目录

一、高斯混合模型的核心原理

1.1 概率生成过程解析

给定数据集X,GMM假设数据由k个高斯分布混合生成:

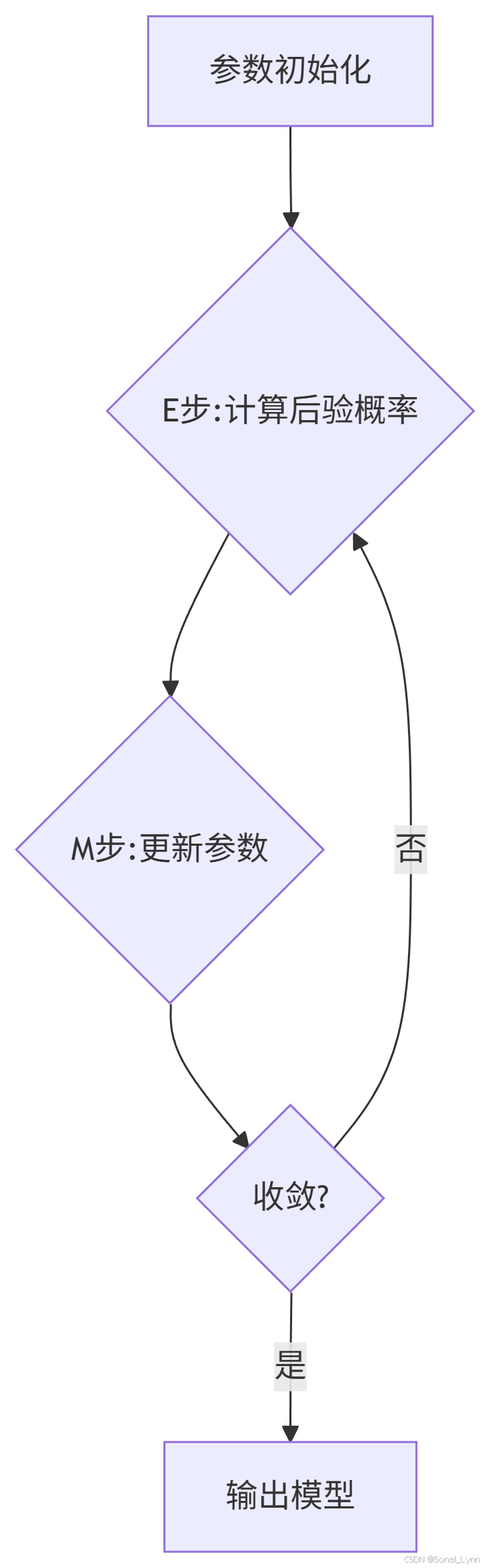

1.2 EM算法迭代过程

二、Scikit-Learn实战:从基础到进阶

2.1 基础建模与可视化

from sklearn.mixture import GaussianMixture

import matplotlib.pyplot as plt

import numpy as np

# 生成模拟数据

np.random.seed(42)

X1 = np.random.normal(0, 1, (300, 2))

X2 = np.random.normal(5, 1.5, (700, 2))

X = np.vstack([X1, X2])

# 训练GMM模型

gmm = GaussianMixture(n_components=2, covariance_type='full')

gmm.fit(X)

# 可视化决策边界

x_min, x_max = X[:,0].min()-1, X[:,0].max()+1

y_min, y_max = X[:,1].min()-1, X[:,1].max()+1

xx, yy = np.meshgrid(np.linspace(x_min, x_max, 100),

np.linspace(y_min, y_max, 100))

Z = -gmm.score_samples(np.c_[xx.ravel(), yy.ravel()])

Z = Z.reshape(xx.shape)

plt.contourf(xx, yy, Z, levels=20, cmap='viridis')

plt.scatter(X[:,0], X[:,1], s=5, c='white')

plt.title("GMM概率密度分布")

plt.colorbar(label='负对数概率密度')2.2 协方差类型对比实验

cov_types = ['spherical', 'tied', 'diag', 'full']

plt.figure(figsize=(15,10))

for i, cov_type in enumerate(cov_types):

gmm = GaussianMixture(n_components=2, covariance_type=cov_type)

gmm.fit(X)

# 获取椭圆参数

if cov_type == 'spherical':

widths = heights = 2 * np.sqrt(gmm.covariances_)

else:

from scipy.stats import multivariate_normal

widths, heights = [], []

for cov in gmm.covariances_:

v, _ = np.linalg.eigh(cov)

widths.append(2*np.sqrt(v[0]))

heights.append(2*np.sqrt(v[1]))

plt.subplot(2,2,i+1)

plt.scatter(X[:,0], X[:,1], s=5, c=gmm.predict(X))

for j in range(len(gmm.means_)):

plt.gca().add_patch(plt.Ellipse(gmm.means_[j], widths[j], heights[j],

angle=0, alpha=0.3))

plt.title(f'Covariance Type: {cov_type}')三、工业级异常检测实战

3.1 信用卡欺诈检测

from sklearn.preprocessing import RobustScaler

from sklearn.metrics import classification_report

# 数据预处理

scaler = RobustScaler()

X_trai 最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

575

575

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言