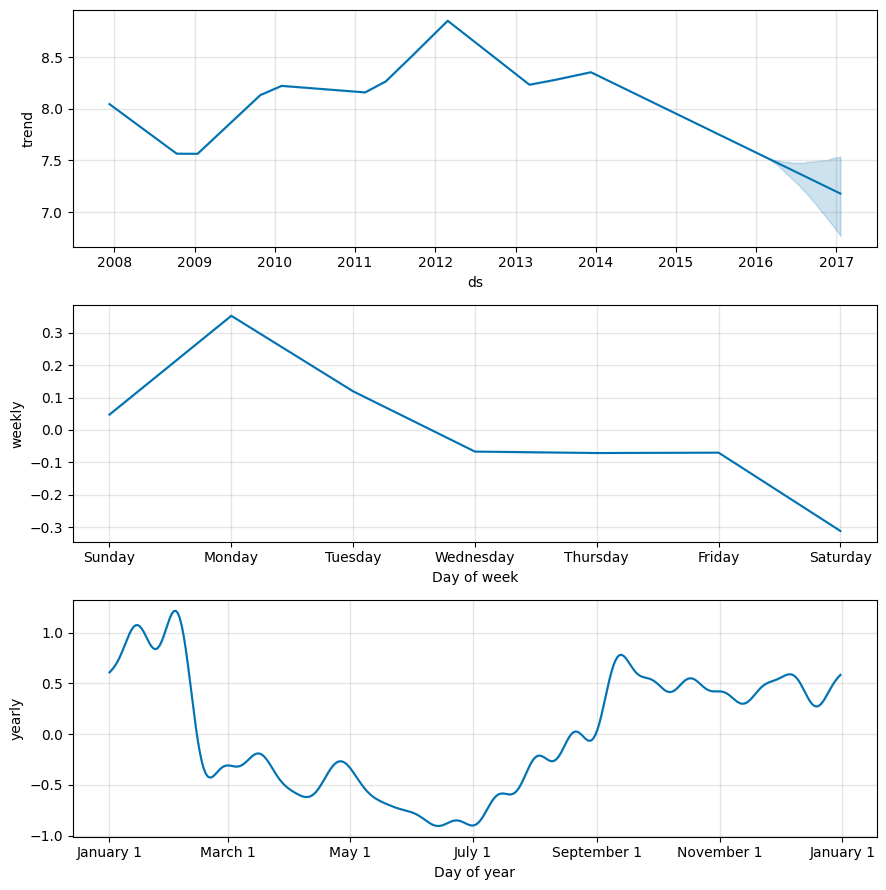

# 使用 Prophet.plot_components 方法。默认情况下,将展示趋势、时间序列的年度季节性和周季节性。如果之前包含了节假日,也会展示出来。

fig2 = m.plot_components(forecast)

如果想查看预测的成分分析,可以使用 Prophet.plot_components 方法。默认情况下,将展示趋势、时间序列的年度季节性和周季节性。如果之前包含了节假日,也会展示出来。

Prophet详解

在上一篇文章【Prophet代码实战(一)趋势项调节】介绍了Prophet算法的趋势项。接下来我们开始介绍Prophet算法的季节项

季节性

Prophet的内置季节性

-

yearly_seasonality,是否需要拟合数据中的yearly季节性,以及yearly季节性的傅里叶级数项数。当训练集中有超过1年的数据时,默认为10,

一般来说拟合yearly的季节性建议至少有一年的数据。 -

yearly_seasonality越大,拟合的季节性曲线波动幅度越大

-

yearly_seasonality=0或者为False时,表示不拟合yearly季节性。

-

类似还有weekly_seasonaliyt和daily_seasonality。

# 调整yearly_seasonality

m = Prophet(yearly_seasonality=20)

m.fit(df)

horizon = 365

future = m.make_future_dataframe(periods=horizon)

forecast = m.predict(future)

fig = m.plot_components(forecast)

