Interest rates affect economic activities at all levels. Central banks, including the Federal Reserve (informally known as the Fed), target interest rates as a policy tool to influence economic activity. Interest rate derivatives利率衍生品 are popular with investors who require customized cash flow needs or specific views on interest-rate movements.

One of the key challenges that interest-rate derivative traders face is to have a good and robust pricing procedure for these products. This involves understanding the complicated behavior of an individual interest-rate movement. Several interest-rate models have been proposed for financial studies. Some common models studied in finance are the Vasicek, CIR, and Hull-White models. These interest-rate models involve modeling the short-rate and rely on factors (or sources of uncertainty) with most of them using only one factor. Two-factor and multi-factor interest rate models have been proposed.

In this chapter, we will cover the following topics:

- Understanding yield curves

- Valuing a zero-coupon bond

- Bootstrapping a yield curve

- Calculating forward rates远期利率

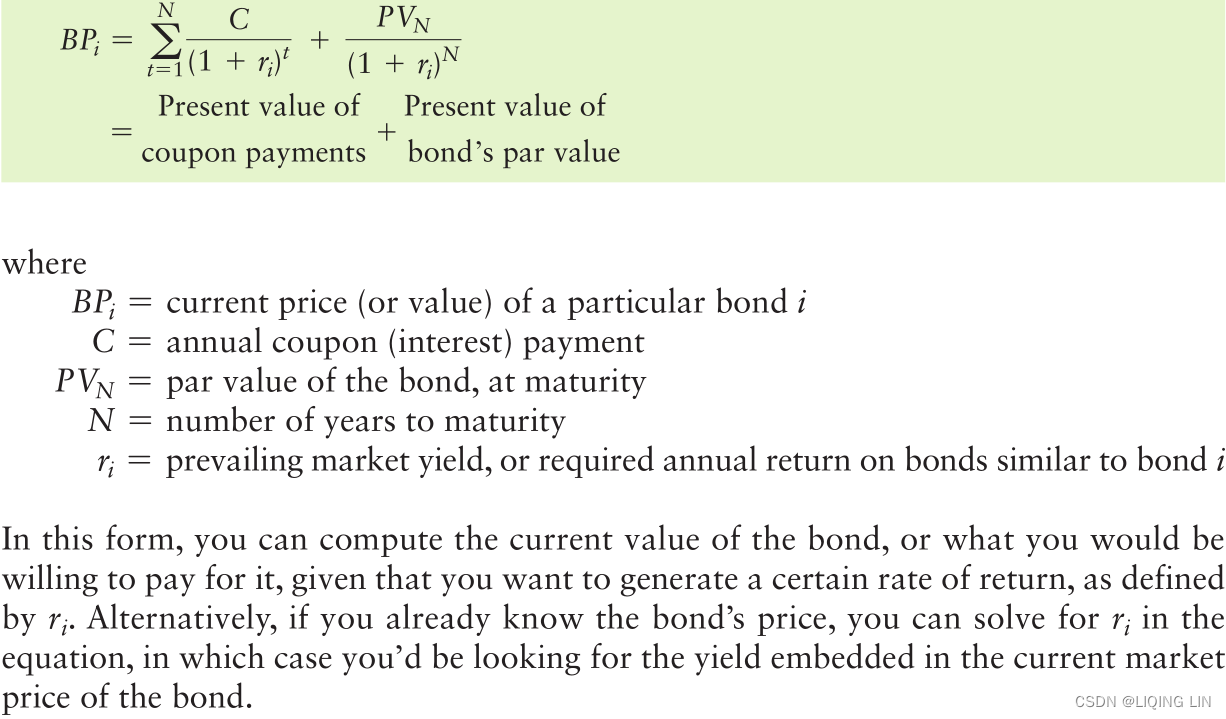

- Calculating the yield to maturity and price of a bond债券的到期收益率和价格

- Calculating the bond duration and convexity using Python

- Short-rate modeling

- The Vasicek short-rate model

- Types of bond options

- Pricing a callable bond option为可赎回债券期权定价

Fixed-income securities固定收益证券

Corporations and governments issue fixed-income securities as a means of raising money筹集资金.

- The owners of such debts lend money and expect to receive the principal when the debt matures.

- The issuer who wishes to borrow money may issue支付 a fixed amount interest payment during the lifetime of the debt at pre-specified times.

The holders of debt securities, such as US Treasury bills美国国库券, notes票据, and bonds, face the risk of default by the issuer. The federal government and municipal( /mjuːˈnɪsɪp(ə)l/ 城市的,市政的) government are thought to face the least default risk, since they can easily raise taxes and create more money to repay the outstanding debts.

Most bonds pay a fixed amount of interest semi-annually(/ ˈsemi ˈænjuəli /每半年一次), while some pay quarterly, or annually. These interest payments are also referred to as coupons息票. They are quoted as a percentage of the face value or par/ pɑːr / amount面值 of the bond on an annual basis.

For example, a 5-year $10,000 Treasury bond国债 with a coupon rate of 5% pays coupons of $500 each year, or coupons of $250 every 6 months, up to and including the maturity date. Should the interest rates drop and new T-bonds pay a 3% coupon rate, the buyer of the new bond will only receive coupons of $300 annually, while existing holders of the 5% bond will continue to receive $500 annually. As the characteristics of the bonds influence their prices, they're closely related to current levels of interest rates in an inverse way:

- the value of the bond decreases as the interest rates increase.

- As interest rates decrease, bond prices increase.

Yield curves收益率曲线

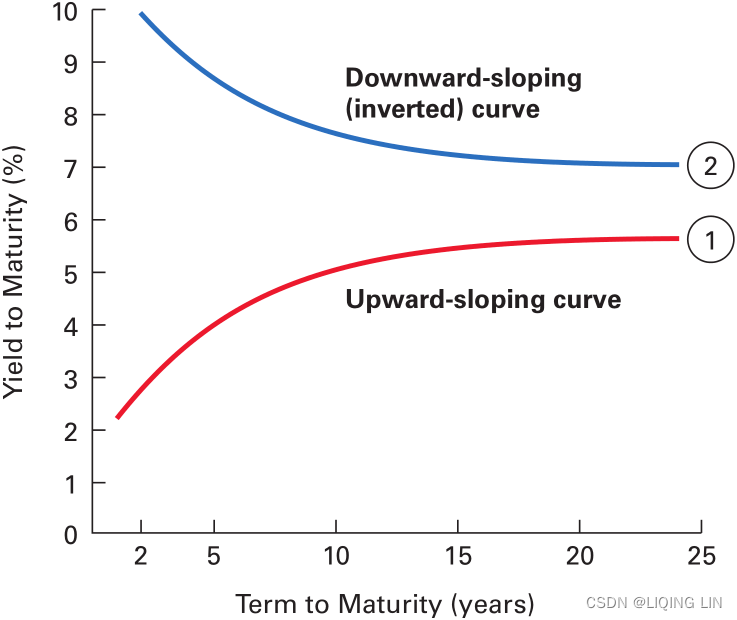

In a normal yield curve environment, long-term interest rates are higher than short-term interest rates. Investors expect to be compensated with higher returns when they lend money for a longer period since they are exposed to a higher default risk. The normal or positive yield curve is said to be upward sloping, as shown in the following graph:

In certain economic conditions, the yield curve can be inverted. Long-term interest rates are lower than short-term interest rates. Such a condition occurs when the supply of money is tight. Investors are willing to forgo(/ fɔːrˈɡoʊ /放弃) long-term gains to preserve their wealth in the short-term. During periods of high inflation, where the inflation rate exceeds the rate of coupon interests, negative interest rates may be observed. Investors are willing to pay in the short-term just to secure their long-term wealth. The inverted yield curve is said to be downward sloping, as shown in the following graph:

Valuing a zero-coupon bond估值零利息债券

##################

Compound interest

Compound interest is interest calculated on the initial principal and also on the accumulated interest of previous periods of a deposit or loan. The effect of compound interest depends on frequency.

Assume an annual interest rate of 12%. If we start the year with $100 and compound only once, at the end of the year, the principal grows to $112 ( = $112). Interest applied only to the principal is referred to as simple interest.

compounded monthly, n =12:

If we instead compound each month at 1%(monthly-compounded yield=), we end up with more than $112 at the end of the year(T=1 year). That is,

=112.68. (It's higher because we compounded more frequently.)

- The future value (FV) of an investment of present value (PV or P) dollars earning interest at an annual rate of r compounded n times per year for a period of T years is

- P: the principal, the amount invested, or present value (PV)

- r: the annual rate (in decimal form),

- n: the number of times it is compounded or compound frequency.

is the interest per compounding period

- T: the number of year

: is the number of compounding periods

If we known the monthly-compounded yield is 1%, and the value is $112.68 after one year, we want to calculate the present value:

Continuously compounded returns compound the most frequently of all. Continuous compounding is the mathematical limit that compound interest can reach. It is an extreme case of compounding since most interest is compounded on a monthly, quarterly, or semiannual basis.

##################http://www.math.iupui.edu/~momran/m119/old/ch4h.htm

- C = the periodic coupon payment

or is the coupon dollar amount paid at each time point T (T=1, 2, ..., nt)

if n = 1

0 ~ T1 ~ T2 ~ ... ~ t

| |

| C | |

| ... C |

| ...

| ... C - y = the yield to maturity (YTM)

- n: the number of times it is compounded

or the coupon payment frequency.

if n=1, then C = C : the coupon dollar amount paid at each time point T (T=1, 2, ..., t)

if n>1, then C = C/n : the coupon dollar amount paid at each time point T (T=1, 2, ..., nt)

: the yield per compounding period

- T = the time period of payment (in years), T=1, 2, ..., t

- t : the bond's maturity date

= the remaining number of periods from until the bond's maturity date t

A zero-coupon bond is a bond that does not pay any periodic interest(C=0) except on maturity(n=1), where the principal or face value is repaid. Zero-coupon bonds are also called pure discount bonds纯贴现债券.

