持续行动1期 52/100,“AI技术应用于量化投资研究”。

今天聊聊backtrader——号称最强大的“工业级”单机版量化框架。可能需要一系列的文章能把这个讲清楚,不只是简单使用,要改造成适合A股市场,电子货币实盘,接入机器学习生态等。

版本1.9,比较成熟,海外很多机构在用,而且支持实盘,支持电子货币等。

我比较看重实盘、生态。所以值得系统学习一下,并整合进我们的投研生态中。backtrader本身包很小,才420k左右,而且依赖包也不多,不像qlib,很多用户估计安装都有些许困难。

写一个简单的量化回测框架很简单,但要把问题考虑全,对上下游生态的整合,并不容易。而且要知道,我们的核心是策略,策略,策略(因子)。

backtrader是否方便整合机器学习生态,这个有待深入研究。

另外backtrader有一个缺点,就是代码比较难懂。这是我一直对这个框架没有提上日程的原因。但仔细一想,我们真正要改框架的地方不会太多,qlib很容易看懂,我也只是复用过它的代码,并没有扩展和修改过它的组件。

安装指令:pip install backtrader。

文档地址:https://www.backtrader.com/docu/quickstart/quickstart/

01 数据源

首先要解决的就是数据源的问题。

官网上的示例使用yahoofinance,国内访问不稳定,而且使用的示例数据也是美股,给我们的感觉是不太熟悉。

backtrader支持PandasData就是Dataframe,这就好办了。

最简单的,就是从本地加载csv,而本地数据我早就准备好了。

这是一个通用的datafeed_csv.py(大家从gitee ailabx可以下载)

# encoding:utf8

import os

import pandas as pd

from loguru import logger

class CSVDatafeed:

def __init__(self):

self.code_dfs = {}

def add_data(self, code, csv_file):

if not os.path.exists(csv_file):

logger.error('{}csv文件不存在!'.format(code))

return

df = pd.read_csv(csv_file)

if len(df) == 0:

logger.error('{}没有数据!'.format(code))

return

for col in ['date']:

if col not in df.columns:

logger.error('{}字段{}不存在!'.format(code, col))

return

df['code'] = code

df['date'] = df['date'].apply(lambda x: str(x))

df.sort_values(by='date', inplace=True)

df['rate'] = df['close'].pct_change()

df['equity'] = (df['rate']+1).cumprod()

self.code_dfs[code] = df

def get_df(self, instrument):

if instrument in self.code_dfs.keys():

df = self.code_dfs[instrument]

df.index = df['date']

return df

else:

logger.info('{}未加载'.format(instrument))

return None

def get_all_df(self):

df_all = pd.concat(self.code_dfs.values(), axis=0)

df_all.dropna(inplace=True)

df_all.index = df_all['date']

df_all.sort_index(inplace=True)

return df_all

if __name__ == '__main__':

from engine.config import DATA_DIR_CSV

feed = CSVDatafeed()

code = '000300.SH'

feed.add_data(code, DATA_DIR_CSV.joinpath('{}.csv'.format(code)))

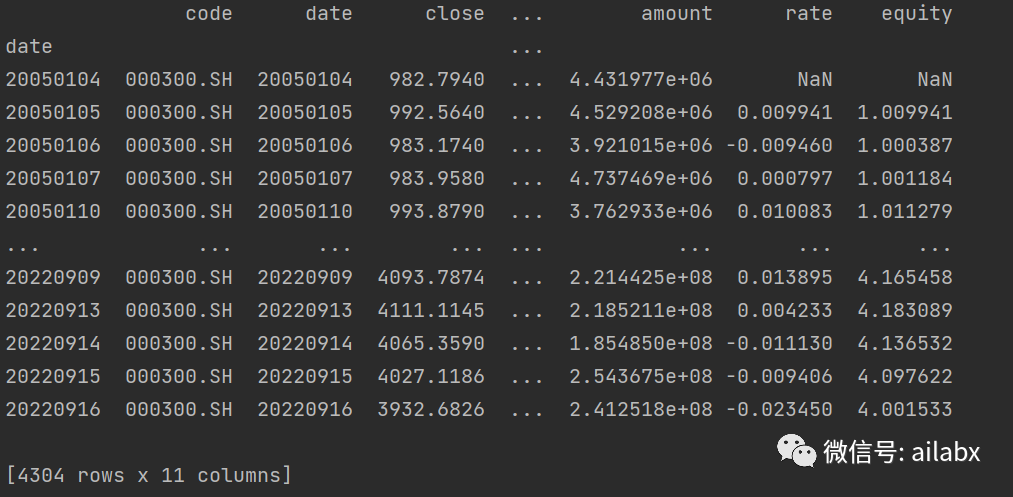

df = feed.get_df(code)

print(df)

读出沪深300指数如下:

数据规整成backtrader格式,

index转为datetime格式,加一列openinterest(这个是期货里的概念,未平仓合约,不知为何要作为必选列,没有就置为0即可),然后把不需要的列去掉。

def to_backtrader_dataframe(df):

df.index = pd.to_datetime(df.index)

df['openinterest'] = 0

df = df[['open', 'high', 'low', 'close', 'volume', 'openinterest']]

return df

02 均线策略

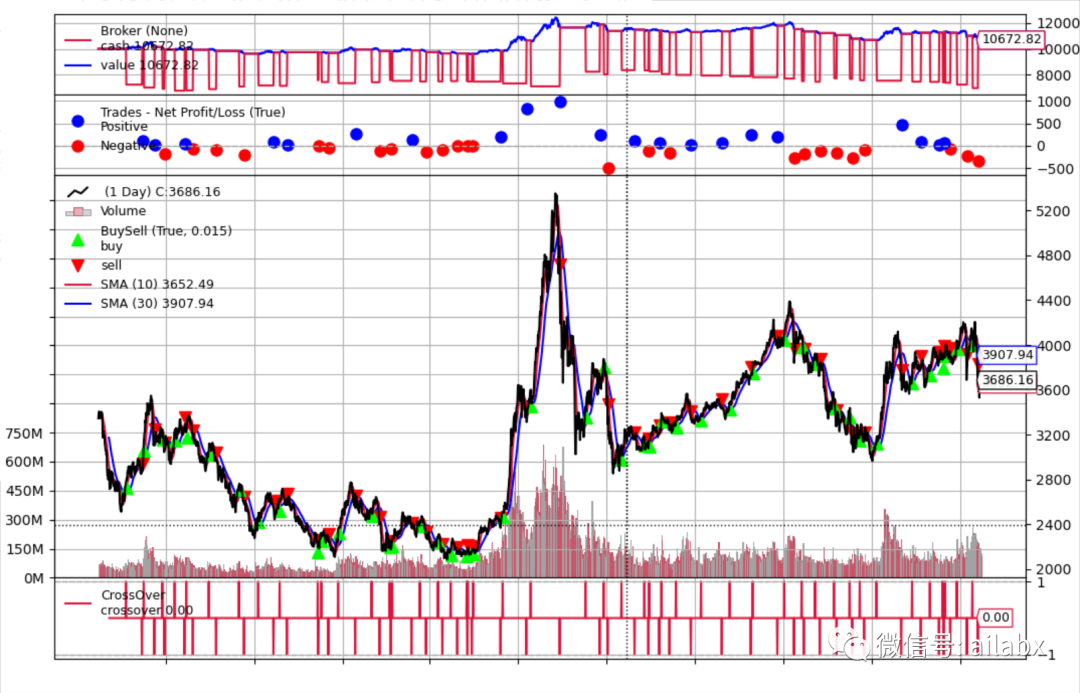

这是官网的第一个策略,一般用来测试系统,快线MA10与慢线MA30之间,金叉时买入,死叉时卖出。

class SmaCross(bt.Strategy):

# list of parameters which are configurable for the strategy

params = dict(

pfast=10, # period for the fast moving average

pslow=30 # period for the slow moving average

)

def __init__(self):

sma1 = bt.ind.SMA(period=self.p.pfast) # fast moving average

sma2 = bt.ind.SMA(period=self.p.pslow) # slow moving average

self.crossover = bt.ind.CrossOver(sma1, sma2) # crossover signal

def next(self):

if not self.position: # not in the market

if self.crossover > 0: # if fast crosses slow to the upside

self.buy() # enter long

elif self.crossover < 0: # in the market & cross to the downside

self.close() # close long position

看样子没有亏,这张图后面会细说,只是先演示一下用法。

另外这里使用的matplotlib的版本==3.2.2,高版本会报错。

另外我们可以有bokeh的web版本的可视化,这个后续的文章再聊。

这只是演示系统功能的例子。

这也是回测的好处,很多讲技术分析的书,一上来什么均线策略,你回测一下就知道均线策略有没有用——买来卖去十年赚了600多块钱——还好就是至少没亏。

几个细节:

一、买卖模式,使用buy/close根据信号来开仓/平仓

if not self.position: # not in the market

if self.crossover > 0: # if fast crosses slow to the upside

self.buy() # enter long

elif self.crossover < 0: # in the market & cross to the downside

self.close() # close long position

二、目标仓位模式,order_target_size(仓位比例)

def next(self):

if not self.position: # not in the market

if self.crossover > 0: # if fast crosses slow to the upside

self.order_target_size(target=1) # enter long

elif self.crossover < 0: # in the market & cross to the downside

self.order_target_size(target=0) # close long position

三、交易信号模式,把crossover添加为交易信号,就不需要实现next函数了,这个功能特别有用——尤其是我们要整合机器学习时。模型就是输出交易信号。

需要继承自bt.SignalStrategy

def __init__(self):

sma1 = bt.ind.SMA(period=self.p.pfast) # fast moving average

sma2 = bt.ind.SMA(period=self.p.pslow) # slow moving average

crossover = bt.ind.CrossOver(sma1, sma2) # crossover signal

self.signal_add(bt.SIGNAL_LONG, crossover) # use it as LONG signal

backtrader不好调试的地方,如果你想看下crossover到底是啥,debug进去,看到这样的东西,还是找不到数据。它用了大量的元编程,让我们访问数据很方便,但你想看到内存中的数据就不容易了。

03 数据序列DataSeries

要自己写策略,next函数(其他框架里加onbar),正确读取DataSeries里的数据。bt框架里使用0下标访问当前值,而且会自动走next(onbar),这一点很方便——但也是一开始不好理解的地方。

明天继续。

反思

大部分事情一开始是想不清楚细节的,一个模糊的正确的方向即可,然后朝着这个方向前进。而且直奔核心而去。比如你要开一家煎饼摊,最重要就是做出煎饼,口味很重要,至于品牌,营销都是之后的事情。

对于量化而言,策略是第一位的。

找一个框架,能让你的策略快速落地;更进一步,生态全,能够很快找到各个策略加以改进。

993

993

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言