最近几个做投资的小伙伴准备增加持仓中的量化中性产品。目前股指期货贴水深度收窄,甚至到了升水运行,这种情形下量化中性做空股指期货的成本低,有利于提升量化中性产品的收益。

为了搞清楚A股市场股指期货基差运行情形,我们几个小伙伴约银河证券的投资专家做了一次辅导讲座,讲清楚基差的定义、基差当前的运行情况、以及如何根据基差对量化中性产品、雪球产品做择时选择。

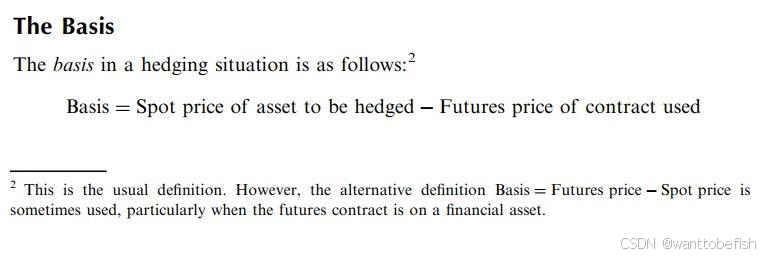

昨天的讲座PPT中,首先讲到商品期货中基差的定义为(见图1)

图1,商品期货基差的定义

商品期货基差=现货价格-期货价格

后来讲到股指期货的年化贴水率时,给出的公式是(见图2):

图2,股指期货基差的定义,更具体说是IC/IM年化贴水率定义

股指期货年化贴水率=(次月合约-当月合约)/现货价格*12

感觉上述两个公式的定义是反的,前者是现货价格减去期货;后者是期货价格减去现货。两者相比多了一个负号。

只有承认两种情况下基差的定义不一致,才能明确下面的陈述是对的:

“商品期货一般贴水运行,期货价格高于现货,因为有储存成本等因素;股指期货一般也是贴水运行,股指期货低于现货,或者远月合约低于近月合约。因为每年年报后,上市公司一般有分红除权等行为,导致看空未来股价”

为了搞清楚基差的定义在商品期货和股指期货市场中是否真的不一致,我想到了求助ChatGPT,以下是问答实录:

问:

基差=现货价格减去期货价格,以此对应,股指期货年化贴水率等于(次月合约-当月合约)/现货价格*12。是否商品期货中基差的定义和股指期货中基差的定义是反的,多了一个负号?

答:

不,商品期货和股指期货的基差定义是相同的,都是现货价格减去期货价格。在股指期货中,年化贴水率的计算公式为(次月合约-当月合约)/现货价格*12。这个公式与商品期货的基差定义没有负号。请注意,在两种情况下,基差可以是正数或负数,取决于现货价格与期货价格之间的关系。

问:

那么,股指期货中贴水的情形是什么?商品期货中贴水的情形又是什么?

答:

在股指期货中,如果次月合约的价格低于当月合约的价格,即(次月合约-当月合约)为负数,那么这被称为贴水情况。这表示市场预期股指未来会下跌或者供应过剩。 在商品期货中,贴水情况是指现货价格高于期货价格,即基差为正数。这通常发生在市场供应充足且需求有限的情况下,暗示着对该商品的现货供应量大于期货市场所需。 总之,贴水情况在不同市场和不同商品中具有不同的含义,但它们都表示了现货价格相对于期货价格的相对关系。

考虑到ChatGPT对英文的理解更准确,于是进一步有下面的问答过程。

问:

please say the last message in English and put more information

答:

Certainly! Here's the last message translated into English with additional information: In stock index futures, when the price of the next month's contract is lower than the current month's contract price, indicated by a negative value in (next month contract - current month contract), it is referred to as "being at a discount" or "in contango." This suggests that the market expects the stock index to decline in the future or there is an oversupply. In commodity futures, being at a discount refers to a situation where the spot price is higher than the futures price, resulting in a positive basis. This typically occurs when there is ample supply in the market and limited demand for the commodity, indicating that the current supply of the commodity exceeds the demand in the futures market. In both cases, whether in stock index futures or commodity futures, being at a discount reflects the relative relationship between the spot price and the futures price, providing insight into market expectations and supply-demand dynamics.