A zero-coupon bond can be valued as follows:![]()

Here, y is the annually-compounded yield年复合收益率 or rate of the bond, and t is the time remaining to the maturity of the bond. Let's take a look at an example of a five-year zero-coupon bond with a face value of $100. The yield is 5%, compounded annually. The price can be calculated as follows: ![]()

A simple Python zero-coupon bond calculator can be used to illustrate this example:

def zero_coupon_bond( par, y, t):

"""

Price a zero coupon bond.

:param par: face value of the bond.

:param y: annual yield or rate of the bond.

:param t: time to maturity, in years.

"""

return par/(1+y)**tUsing the preceding example, we get the following result:

print( zero_coupon_bond(100, 0.05, 5) ) ![]()

In the preceding example, we assumed that the investor is able to invest $78.35 at the prevailing(/ prɪˈveɪlɪŋ 现存的,现行) annual interest rate of 5% for 5 years, compounded annually.

Now that we have a zero-coupon bond calculator, we can use it to determine zero rates by bootstrapping引导 the yield curve, as explained in the next section.

#######################

effective interest rate

The effective interest rate is calculated as if compounded annually. The effective rate is calculated in the following way, where is the effective annual rate,

- r the nominal rate, and

- n the number of compounding periods per year (for example, 12 for monthly compounding):

For example, a nominal interest rate of 6% compounded monthly is equivalent to an effective interest rate of 6.17%.

When the frequency of compounding is increased up to infinity (as for many processes in nature) the calculation simplifies to:

If we increase the compound frequency to its limit, we are compounding continuously. While this may not be practical, the continuously compounded interest rate offers marvelously convenient properties. It turns out that the continuously compounded interest rate is given by:

note:

- P: the principal, the amount invested, or present value (PV)

- r: the annual rate (in decimal form),

- T: the number of year

- n: the number of times it is compounded or compound frequency in each T.

the interest rate is compounded n times per year - n*T: is the total number of compounding

When interest is compounded more frequently, the amount of interest earned in each increment of time becomes smaller, but the total amount of accumulated interest grows faster

What's so great about the continuously compounded rate (or return) that we will denote with ? First, it's easy to scale it forward. Given a principal of (P), our final wealth over (T) years is given by:

If the interest is compounded continuously for T years at a rate of

per year, then the compounded amount is given by

Note that e is the exponential function. For example, if we start with $100 and continuously compound at 8% over three years, the final wealth is given by:

=

![]()

Discounting to the present value (PV or p) is merely compounding in reverse, so the present value of a future value (FV) compounded continuously at a rate of () is given by:

PV of FV received in (n) years

#######################Continuous Compound Interest

Spot and zero rates

As the compounding frequency increases (say, from compounded yearly to compounded daily), the future value of money reaches an exponential limit指数极限. That is to say, the value of $100 today will reach a future value of $100* when it is invested at a continuously compounded rate, R, for a period of time, T. If we discount these values for a security that pays $100 at a future time, T, with a continuously-compounded discount rate, R, its value at time 0 is

. This rate is known as the spot rate即期利率.需要注意得是,即期利率不是一个能够直接观察到的市场变量,而是一个基于现金流折现法,通过对市场数据进行分析而得到的利率。

Spot rates represent the current interest rates for several maturities, should we want to borrow or lend money now. Zero rates( called zero-coupon interest rate or spot rate) represent the internal rate of return of zero-coupon bonds.

By deriving the spot rates of bonds with different maturities, we can construct the present yield curve through a bootstrapping引导 process using zero-coupon bonds.

Bootstrapping a yield curve引导收益率曲线

Short-term spot rates短期即期利率 can be derived directly from various short-term securities, such as zero-coupon bonds, T-bills国库券, notes, and eurodollar deposits欧洲美元存款. However, longer-term spot rates are typically derived from the prices of long-term bonds through a bootstrapping process, taking into account the spot rates of maturities that correspond to the coupon payment date. After obtaining short-term and long-term spot rates, the yield curve can then be constructed.

An example of bootstrapping the yield curve

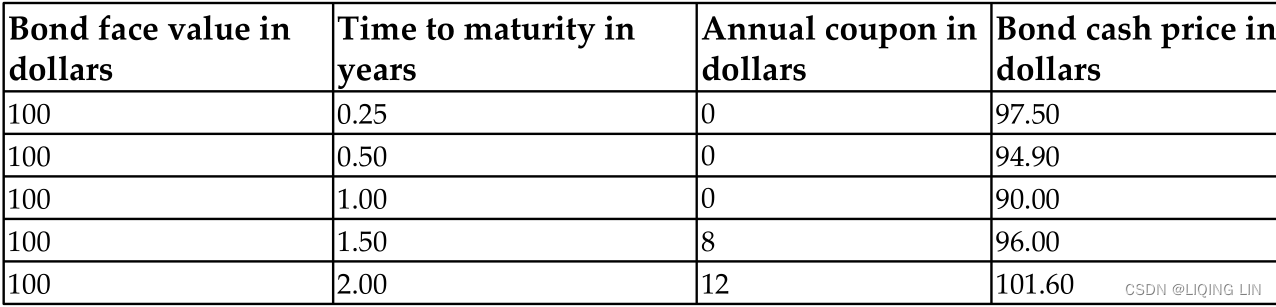

Let's illustrate the bootstrapping of the yield curve with an example. The following table shows a list of bonds with different maturities and prices:

When T<=1 year, then C=0 Annual coupon (interest in dollars) payment

When T<=1 year, then C=0 Annual coupon (interest in dollars) payment

![]() is replace with

is replace with , and N==T, and R is the sport rate

if n=1 ==>

OR

==>

==>

An investor in a three-month zero-coupon(interest payment C=0) bond today at $97.50 would earn interest of $2.50. The three-month spot rate can be calculated as follows:

Thus, the 3-month zero rate is 10.127% with continuous compounding. The spot rates of the zero-coupon bonds are shown in the following table:

import numpy as np

def spot_rate( price, T, par=100 ):

return np.log(par/price)/T

print( "0.25 year's Sport rate:{:.5f}".format( spot_rate( 97.5, 0.25, par=100 ) ) )

print( "0.5 year's Sport rate(:{:.5f}".format( spot_rate( 94.9, 0.5, par=100 ) ) )

print( "1 year's Sport rate:{:.5f}".format( spot_rate( 90, 1., par=100 ) ) ) ![]()

Using these spot rates, we can now price the 1.5-year bond (> 1year) as follows:

C = semi-annual coupon (interest) payment = 8/round(1.5) = 8/2 =4==>

![]()

The value of y (annual yield or rate of the bond) can easily be solved by rearranging the equation, as follows:

With the spot rate of the 1.5-year bond as 10.681%, we can use it to price the 2-year bond with coupons of $6 semi-annually, as follows:

C/2 = semiannual coupon payment = 12/2=6

![]()

Rearranging the equation and solving for y gives us the spot rate of the 2-year bond as 10.808.

Through this iterative procedure of calculating the spot rate of every bond in increasing order of maturity and using it in the next iteration, we obtain a list of spot rates of different maturities that we can use to construct the yield curve.

the yield curve bootstrapping class

The steps for writing the Python code to bootstrap the yield curve and running with a plot output are outlined as follows:

import math

class BootstrapYieldCurve( object ):

def __init__(self):

self.zero_rates = dict() # self.zero_rates[T] = spot_rate

self.instruments = dict() # self.instruments[T] = (par, coup, price, compounding_freq)

################## step 1 ##################

def add_instrument( self, par, T, coup, price, compounding_freq=2 ):

# par : face value of the bond

# price : current price of the bond

# T as key : indexed by the maturity time T

self.instruments[T] = (par, coup, price, compounding_freq)

def get_maturities( self ):

# return: a list of maturities Ts of added instruments in ascending order

return sorted( self.instruments.keys() )

# calculate the spot rate of a zero-coupon bond(interest payment=0)

# This method is called by bootstrap_zero_coupons()

def zero_coupon_spot_rate(self, par, price, T):

# return: the zero coupon spot rate with continuous compounding

spot_rate = math.log( par/price ) / T

return spot_rate

################## step 3 ##################

# calculate the annual yield rate of the bond when interest payment=0

# OR

# spot rates: zero-coupon interest rate or Zero rates

# calculate the spot rates of the given zero-coupon bonds(interest payment=0)

# and adds them to the zero_rates dictionary, indexed by maturity.

def bootstrap_zero_coupons( self ):

# Bootstrap the yield curve with zero coupon(interest payment=0) instruments first.

for (T, instrument ) in self.instruments.items():

# self.instruments[T] = (par, coup, price, coumpounding_freq)

par, coup, price, freq = instrument

if coup==0:

# the annual yield or rate of the bond when interest payment=0

spot_rate = self.zero_coupon_spot_rate( par, price, T )

self.zero_rates[T] = spot_rate

# calculate the spot rate at a particular maturity period T

def calculate_bond_spot_rate( self, T, instrument ):

try:

# par : face value of the bond

par, coup, price, freq = instrument

periods = T*freq # 1.5 years * (1/0.5) = 1.5 * 2 = 3

# 2 years * (1.0.5) = 2 *2 = 4

# 8/2=4, 12/2=6 if freq=2

per_coupon = coup/freq # annual coupon payment/frequent

value = price # current bond price

for i in range( int(periods)-1 ): # if freq=2

t = (i+1)/float(freq) # 1/2 = 0.5, 2/2 = 1, 3/2 =1.5, ...