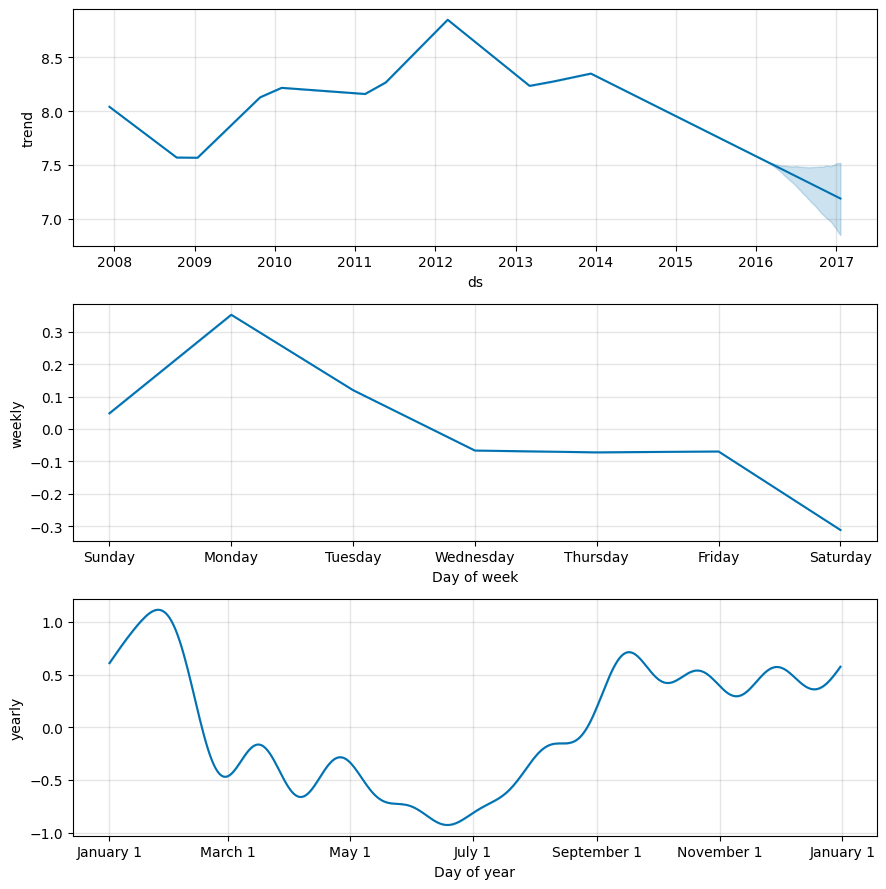

关闭yearly_seasonality

m = Prophet(yearly_seasonality=0)

m.fit(df)

horizon = 365

future = m.make_future_dataframe(periods=horizon)

forecast = m.predict(future)

fig = m.plot_components(forecast)

超参数seasonality_prior_scale

- 小数,季节性曲线的系数先验概率,默认值为10

- 理论上,seasonality_prior_scale越大,季节性曲线波动越大,越容易过拟合

# 调整seasonality_prior_scale = 10

m = Prophet(seasonality_prior_scale = 10)

m.fit(df)

horizon = 365

future = m.make_future_dataframe(periods=horizon)

forecast = m.predict(future)

fig = m.plot_components(forecast)