问:

基差=现货价格-期货价格;对商品期货来说,期货会贵一些,因为有存储等成本,所以基差一般为负数。 贴水:现货价格<期货价格,商品正常供求。 升水:现货价格>期货价格,市场出现短缺,供不应求 在你的PPT的第14页,股指期货年化贴水率的定义中 IC/IM年化贴水率=(次月合约-当月合约)/现货价格*12 这个股指期货年化贴水率的定义和商品期货基差的定义是反的。商品中是现货减去期货,估值期货基差相当于是期货减去现货。 只有承认商品期货和股指期货基差定义相反,才能保证下面表述正确: 商品期货一般贴水运行,期货价格高于现货;股指期货一般也是贴水运行,股指期货低于现货,或者远月合约低于近月合约。

答:

I apologize for the confusion. You are correct in your explanation. In commodity futures, the basis is calculated as the spot price minus the futures price. As there are costs associated with storage and other factors, the futures price tends to be higher, resulting in a negative basis. When the spot price is lower than the futures price, it is referred to as "backwardation" or being "at a discount." This typically reflects a normal supply-demand situation in the commodity market. On the other hand, when the spot price is higher than the futures price, it is known as "contango" or being "at a premium." This suggests a shortage in the market where demand exceeds supply. Regarding the definition of annualized contango rate for stock index futures from slide 14 of your presentation: IC/IM annualized contango rate = (next month contract - current month contract) / spot price * 12 You are right that the definitions of contango in commodity futures and the annualized contango rate in stock index futures are opposite. In commodities, the basis is calculated as spot price minus futures price, while in stock index futures, it is defined as futures price minus spot price. To clarify further, it is generally expected that commodity futures operate at a discount, with futures prices higher than spot prices. Similarly, stock index futures tend to operate at a discount, where the stock index futures price is lower than the spot price, or the price of far-month contracts is lower than that of near-month contracts.

昨天下午收到银河证券杨同学信息:

自衍生品入门必读教材 John C. Hull 的《Options, Futures, and Other Derivatives》提到,基差的定义是现货价格-期货价格,但是教材同时在附注2中明确指出:在标的为金融资产的情况下,基差往往定义为期货价格-现货价格。

同时给出了截图证明,见图3

图3,教科书中对商品期货基差的定义以及附注中关于财富资产情形下对基差定义的修正

股指基差为期货价格减去现货价格。股指情形一般是现货价格高于期货,因为有现金成本,另外,股指期货是有杠杆的,占用现金少。所以按这个股指基差定义,股指基差一般也为负数,也就是一般是贴水运行。

商品期货基差等于现货价格减去期货价格。因为存储成本等原因,期货价格高于现货,这种情形下,基差一般也是负数,也是贴水运行。

通过这一通问答,明白或者记住以下几个结论即可:

- 商品期货基差定义为现货价格减去期货;股指期货基差定义为期货价格减去现货。两种情形下,基差一般都为负数,贴水运行。

- 股指期货基差年化贴水率的定义中是次月减去当月。贴水如果为负数,而且越向下偏离水平轴(见图2),表示贴水越深。否则表示贴水收窄。水平轴以上运行表示升水。

- 股指期货贴水收窄时,有利于量化中性产品,因为其要求做空股指期货。股指期货贴水收窄甚至升水时,量化中性策略付出的成本低,有利于策略提升收益率。与此对应,股指期货基差深度贴水时,有利于雪球产品,因为其要求做多股指期货,深度贴水时,成本低,雪球产品给出的票息高。

- 目前时间窗口内,IC/IM年化贴水率收窄甚至升水运行,有利于量化中性策略产品

1651

1651

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言