# self.zero_rates[T] : def bootstrap_zero_coupons( self )

spot_rate = self.zero_rates[t]

# Coupon payment / e^( R*t )

discounted_coupon = per_coupon * math.exp(-spot_rate*t)

# value = current bond price

value -= discounted_coupon

# last_period == maturity T

last_period = int(periods)/float(freq) # 3//2 = 1.5, 4//2=2.0

spot_rate = -math.log( value/(par+per_coupon) )/last_period

return spot_rate

except:

print("Error: spot rate not found for T=",t)

################## step 4 ##################

# calculate the annual yield rate of the bond when interest payment !=0

# spot rates: zero-coupon interest rate or Zero rates

# calculate the spot rates of non zero-coupon bonds(interest payment !=0)

# and adds them to the zero_rates dictionary, indexed by maturity T.

def get_bond_spot_rates(self):

"""

Get spot rates implied by bonds, using short-term instruments.

# par : face value of the bond

"""

for T in self.get_maturities(): # T_list in ascending order

instrument = self.instruments[T]

# self.instruments[T] = (par, coup, price, coumpounding_freq)

par, coup, price, freq = instrument

if coup !=0 :

spot_rate = self.calculate_bond_spot_rate(T, instrument)

self.zero_rates[T] = spot_rate

################## step 2 ##################

def get_zero_rates( self ):

# calculate the annual yield rate of the bond when interest payment=0

self.bootstrap_zero_coupons()

# calculate the annual yield rate of the bond when interest payment!=0

self.get_bond_spot_rates()

# return a list of zero rates in ascending order of maturity..

# self.get_maturities() : # T_list in ascending order

return [ self.zero_rates[T] for T in self.get_maturities() ] Instantiate the BootstrapYieldCurve class and add each bond's information from the preceding table:

yield_curve = BootstrapYieldCurve()

# (par, T, coup, price, compounding_freq=2 )

yield_curve.add_instrument(100, 0.25, 0., 97.5)

yield_curve.add_instrument(100, 0.5, 0., 94.9)

yield_curve.add_instrument(100, 1.0, 0., 90.)

yield_curve.add_instrument(100, 1.5, 8, 96., 2)

yield_curve.add_instrument(100, 2., 12, 101.6, 2)

ys = yield_curve.get_zero_rates()

ys

==>

==>==>

==>

![]() ==>

==>

xs = yield_curve.get_maturities()

xs ![]()

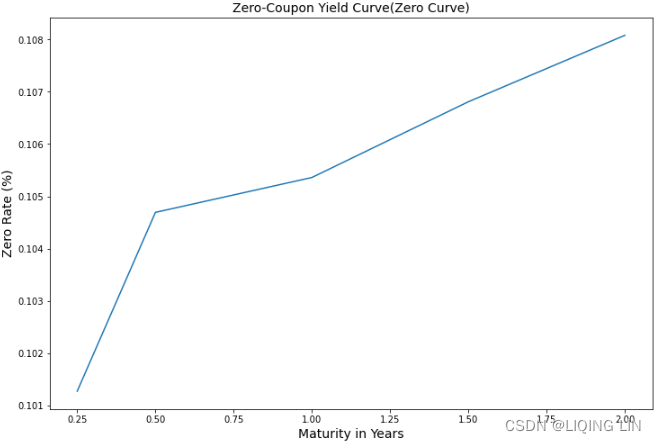

Calling the get_zero_rates() method in the class instance returns a list of spot rates in the same order as the maturities, which are stored in the x and y variables, respectively. Issue the following Python code to plot x and y on a graph:

%matplotlib inline

import matplotlib.pyplot as plt

fig = plt.figure( figsize=(12,8) )

plt.plot(xs,ys)

plt.title("Zero-Coupon Yield Curve(Zero Curve)", fontsize=14)

plt.ylabel( "Zero Rate (%)", fontsize=14 )

plt.xlabel( "Maturity in Years", fontsize=14 )

plt.show()

In a normal yield curve environment, where the interest rates increase as the maturities increase, we obtain an upward-sloping yield curve.

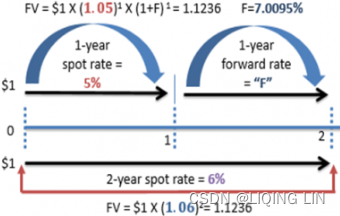

Forward rates远期利率

############################

The forward rate is the future yield on a bond. It is calculated using the yield curve.

We are trying to find the future interest rate for time period

,

and

expressed in years, given

- the rate

for time period

- and rate

for time period

.

To do this, we use the property that the proceeds from

- investing at rate

- and then reinvesting those proceeds at rate

for time period

- is equal to the proceeds from investing at rate

depends on the rate calculation mode (simple, yearly compounded or continuously compounded), which yields three different results.

Simple rate

Yearly compounded rate

Continuously compounded rate

############################

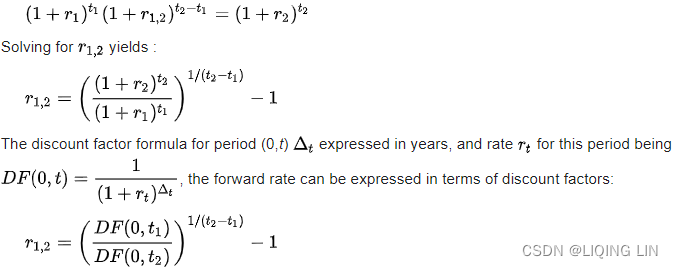

An investor who plans to invest at a later time may be curious to know what the future interest rate will look like, as implied by today's term structure of interest rates. For example, you might ask, What is the one-year spot rate one year from now? To answer this question, you can calculate forward rates for the period between T1 and T2 using this formula:

Here, and

are the continuously-compounded annual interest rates at time periods

and

, respectively.

The following ForwardRates class helps us generate a list of forward rates from a list of spot rates:

# Continuously compounded rate

class ForwardRates( object ):

def __init__(self):

self.forward_rates = []

self.spot_rates = dict()

def add_spot_rate( self, T, spot_rate ):

self.spot_rates[T] = spot_rate

def calculate_forward_rate( self, T1, T2 ):

# 0 ~ R1 ~ T1 ~ Forward rate ~ T2

# | -- R2 -- |

R1 = self.spot_rates[T1]

R2 = self.spot_rates[T2]

forward_rate = (R2*T2 - R1*T1)/(T2-T1)

return forward_rate

def get_forward_rates( self ):

"""

Returns a list of forward rates

starting from the second time period.

"""

periods = sorted( self.spot_rates.keys() )

for T2, T1 in zip( periods, periods[1:] ):

forward_rate = self.calculate_forward_rate(T1, T2)

self.forward_rates.append( forward_rate )

return self.forward_ratesUsing spot rates derived from our preceding yield curve, we get the following result:

fr = ForwardRates()

fr.add_spot_rate( 0.25, 10.127 )

fr.add_spot_rate( 0.50, 10.469 )

fr.add_spot_rate( 1.00, 10.536 )

fr.add_spot_rate( 1.50, 10.681 )

fr.add_spot_rate( 2.00, 10.808 )

print( fr.get_forward_rates() ) ![]()

Calling the get_forward_rates() method of the ForwardRates class returns a list of forward rates, starting from the next time period.

Calculating the yield to maturity

The yield to maturity (YTM到期收益率) measures the interest rate, as implied by the bond, which takes into account the present value of all the future coupon payments and the principal. It is assumed that bond holders can invest received coupons(or interest payments) at the YTM rate until the maturity of the bond; according to risk-neutral expectations, the payments received should be the same as the price paid for the bond.

- C = the periodic coupon payment

or is the coupon dollar amount paid at each time point T (T=1, 2, ..., nt)

if n = 1

0 ~ T1 ~ T2 ~ ... ~ t

| |

| C | |

| ... C |

| ...

| ... C - y = the yield to maturity (YTM)

- n: the number of times it is compounded

or the coupon payment frequency.

if n=1, then C = C : the coupon dollar amount paid at each time point T (T=1, 2, ..., t)

if n>1, then C = C/n : the coupon dollar amount paid at each time point T (T=1, 2, ..., nt)

- T = the time period of payment (in years), T=1, 2, ..., t

- t : the bond's maturity date

Let's take a look at an example of a 5.75% bond that will mature in 1.5 years(t=1.5) with a par value of 100(C=5.75%*100=5.75). The price of the bond is $95.0428 and coupons are paid semi-annually(n=2, c=C/n= 5.75/2=2.875). The pricing equation can be stated as follows:

To solve the YTM is typically a complex process, and most bond YTM calculators use Newton's method as an iterative process.

https://blog.csdn.net/Linli522362242/article/details/125662545

==>

==>![]()

The bond YTM calculator is illustrated by the following bond_ytm() function:

import scipy.optimize as optimize

def bond_ytm( price, par, T, coupon, freq=2, guess_y=0.05):

freq = float( freq )

periods = T*freq

# dt = [ (i+1)/freq for T_i in range(int(periods)) ]

dt = [ (i+1)/freq for i in range(int(periods))]

# price : Bound_Price

ytm_func = lambda y : sum([coupon/freq / (1+y/freq)**(freq*t_i)

for t_i in dt

])+\

par / (1+y/freq)**(freq*T)\

- price

# Bound_Price=ytm_func ==> ytm_func-Bound_Price=0

return optimize.newton(ytm_func, guess_y)Remember that we covered the use of Newton's method and other nonlinear function root solvers in https://blog.csdn.net/Linli522362242/article/details/125662545, Nonlinearity in Finance. For this YTM calculator function, we used the scipy.optimize package to solve the YTM.