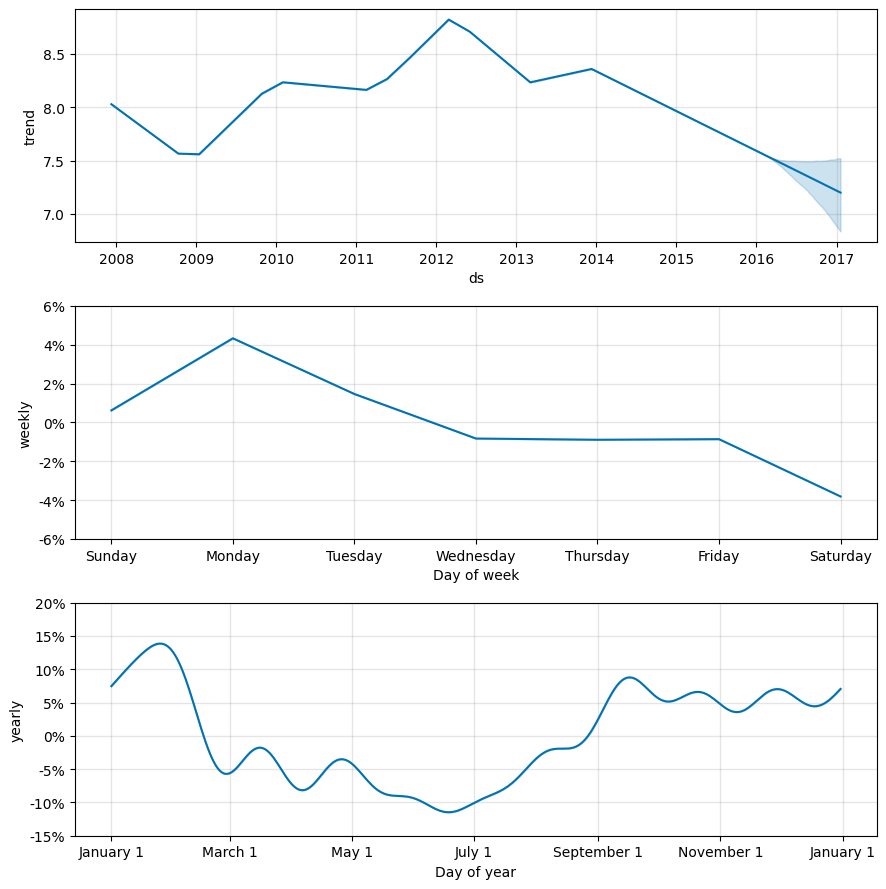

季节性的加法模式和乘法模式

超参数seasonality_mode

- “additive”:默认值,表示季节性对观测值是加法的作用,即y = trend + seasonality

- “multiplicative”:表示季节性对观测值是乘法作用,即y = trend * seasonality

- 一般business相关的时间序列只要选取"multiplicative"

- multiplicative和additive可以通过对数操作相互转化。即 y = trend * seasonality

可以表示为log(y) = log(trend) + log(seasonality)

# 调整seasonality_mode

m = Prophet(seasonality_mode="multiplicative")

m.fit(df)

horizon = 365

future = m.make_future_dataframe(periods=horizon)

forecast = m.predict(future)

fig = m.plot_components(forecast)

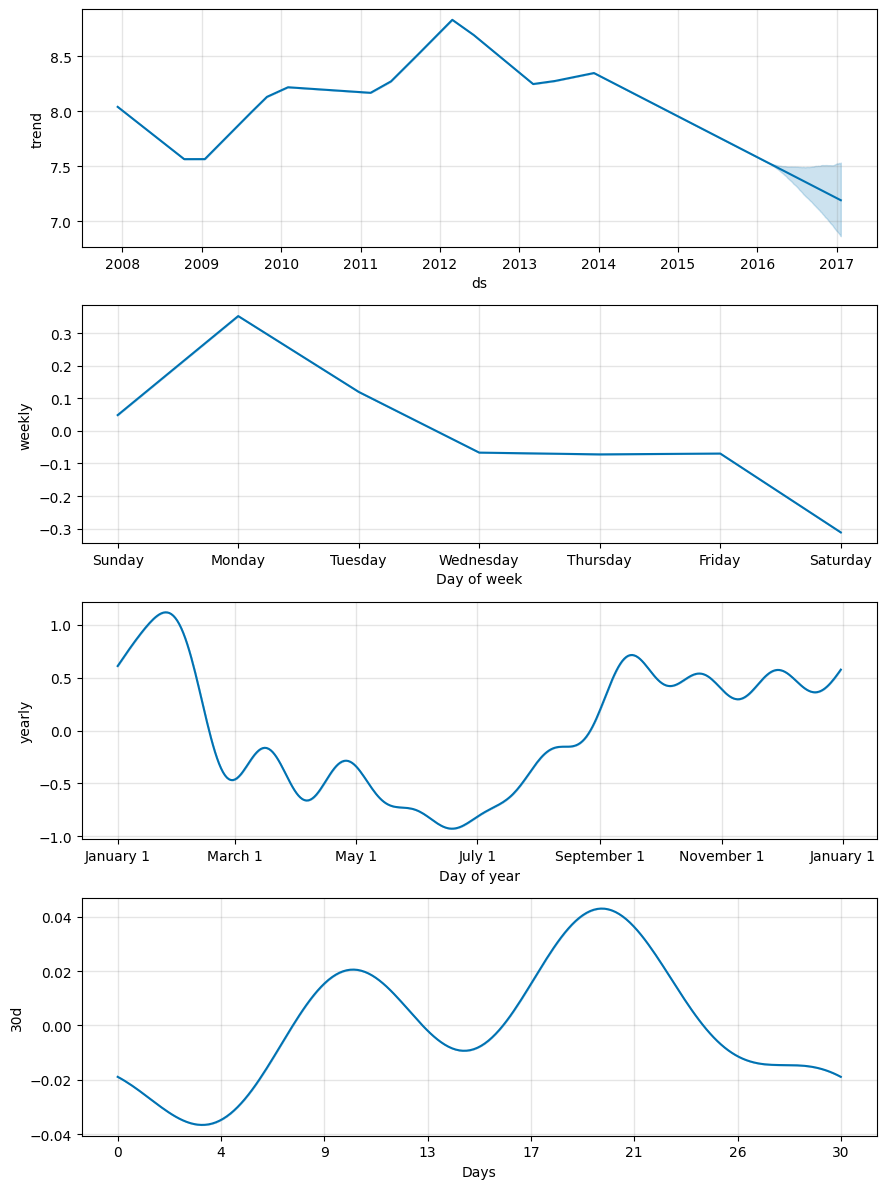

自定义季节性

通过函数add_seasonality()增加新的季节性,参数有:

- name:名称

- period:周期长度

- fourier_order:傅里叶级数项数

- prior_scale:傅里叶系数先验概率

# 通过函数add_seasonality()增加新的季节性

m = Prophet()

m.add_seasonality(name='30d',period=30,fourier_order=3,prior_scale=0.1)

m.fit(df)

horizon = 365

future = m.make_future_dataframe(periods=horizon)

forecast = m.predict(future)

fig = m.plot_components(forecast)

季节性的置信区间

超参数mcmc_samples,计算置信区间时的蒙特卡洛样本数量

- 默认情况下,Prophet只会返回趋势的置信区间,为了得到季节性的置信区间,我们需要做完全的贝叶斯抽样,采用是通过蒙特卡洛方法完成的。

- mcmc_samples越大,样本越具有代表性,置信区间越准,运算时间也会越久

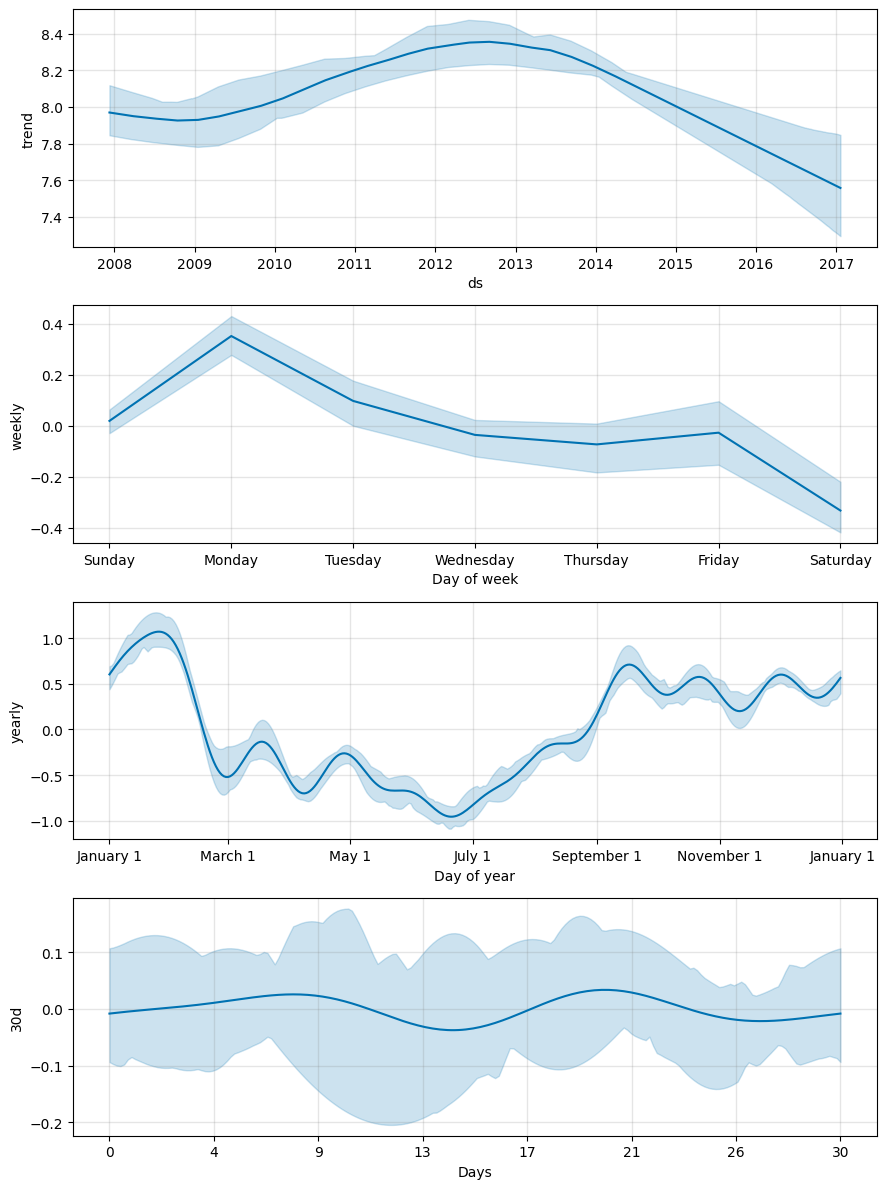

# 通过mcmc_samples参数返回季节性趋势

m = Prophet(mcmc_samples=30)

m.add_seasonality(name='30d',period=30,fourier_order=3,prior_scale=0.1)

m.fit(df)

horizon = 365

future = m.make_future_dataframe(periods=horizon)

forecast = m.predict(future)

fig = m.plot_components(forecast)

1051

1051

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言