Let's take a look at an example of a 5.75% bond(==> coupon=5.75% * par / nt) that will mature in 1.5 years with a par value of 100. The price of the bond is $95.0428 and coupons are paid semi-annually. The pricing equation can be stated as follows:

par = 100

T = 1.5 # deltaT = 1

freq_in_deltaT = 2 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 5.75

bondPrice = 95.0428

ytm = bond_ytm(bondPrice,

par, T, coupon_at_Ti, freq_in_deltaT)

print( "YTM: {}".format( ytm ) )![]()

The YTM of the bond is 9.369%. Now we have a bond YTM calculator that can help us compare a bond's expected return with those of other securities.

if n=1==>

The cash flows for the Ford bond consist of the purchase price for the bond today of $744.80, annual interest payments for Years 1 through 10 of $65, and a final interest payment of $65 plus the principal payment of $1,000, both at the end of Year 11.

par = 1000

T = 11 # deltaT = 1

freq_in_deltaT = 1 # dt = deltaT/freq_in_deltaT ==> dt = 1

coupon_at_Ti = 65 # Ti : 1,2,3...11=T

bondPrice = 744.80

ytm = bond_ytm(bondPrice,

par, T, coupon_at_Ti, freq_in_deltaT)

print( "YTM: {:.2f}%".format( ytm*100 ) ) ![]()

The yield to maturity on the bond is 10.52 percent, considerably higher than the coupon rate of interest of 6.5 percent($65/$1000) that the bond promises to pay. The fact that the yield to maturity is higher than the coupon rate is also consistent with the fact that the current market price of the bond is considerably less than the bond’s par value of $1,000. In fact, if the bond price were equal to the bond’s par value, then the yield to maturity and coupon rate of interest would be the same.

par = 1000

T = 11 # deltaT = 1

freq_in_deltaT = 1 # dt = deltaT/freq_in_deltaT ==> dt = 1

coupon_at_Ti = 65 # Ti : 1,2,3...11=T

bondPrice = 1000

ytm = bond_ytm(bondPrice,

par, T, coupon_at_Ti, freq_in_deltaT)

print( "YTM: {:.2f}%".format( ytm*100 ) )![]() if the bond price were equal to the bond’s par value, then the yield to maturity and coupon rate of interest would be the same.

if the bond price were equal to the bond’s par value, then the yield to maturity and coupon rate of interest would be the same.

Calculating the price of a bond

When the YTM is known, we can get back the bond price in the same way we used the pricing equation. This is implemented by the bond_price() function:

def bond_price( par, T, ytm, coup, freq=2 ):

freq = float(freq)

periods = T*freq

coupon = coup

# dt = [ (i+1)/freq for T_i in range(int(periods)) ]

dt = [ (i+1)/freq for i in range(int(periods))]

# price : Bound_Price

price = sum([coupon/freq / (1+ytm/freq)**(freq*t_i)

for t_i in dt

])+\

par / (1+ytm/freq)**(freq*T)

return pricePlugging in the same values from the earlier example, we get the following result:

par = 100

T = 1.5 # deltaT = 1

freq_in_deltaT = 2 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 5.75 # Ti

ytm_in_deltaT = 0.09369155345239522

price = bond_price(par, T,

ytm_in_deltaT,

coupon_at_Ti, freq_in_deltaT)

print("Bond price:", price)![]()

This gives us the same original bond price discussed in the earlier example, Calculating the yield to maturity. With the bond_ytm() and bond_price() functions, we can apply these for further uses in bond pricing, such as finding the bond's modified duration and convexity. These two characteristics of bonds are of importance to bond traders in helping them formulate制定 various trading strategies and hedge their risk.

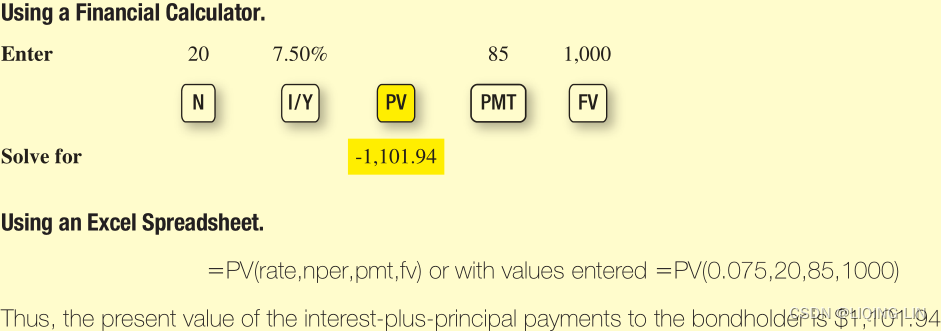

Consider a $1,000 par value bond issued by AT&T (T) with a maturity date of 2032 and a stated coupon rate of 8.5 percent. On January 1, 2013, the bond had 20 years left to maturity, and the market’s required yield to maturity for similar rated debt was 7.5 percent. What is the value of the bond?

The cash flows for the AT&T bond consist of the value of the bond today, which we are trying to estimate, the annual interest payments for Years 1 through 20 of $85 each, and principal payment at the end of Year 20 equal to $1,085 (this is in addition to the $85 interest payment also at the end of Year 20).

par = 1000

T = 20 # deltaT = 1

freq_in_deltaT = 1 # dt = deltaT/freq_in_deltaT ==> dt = 1

coupon_at_Ti = 85 # Ti : 1,2,3...20=T

ytm_in_deltaT = 0.075

price = bond_price(par, T,

ytm_in_deltaT,

coupon_at_Ti, freq_in_deltaT)

print("Bond price:", price)

bondPrice = 1101.94

ytm = bond_ytm( bondPrice,

par, T, coupon_at_Ti, freq_in_deltaT)

print( "{:.2f}%".format( ytm*100 ) ) ![]()

The value we calculated for the AT&T bond is $1,101.94, which exceeds the $1,000 par value of the bond. This reflects the fact that the market’s required yield to maturity on a comparable-risk bond is less than the coupon rate of interest paid on the bond of 8.5 percent($85/1000). In all likelihood, when the AT&T bonds were originally issued, they were issued at par because the market’s required yield to maturity on comparable-risk bonds was at or very near to the 8.5 percent coupon rate. Since the time of issue, however, market rates of interest have declined such that the bonds now sell at a premium(sell at >$1,000 par value). Thus if the bonds are sold for $1,101.94, they will yield a return of only 7.5 percent.

To illustrate this bond price formula in action, consider a 20-year, 9.5% bond priced to yield 10%. That is, the bond pays an annual coupon of 9.5% (or $95), has 20 years left to maturity, and should be priced to provide a market yield of 10%. We can now use Equation 11.3 to find the price of our bond.

par = 1000

T = 20 # deltaT = 1

freq_in_deltaT = 1 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 95 # Ti : 1,2,3...20=T*1 if freq_in_deltaT =1

# Ti : 1,2,3...40=T*2 if freq_in_deltaT =2

ytm_in_deltaT = 0.1

price = bond_price(par, T,

ytm_in_deltaT,

coupon_at_Ti, freq_in_deltaT)

print("Bond price:", price) ![]()

Note that because this is a coupon-bearing bond, we have an annuity of coupon payments of $95 a year for 20 years, plus a single cash flow of $1,000 that occurs at the end of year 20. Thus, we find the present value of the coupon annuity and then add that amount to the present value of the recovery of principal at maturity. In this particular case, you should be willing to pay about $958 for this bond, so long as you’re satisfied with earning 10% on your money.

Notice that this bond trades at a discount of $42.57 ($1,000 – $957.43). It trades at a discount because its coupon rate (9.5%) is below the market’s required return (10%). You can directly link the size of the discount on this bond to the present value of the difference between the coupons that it pays ($95) and the coupons that would be required if the bond matched the market’s 10% required return ($100). In other words, this bond’s coupon payment is $5 less than what the market requires, so if you take the present value of that difference over the bond’s life, you will calculate the size of the bond’s discount:

semiannual basis ==>

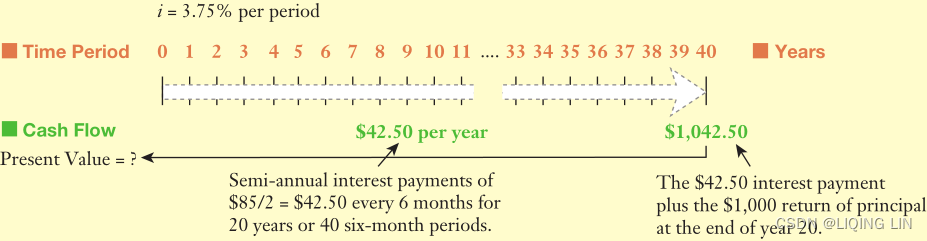

Reconsider the bond issued by AT&T (T) with a maturity date of 2032 and a stated coupon rate of 8.5 percent. AT&T pays interest to bondholders on a semiannual basis on January 15 and July 15. On January 1, 2013, the bond had 20 years left to maturity. The market’s required yield to maturity for a similarly rated debt was 7.5 percent per year or 3.75 percent(3.75%=7.5%/2.0) for six months. What is the value of the bond?

The cash flows for the AT&T bond consist of the value of the bond today, which we are trying to estimate, the semiannual interest payments for Periods 1 through 39 of $42.50 each($42.50=$85/2), and a final interest-plus-principal pay-ment at the end of Year 20 or Period 40 equal to $1,042.50.

par = 1000

T = 20 # deltaT = 1

freq_in_deltaT = 2 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 85 # Ti : 1,2,3...20=T*1 if freq_in_deltaT =1

# Ti : 1,2,3...40=T*2 if freq_in_deltaT =2

ytm_in_deltaT = 0.075

price = bond_price(par, T,

ytm_in_deltaT,

coupon_at_Ti, freq_in_deltaT)

print("Bond price:", price)

bondPrice = 1102.75

ytm = bond_ytm(bondPrice,

par, T, coupon_at_Ti, freq_in_deltaT)

print( "YTM: {:.2f}%".format( ytm*100 ) )

print( "YTM/{}: {:.2f}%".format( freq_in_deltaT, ytm*100/freq_in_deltaT ) ) ![]()

Using semiannual compounding, we calculate a value of $1,102.75 for the AT&T bond compared to the $1,101.94 we calculated using annual compounding—this value is not vastly different没有太大的不同, but for a large investor buying thousands of bonds, this can certainly add up over time.

Bond duration

###################

Measuring Duration(Macaulay duration)

==>

![]()

Duration is a measure of the average maturity of a fixed-income security. The term average maturity may be confusing because bonds have only one final maturity date. An alternative definition of average maturity might be that it captures the average timing of the bond’s cash flow.

- For a zero-coupon bond(C=0 and n=1) that makes only one cash payment on the final maturity date, the bond’s duration equals its maturity.

- But because coupon-paying bonds make periodic interest payments, the average timing of these payments (i.e., the average maturity) is different from the actual maturity date(t). For instance, a 10-year bond that pays a 5% coupon each year(n=1, C = 5% * FV /n = 5%*FV) distributes a small cash flow in year 1, in year 2, and so on up until the last and largest cash flow in year 10.

Duration is a measure that puts some weight on these intermediate payments, so that the “average maturity” is a little less than 10 years.

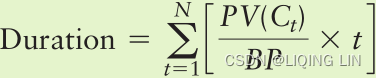

Equation 11.8  Macaulay duration

Macaulay duration

where

= present value of a future coupon or principal payment

- BP = current market price of the bond

- t = year in which the cash flow (coupon or principal) payment is received

- N = number of years to maturity

The duration measure obtained from Equation 11.8 is commonly referred to as Macaulay duration—named after the actuary who developed the concept.

Although duration is often computed using semiannual compounding, Equation 11.8 uses annual coupons and annual compounding to keep the ensuing discussion and calculations as simple as possible. Even so, the formula looks more formidable than it really is. If you follow the basic steps noted below, you’ll find that duration is not tough to calculate.

- Step 1. Find the present value of each annual coupon or principal payment

. Use the 现行prevailing YTM on the bond as the discount rate.

OR

- Step 2. Divide this present value by the current market price of the bond (BP). This is the weight, or the fraction of the bond’s total value accounted for by each individual payment每笔单独付款占债券总价值的比例.

Because a bond’s value is just the sum of the present values of its cash payments, these weights must sum to 1.0. - Step 3. Multiply this weight by the year in which the cash flow is to be received (t).

- Step 4. Repeat steps 1 through 3 for each year in the life of the bond, and then add up the values computed in step 3.

Duration for a Single Bond

Table 11.1 (on page 435) illustrates the four-step procedure for calculating the duration of a 7.5%(n=1, C = 7.5% * FV /n = 7.5%*1000 = $75), 15-year bond priced at $957.20 to yield 8%.

Table 11.1 provides the basic input data:

- Column (1) shows the year (t) in which each cash payment arrives.

- Column (2) provides the dollar amount of each cash payment (coupons and principal) made by the bond.

- Column (3) lists the present value of each cash flow, given an 8% discount rate (which is equal to the prevailing YTM on the bond).

- For example, in row 1 of Table 11.1, we see that in year 1 the bond makes a $75 coupon payment, and discounting that to the present at 8% reveals that the first coupon payment has a present value of

.

- For example, in row 1 of Table 11.1, we see that in year 1 the bond makes a $75 coupon payment, and discounting that to the present at 8% reveals that the first coupon payment has a present value of

- Next, in column 4 we divide the present value in column 3 by the current market price of the bond. If the present value of this bond’s first coupon payment is $69.44 and the total price of the bond is $957.20, then that first payment accounts for 7.25% of the bond’s total value (

). Therefore, 7.25% is the “weight” given to the cash payment made in year 1.

is the “weight” given to the cash payment made in year 2

is the “weight” given to the cash payment made in year 15

- If you sum the weights in column 4, you will see that they add to 1.0.

Because a bond’s value is just the sum of the present values of its cash payments, these weights must sum to 1.0

- If you sum the weights in column 4, you will see that they add to 1.0.

- Multiplying the weights from column 4 by the year (t) in which the cash flow arrives results in a time-weighted value for each of the annual cash flow streams shown in column 5.

- Adding up all the values in column 5 yields the duration of the bond. As you can see, the duration of this bond is a lot less than its maturity(9.36 yr < 15 yr).

In addition, keep in mind that the duration on any bond will change over time as YTM and term to maturity change. For example, the duration on this 7.5%, 15-year bond will fall as the bond nears maturity and/or as the market yield (YTM) on the bond increases.

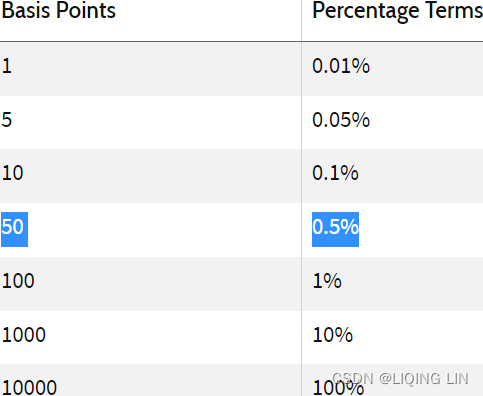

A bond’s price volatility is, in part, a function of its term to maturity and, in part, a function of its coupon. Unfortunately, there is no exact relationship between bond maturities and bond price volatilities with respect to interest rate changes. There is, however, a fairly close relationship between bond duration and price volatility—as long as the market doesn’t experience wide swings in interest rates. A bond’s duration can be used as a viable predictor of its price volatility only so long as the yield swings are relatively small (no more than 50 to 100 basis points, or so). That’s because as interest rates change, bond prices change in a nonlinear (convex) fashion. For example,

- when interest rates fall, bond prices rise at an increasing rate.

- When interest rates rise, bond prices fall at a decreasing rate.

The duration measure essentially predicts that as interest rates change, bond prices will move in the opposite direction in a linear fashion. This means that

- when interest rates fall, bond prices will rise a bit faster than the duration measure would predict,

- and when interest rates rise, bond prices will fall at a slightly slower rate than the duration measure would predict.

The bottom line最重要的是 is that the duration measure helps investors understand how bond prices will respond to changes in market rates, as long as those changes are not too large.

Modified Duration

The mathematical link between changes in interest rates and changes in bond prices involves the concept of modified duration. To find modified duration, we simply take the (Macaulay) duration for a bond (as found from Equation 11.8and) and adjust it for the bond’s yield to maturity.

Equation 11.9

Thus, the modified duration for the 15-year bond discussed above is  Note that here we use the bond’s computed (Macaulay) duration of 9.36 years and the same YTM we used to compute duration in Equation 11.8; in this case, the bond was priced to yield 8%, so we use a yield to maturity of 8%.

Note that here we use the bond’s computed (Macaulay) duration of 9.36 years and the same YTM we used to compute duration in Equation 11.8; in this case, the bond was priced to yield 8%, so we use a yield to maturity of 8%.

To determine, in percentage terms, how much the price of this bond would change as market interest rates increased by 50 basis points from 8% to 8.5%,

we multiply the modified duration value calculated above first by –1 (because of the inverse relationship between bond prices and interest rates) and then by the change in market interest rates. That is,

Thus, a 50-basis-point (or 0.5% = ½ of 1%) increase in market interest rates will lead to an approximate 4.33% drop in the price of this 15-year bond. Such information is useful to bond investors seeking—or trying to avoid—price volatility.

Effective Duration

One problem with the duration measures that we’ve studied so far is that they do not always work well for bonds with embedded options such as callable bonds. That is, the duration measures we’ve been using assume that the bond’s future cash flows ( or

) are paid as originally scheduled through maturity, but that may not be the case with callable bonds (or convertible bonds or bonds with other types of options attached to them). An alternative duration measure that is used for these types of bonds is the effective duration. To calculate effective duration (ED), you use Equation 11.11:

VS

VS

-

= the new price of the bond if market interest rates

= the new price of the bond if market interest ratesgo down

the price of the bond from a decrease in yield by dY  = the new price of the bond if market interest rates

= the new price of the bond if market interest rates

the price of the bond from an increase in yield by dY= the original price of the bond

= the change in market interest rates

dY is the given change in yield

Suppose you want to know the effective duration of a 25-year bond that pays a 6% coupon semiannually(2). The bond is currently priced at $882.72 for a yield of 7%.

par = 1000

T = 25 # deltaT = 1

freq_in_deltaT = 2 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 60 # Ti : 1,2,3...20=T*1 if freq_in_deltaT =1

# Ti : 1,2,3...40=T*2 if freq_in_deltaT =2

ytm_in_deltaT = 0.07

price = bond_price(par, T,

ytm_in_deltaT,

coupon_at_Ti, freq_in_deltaT)

print("Bond price:", price)![]()

Now suppose the bond’s yield goes up by 0.5%

( use 50-basis-point = 50% * 1% = 0.5% change in yield )

change in yield) to 7.5%. At that yield the new price![]() would be $831.74 (using a calculator, N = 50 = 25*2, I = 3.75 = 7%/2, PMT = 30 = 6%/2 * 1000, and PV = 1,000).

would be $831.74 (using a calculator, N = 50 = 25*2, I = 3.75 = 7%/2, PMT = 30 = 6%/2 * 1000, and PV = 1,000).

par = 1000

T = 25 # deltaT = 1

freq_in_deltaT = 2 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 60 # Ti : 1,2,3...20=T*1 if freq_in_deltaT =1

# Ti : 1,2,3...40=T*2 if freq_in_deltaT =2

ytm_in_deltaT = 0.075

price = bond_price(par, T,

ytm_in_deltaT,

coupon_at_Ti, freq_in_deltaT)

print("Bond price:", price)![]()

![]()

What if the yield drops by 0.5%

( use 50-basis-point = 50% * 1% = 0.5% change in yield )

to 6.5%? In that case, the price rises![]() to $938.62 (N = 50, I = 3.25, PMT = 30, PV = 1,000).

to $938.62 (N = 50, I = 3.25, PMT = 30, PV = 1,000).

par = 1000

T = 25 # deltaT = 1

freq_in_deltaT = 2 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 60 # Ti : 1,2,3...20=T*1 if freq_in_deltaT =1

# Ti : 1,2,3...40=T*2 if freq_in_deltaT =2

ytm_in_deltaT = 0.065

price = bond_price(par, T,

ytm_in_deltaT,

coupon_at_Ti, freq_in_deltaT)

print("Bond price:", price) ![]()

![]()

Now we can use Equation 11.11 to calculate the bond’s effective duration.

Effective duration =

This means that if interest rates rise or fall by a full percentage point一个百分点(50-basis-point = 50% * 1% = 0.5% change in yield, 0.5%*2=1%), the price of the bond would fall or rise by approximately 12.11%.

Note that you can use effective duration in place of modified duration in Equation 11.10to find the percent change in the price of a bond when interest rates move by more or less than 1.0%.

When calculating the effective duration of a callable bond, one modification may be necessary.

- If the calculated price of the bond when interest rates fall is greater than the bond’s call price, then use the call price in the equation rather than and proceed as before.

###################

Duration is a sensitivity measure of bond prices to yield changes. Some duration measures are

- effective duration,

- Macaulay duration,

- and modified duration.

The type of duration that we will discuss is modified duration, which measures the percentage change in bond price with respect to a percentage change in yield衡量债券 价格的百分比变化 相对于 收益率百分比变化 (typically 1% or 100 basis points (bps)).

- The higher the duration of a bond, the more sensitive it is to yield changes.

- Conversely, the lower the duration of a bond, the less sensitive it is to yield changes.

The modified duration of a bond can be thought of as the first derivative of the relationship between price and yield: VS

Here:

- dY is the given change in yield

is the price of the bond from a decrease in yield by dY

is the price of the bond from an increase in yield by dY

is the initial price of the bond

It should be noted that the duration describes the linear price-yield relationship for a small change in Y. Because the yield curve is not linear, using a large value of dY does not approximate the duration measure well.

The implementation of the modified duration(should be called Effective duration) calculator is given in the following bond_mod_duration() function.

- It uses the bond_ytm() function as discussed earlier in this chapter, Calculating the yield to maturity, to determine the yield of the bond with the given initial value.

- Also, it uses the bond_price() function to determine the price of the bond with the given change in yield:

def bond_mod_duration( price, par, T, coup, freq, dy=0.01 ):

# dy : the change in market interest rates

# 0.01 : 1-basis-point change in yield

ytm = bond_ytm( price, par, T, coup, freq )

ytm_minus = ytm - dy

price_minus = bond_price( par, T, ytm_minus, coup, freq )

# the price of the bond from a decrease in yield by dY

# or the new price of the bond if market interest rate(ytm) go down

print( 'the price of the bond from a decrease in yield by {}: {:.4f}'.format(dy, price_minus) )

ytm_plus = ytm + dy

price_plus = bond_price( par, T, ytm_plus, coup, freq )

# the price of the bond from an increase in yield by dY

# the new price of the bond if market interest rate(ytm) go up

print( 'the price of the bond from an increase in yield by {}: {:.4f}'.format(dy, price_plus) )

mduration = ( price_minus-price_plus )/( 2*price*dy )

return mduration We can find out the modified duration of the 5.75% bond(coupon payment: 5.75%*100=$5.75) discussed earlier, in Calculating the yield to maturity, which will mature in 1.5 years(t) with a par value of 100 and a bond price of 95.0428(BP):n=2 since this bond will pay a fixed amount of interest semi-annually,

vs

mod_duration = bond_mod_duration( 95.0428, 100, 1.5, 5.75, 2 )

print( mod_duration )![]()

The modified duration of the bond is 1.392 years(< the maturity of bond 1.5 yr). Duration is a measure of the average maturity of a fixed-income security. The term average maturity may be confusing because bonds have only one final maturity date. An alternative definition of average maturity might be that it captures the average timing of the bond’s cash flow.

Suppose you want to know the effective duration of a 25-year bond that pays a 6% coupon semiannually(n=2). The bond is currently priced at $882.72 for a yield of 7%.

Now suppose the bond’s yield goes up by 0.5%

( use 50-basis-point = 50% * 1% = 0.5% change in yield ) change in yield )

to 7.5%. At that yield the new price![]() would be $831.74 (using a calculator, N = 50 = 25*2, I = 3.75 = 7%/2, PMT = 30 = 6%/2 * 1000, and PV = 1,000).

would be $831.74 (using a calculator, N = 50 = 25*2, I = 3.75 = 7%/2, PMT = 30 = 6%/2 * 1000, and PV = 1,000).

What if the yield drops by 0.5% to 6.5%? In that case, the price rises![]() to $938.62 (N = 50, I = 3.25, PMT = 30, PV = 1,000).

to $938.62 (N = 50, I = 3.25, PMT = 30, PV = 1,000).

par = 1000

T = 25 # deltaT = 1

freq_in_deltaT = 2 # dt = deltaT/freq_in_deltaT ==> dt = 0.5

coupon_at_Ti = 60 # Ti : 1,2,3...20=T*1 if freq_in_deltaT =1

# Ti : 1,2,3...40=T*2 if freq_in_deltaT =2

ytm_in_deltaT = 0.07

bondPrice = 882.72

dy=0.005 # use 50-basis-point = 50% * 1% = 0.5% change in yield

mod_duration = bond_mod_duration( bondPrice, par, T, coupon_at_Ti, freq_in_deltaT, dy)

print( mod_duration )![]() This means that if interest rates rise or fall by a full percentage point一个百分点(50-basis-point = 50% * 1% = 0.5% change in yield, 0.5%*2=1%), the price of the bond would fall or rise by approximately 12.11%.

This means that if interest rates rise or fall by a full percentage point一个百分点(50-basis-point = 50% * 1% = 0.5% change in yield, 0.5%*2=1%), the price of the bond would fall or rise by approximately 12.11%.

Bond convexity

Convexity is the sensitivity measure of the duration of a bond to yield changes衡量债券久期对收益率变化的敏感度. Think of convexity as the second derivative of the relationship between the price and yield:

Bond traders use convexity as a risk-management tool to measure the amount of market risk in their portfolio衡量其投资组合中的市场风险量.

- Higher-convexity portfolios are less affected by interest-rate volatilities than lower-convexity portfolios, given the same bond duration and yield.

- As such, higher-convexity bonds are more expensive than lower-convexity ones, everything else being equal.

The implementation of a bond convexity is given as follows:

def bond_convexity( price, par, T, coup, freq, dy=0.01 ):

# dy : the change in market interest rates

# 0.01 : 1-basis-point change in yield

ytm = bond_ytm( price, par, T, coup, freq )

ytm_minus = ytm-dy

price_minus = bond_price( par, T, ytm_minus, coup, freq )

# the price of the bond from a decrease in yield by dY

# or the new price of the bond if market interest rate(ytm) go down

print( 'the price of the bond from a decrease in yield by {}: {:.4f}'.format(dy, price_minus) )

ytm_plus = ytm + dy

price_plus = bond_price(par, T, ytm_plus, coup, freq)

# the price of the bond from an increase in yield by dY

# the new price of the bond if market interest rate(ytm) go up

print( 'the price of the bond from an increase in yield by {}: {:.4f}'.format(dy, price_plus) )

convexity = (price_minus + price_plus - 2*price)/(price*dy**2)

return convexityWe can now find the convexity of the 5.75% bond discussed earlier, in Calculating the yield to maturity section, which will mature in 1.5 years with a par value of 100 and a bond price of 95.0428:

convexity = bond_convexity( 95.0428, 100, 1.5, 5.75, 2 )

print( convexity )![]()

The convexity of the bond is 2.63. For two bonds with the same par value(), coupon

, and maturity(

), their convexity may be different, depending on their location on the yield curve.

Higher-convexity bonds will exhibit higher price changes for the same change in yield(dY).

Short–rate modeling

In short-rate modeling, the short-rate, r(t), is the spot rate即期利率 at a particular time. It is described as a continuously-compounded连续复利, annualized interest rate term for an infinitesimally short period of time on the yield curve. The short-rate takes on the form of a stochastic variable in interest-rate models, where the interest rates may change by small amounts at every point in time. Short-rate models attempt to model the evolution of interest rates over time, and hopefully describe the economic conditions at certain periods.

Short-rate models are frequently used in the evaluation of interest-rate derivatives利率衍生品的评估. Bonds, credit instruments, mortgages, and loan products are sensitive to interest-rate changes. Short-rate models are used as interest rate components in conjunction with pricing implementations, such as numerical methods, to help price such derivatives.

Interest-rate modeling is considered a fairly complex topic since interest rates are affected by a multitude of factors, such as

- economic states经济状况,

- political decisions政策决定,

- government intervention政府干预,

- and laws of supply and demand供求规律 .

A number of interest-rate models have been proposed to account for various characteristics of interest rates.

In this section, we will take a look at some of the most popular one-factor short-rate models单因素短期利率模型 used in financial studies, namely,

- the Vasicek,

- Cox-Ingersoll-Ross,

- Rendleman and Bartter,

- and Brennan and Schwartz models.

Using Python, we will perform a one-path simulation to obtain a general overview of the interest-rate path process. Other models commonly discussed in finance include the Ho-Lee, Hull-White, and Black-Karasinki.

#########################

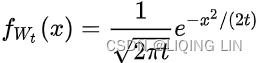

Brownian motion(Wiener process维纳过程)

以W(t)表示运动中一微粒从时刻t=0到时刻t>0的位移的横坐标(同样也可以讨论纵坐标),且设=0,根据爱因斯坦1905年提出的理论,微粒的这种运动是由于受到大量随机的相互独立的分子的碰撞的结果. 于是,粒子在时段(s,t]上的位移可以看作是许多微小位移的代数和. 则

服从正态分布。

The Wiener process is characterised by the following properties:

=0 OR

- W has independent increments:

for every t>0, the future increments, u>=0, are independent of the past values

, s<=t,

s <= t <= t+u - W has Gaussian increments:

- W has continuous paths:

is continuous in t

is continuous in t

That the process has independent increments means that if  then

then and

are independent random variables, and the similar condition holds for n increments.

Basic properties of a one-dimensional Wiener process

The unconditional probability density function follows a normal distribution with mean = 0 and variance = t, at a fixed time t:

normal distribution:

The expectation is zero:

The expectation is zero:

The variance, using the computational formula, is t: ![]()

These results follow immediately from the definition that increments have a normal distribution, centered at zero. Thus

######################

The Vasicek model

In finance, the Vasicek model is a mathematical model describing the evolution of interest rates. It is a type of one-factor short-rate model as it describes interest rate movements as driven by only one source of market risk. The model can be used in the valuation估值 of interest rate derivatives, and has also been adapted for credit markets. It was introduced in 1977 by Oldřich Vašíček,[1] and can be also seen as a stochastic investment model.

In the one-factor Vasicek model, the short-rate is modeled as a single stochastic factor单个随机因素:![]()

-

Process level at date t

The drift coefficient

depends on the current value of

If, then the drift coefficient is positive;

if -

All future trajectories of -

K Mean-reversion factor

"speed of reversion回归速度". K characterizes the velocity at which such trajectories will regroup around -

is a Wiener process(Standard Brownian motion) under the risk neutral framework modelling the random market risk factor, in that it models the continuous inflow of randomness into the systemhttps://blog.csdn.net/Linli522362242/article/details/125355166

- The standard deviation parameter,

, determines the volatility of the interest rate and in a way characterizes the amplitude/ˈæmplɪtuːd/ of the instantaneous randomness inflow.

: "long term variance". All future trajectories of r will regroup around the long term mean with such variance after a long time.

- K and

increasing OR

OR ) determined also by K. This is clear when looking at the long term variance,

increases

Here, K, θ, and σ are constants, and σ is the instantaneous/ˌɪnstənˈteɪniəs/ standard deviation. W(t) is the random Wiener process. The Vasicek follows an Ornstein–Uhlenbeck stochastic process, where the model reverts around the mean, θ, with K, the speed of mean reversion. As a result, the interest rates() may become negative, which is an undesirable不受欢迎的 property in most normal economic conditions.

(![]() Making the long term mean

Making the long term mean stochastic to another SDE is a simplified version of the cointelation SDEhttps://blog.csdn.net/Linli522362242/article/details/96593981)

![]() https://blog.csdn.net/Linli522362242/article/details/125355166

https://blog.csdn.net/Linli522362242/article/details/125355166

since![]() and

and ![]() are identical in distribution, where Z is a standard normal variable.(

are identical in distribution, where Z is a standard normal variable.(![]() =

=![]() =

=![]()

)

To help us understand this model, the following code generates a list of interest rates:

import math

import numpy as np

def vasicek( r0, K, theta, sigma, T=1., N=10, seed=777 ):

# r0 : the initial rate of interest at t=0

# K : "speed of Mean-reversion

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

# T : the period in terms of number of years

# N : the number of intervals for the modeling process

# W : a Wiener process(Standard Brownian motion)

# modelling the random market risk factor(under the risk neutral framework)

np.random.seed( seed )

dt = T/float(N)

rates = [r0]

# Z is a standard normal variable

for i in range(N): # dW = sqrt(dt) * dZ

dr = K * (theta - rates[-1]) * dt + sigma* math.sqrt(dt) * np.random.normal()

rates.append( rates[-1]+dr )

# returns a list of time periods and interest rates

return range(N+1), ratesThe vasicek() function returns a list of time periods and interest rates from the Vasicek model. It takes in a number of input arguments: r0 is the initial rate of interest at t=0; K , theta , and sigma are constants; T is the period in terms of number of years; N is the number of intervals for the modeling process; and seed is the initialization value for NumPy's standard normal random-number generator.

Assume that the current interest rate is close to zero at 0.5%, the long term mean level theta is 0.15, and the instantaneous volatility sigma is 5%. We will use a T value of 10 and an N value of 200 to model the interest rates for different speeds of mean reversion, K, with values of 0.002, 0.02, and 0.2 :

%matplotlib inline

import matplotlib.pyplot as plt

fig = plt.figure( figsize=(12,8) )

# r0 : the initial rate of interest at t=0

r0 = 0.005

# K : "speed of Mean-reversion

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

theta = 0.15

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

sigma = 0.05

# T : the period in terms of number of years

T = 10

# N : the number of intervals for the modeling process

N = 200

# K : "speed of Mean-reversion

K_list = [0.002, 0.02, 0.2]

colors = ['k','g','b']

for index, K in enumerate(K_list):

N_plus_1, rate_list = vasicek( r0, K, theta ,sigma, T, N )

plt.plot( N_plus_1, rate_list,

label='K=%s' % K,

c = colors[index]

)

plt.axhline(y=theta, ls='--', c='r') # Long-term mean(theta) of the process

plt.annotate( r'Long-term mean(${\theta}$)',

ha='right',

va='top',

xytext=(80, theta - 0.01), #The xytext parameter specifies the text position

xy=(80, theta), #The xy parameter specifies the arrow's destination

arrowprops=dict(facecolor='blue', headwidth=10, headlength=4, width=2 ),

#arrowprops={'facecolor':'blue', 'headwidth':10, 'headlength':4, 'width':2} #OR

fontsize=14

)

plt.legend( loc='upper left' , fontsize=14)

plt.ylabel('The interest rate', fontsize=14)

plt.xlabel('The time t', fontsize=14)

plt.title('Vasicek model', fontsize=14)

plt.show()After running the preceding commands, we get the following graph:

In this example, we are running just one simulation to see what the interest rates from the Vasicek model looks like. Observe that interest rates did become negative at some point. With higher levels of speed for mean reversion, K , the process reaches its long-term level of 0.15(the model reverts around the mean, θ=0.15) sooner.

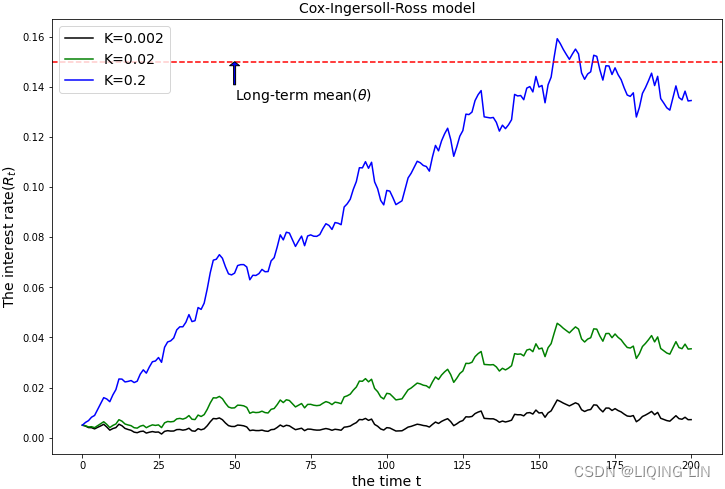

The Cox-Ingersoll-Ross model

The Cox-Ingersoll-Ross (CIR) model is a one-factor model that was proposed to address the negative interest rates found in the Vasicek model.(It is a type of one-factor short-rate model as it describes interest rate movements as driven by only one source of market risk)![]() ==>

==>. The process is given as follows:

==>

==>

-

The drift coefficient

If

if -

All future trajectories of -

K Mean-reversion factor

"speed of reversion回归速度". K characterizes the velocity at which such trajectories will regroup around -

- The standard deviation parameter,

- K and

increasingOR

increases

The term increases the standard deviation as the short-rate increases. Now the vasicek() function can be rewritten as the CIR model in Python:

import math

import numpy as np

def CIR( r0, K, theta, sigma, T=1, N=10, seed=777 ):

# r0 : the initial rate of interest at t=0

# K : "speed of Mean-reversion

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

# T : the period in terms of number of years

# N : the number of intervals for the modeling process

# W : a Wiener process(Standard Brownian motion)

# modelling the random market risk factor(under the risk neutral framework)

np.random.seed(seed)

dt = T/float(N)

rates = [r0]

# dW = sqrt(dt) * dZ

for i in range(N): # Z is a standard normal variable

dr = K * ( theta-rates[-1] ) * dt +\

sigma * math.sqrt( rates[-1] ) * math.sqrt(dt)*np.random.normal()

rates.append( rates[-1] + dr )

# returns a list of time periods and interest rates

return range(N+1), ratesUsing the same example given in the The Vasicek model section, assume that the current interest rate is 0.5%, theta is 0.15 , and sigma is 0.05 . We will use a T value of 10 and N of 200 to model the interest rates with different speeds of mean reversion, K , using values of 0.002 , 0.02 , and 0.2:

%matplotlib inline

import matplotlib.pyplot as plt

fig = plt.figure( figsize=(12,8) )

# r0 : the initial rate of interest at t=0

r0 = 0.005

# K : "speed of Mean-reversion

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

theta = 0.15

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

sigma = 0.05

# T : the period in terms of number of years

T = 10

# N : the number of intervals for the modeling process

N = 200

# K : "speed of Mean-reversion

K_list = [0.002, 0.02, 0.2]

colors = ['k','g','b']

for index, K in enumerate(K_list):

N_plus_1, rate_list = CIR( r0, K, theta ,sigma, T, N )

plt.plot( N_plus_1, rate_list,

label='K=%s' % K,

c = colors[index]

)

plt.axhline(y=theta, ls='--', c='r') # Long-term mean(theta) of the process

plt.annotate( r'Long-term mean(${\theta}$)',

ha='left',

va='top',

xytext=(50, theta - 0.01), #The xytext parameter specifies the text position

xy=(50, theta), #The xy parameter specifies the arrow's destination

arrowprops=dict(facecolor='blue', headwidth=10, headlength=4, width=2 ),

#arrowprops={'facecolor':'blue', 'headwidth':10, 'headlength':4, 'width':2} #OR

fontsize=14

)

plt.legend( loc='upper left' , fontsize=14)

plt.ylabel('The interest rate$(R_t)$', fontsize=14)

plt.xlabel('the time t', fontsize=14)

plt.title('Cox-Ingersoll-Ross model', fontsize=14)

plt.show() "speed of reversion回归速度". K characterizes the velocity at which such trajectories will regroup around in time; K 表征这些轨迹将在时间

周围重新组合的速度

With higher levels of speed for mean reversion, K , the process reaches its long-term level of 0.15(the model reverts around the mean, θ=0.15) sooner.

With higher levels of speed for mean reversion, K , the process reaches its long-term level of 0.15(the model reverts around the mean, θ=0.15) sooner.

Observe that the CIR interest model does not have negative interest rate values.

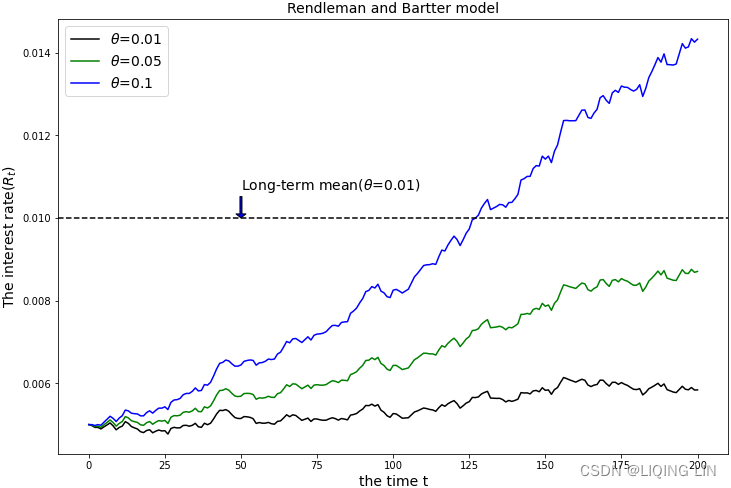

The Rendleman and Bartter model

The Rendleman and Bartter model (Richard J. Rendleman, Jr. and Brit J. Bartter) in finance is a short-rate model describing the evolution of interest rates. It is a "one factor model" as it describes interest rate movements as driven by only one source of market risk. It can be used in the valuation估值 of interest rate derivatives. It is a stochastic asset model.

In the Rendleman and Bartter model, the short-rate process is given as follows:

![]()

-

-

All future trajectories of -

- The standard deviation parameter,

Here, the instantaneous drift is θ*r(t) with an instantaneous standard deviation, σ*r(t). The Rendleman and Bartter model can be thought of as a geometric Brownian motion, akin to a stock price stochastic process that is log-normally distributed(https://blog.csdn.net/Linli522362242/article/details/96593981 ). This model lacks the property of mean reversion( no K : "speed of reversion回归速度". K characterizes the velocity at which such trajectories will regroup around

). This model lacks the property of mean reversion( no K : "speed of reversion回归速度". K characterizes the velocity at which such trajectories will regroup around in time; K 表征这些轨迹将在时间

周围重新组合的速度). Mean reversion is a phenomenon where the interest rates seem to be pulled back toward a long-term average level

.

The following Python code models the Rendleman and Bartter interest-rate process:

import math

import numpy as np

def rendleman_bartter( r0, theta, sigma, T=1, N=10, seed=777 ):

# r0 : the initial rate of interest at t=0

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

# T : the period in terms of number of years

# N : the number of intervals for the modeling process

# W : a Wiener process(Standard Brownian motion)

# modelling the random market risk factor(under the risk neutral framework)

np.random.seed( seed )

dt = T/float(N)

rates = [r0] # dW = sqrt(dt) * dZ

for i in range( N ): # Z is a standard normal variable

dr = theta*rates[-1]*dt + sigma*rates[-1]*math.sqrt(dt)*np.random.normal()

rates.append( rates[-1] + dr )

# returns a list of time periods and interest rates

return range(N+1), ratesWe will continue to use the example from the previous sections and compare the model.

Assume that the current interest rate is 0.5%, and sigma is 0.05 . We will use a T value of 10 and N of 200 to model the interest rates with different instantaneous drift, theta

, using values of 0.01 , 0.05 , and 0.1:

%matplotlib inline

import matplotlib.pyplot as plt

fig = plt.figure( figsize=(12,8) )

# r0 : the initial rate of interest at t=0

r0 = 0.005

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

sigma = 0.05

# T : the period in terms of number of years

T = 10

# N : the number of intervals for the modeling process

N = 200

colors = ['k','g','b']

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

theta_list = [0.01, 0.05, 0.1]

for index, theta in enumerate(theta_list):

N_plus_1, rate_list = rendleman_bartter( r0, theta, sigma, T, N )

plt.plot( N_plus_1, rate_list,

label=r'${\theta}$=%s' % theta,

c = colors[index]

)

plt.annotate( r'Long-term mean(${\theta}$=0.01)',

ha='left',

va='top',

xytext=(50, 0.01 + 0.001), # The xytext parameter specifies the text position

xy=(50, 0.01), # The xy parameter specifies the arrow's destination

arrowprops=dict(facecolor=colors[index], headwidth=10, headlength=4, width=2 ),

# arrowprops={'facecolor':'blue', 'headwidth':10, 'headlength':4, 'width':2} #OR

fontsize=14

)

plt.axhline(y=0.01, ls='--', c=colors[0]) # Long-term mean(theta) of the process

plt.legend( loc='upper left' , fontsize=14)

plt.ylabel('The interest rate$(R_t)$', fontsize=14)

plt.xlabel('the time t', fontsize=14)

plt.title('Rendleman and Bartter model', fontsize=14)

plt.show() In general, this model lacks the property of mean reversion and grows toward a long-term average level.

The Brennan and Schwartz model

The Brennan and Schwartz model is a two-factor model where the short-rate reverts toward a long-term rate as the mean

, which also follows a stochastic process. (The Brennan and Schwartz model is a two factors model that models the dynamics of the short and long term rates.

![]() ,

, ![]() ==>

==>

![]() ,

, ![]() ==>

==>

http://www.ericbenhamou.net/documents/Encyclo/Brennan%20and%20Schwartz%20_1982_%20model.pdf

OR https://web.mst.edu/~bohner/fim-10/fim-chap6.pdf

)

The short-rate process is given as follows(

The Brennan-Schwartz model is one of the one-factor stochastic differential equation models and it represents the dynamics of the short-rate. It is a "one factor model" as it describes interest rate movements as driven by only one source of market risk): http://trihandika.staff.gunadarma.ac.id/Publications/files/1558/ICREM.pdf==>

-

is called diffusion coefficient(扩散系数) of the process

The drift coefficient

If

if -

All future trajectories of -

K Mean-reversion factor

"speed of reversion回归速度". K characterizes the velocity at which such trajectories will regroup around -

- The standard deviation parameter,

- K and

increasingOR

increases

It can be seen that the Brennan and Schwartz model is another form of a geometric Brownian motion(https://blog.csdn.net/Linli522362242/article/details/125355166).

import math

import numpy as np

def rendleman_bartter( r0, theta, sigma, T=1, N=10, seed=777 ):

# r0 : the initial rate of interest at t=0

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

# T : the period in terms of number of years

# N : the number of intervals for the modeling process

# W : a Wiener process(Standard Brownian motion)

# modelling the random market risk factor(under the risk neutral framework)

np.random.seed( seed )

dt = T/float(N)

rates = [r0] # dW = sqrt(dt) * dZ

for i in range( N ): # Z is a standard normal variable

dr = theta*rates[-1]*dt + sigma*rates[-1]*math.sqrt(dt)*np.random.normal()

rates.append( rates[-1] + dr )

return range(N+1), ratesAssume that the current interest rate remains at 0.5%, and the long-term mean level of theta is 0.006. sigma is 0.05 . We will use a T value of 10 and N of 200 to model the interest rates with different speeds of mean reversion, K , using values of 0 2 , 0.02 , and 0.002

%matplotlib inline

import matplotlib.pyplot as plt

fig = plt.figure( figsize=(12,8) )

# r0 : the initial rate of interest at t=0

r0 = 0.005

# K : "speed of Mean-reversion

# theta : All future trajectories of r(t) will evolve around a 'mean' level 'theta' in the long run

theta = 0.006 # long-term mean level of theta

# sigma : determines the volatility of the interest rate and amplitude(range of r(t))

sigma = 0.05

# T : the period in terms of number of years

T = 10

# N : the number of intervals for the modeling process

N = 200

# K : "speed of Mean-reversion

K_list = [0.2, 0.02, 0.002]

colors = ['k','g','b']

for index, K in enumerate(K_list):

N_plus_1, rate_list =brennan_schwartz( r0, K, theta ,sigma, T, N )

plt.plot( N_plus_1, rate_list,

label='K=%s' % K,

c = colors[index]

)

plt.axhline(y=theta, ls='--', c='r') # Long-term mean(theta) of the process

plt.annotate( r'Long-term mean(${\theta}$=%s)' % theta,

ha='center',

va='top',

xytext=(50, theta - 0.0001), #The xytext parameter specifies the text position

xy=(50, theta), #The xy parameter specifies the arrow's destination

arrowprops=dict(facecolor='blue', headwidth=10, headlength=4, width=2 ),

#arrowprops={'facecolor':'blue', 'headwidth':10, 'headlength':4, 'width':2} #OR

fontsize=14

)

plt.legend( loc='upper left' , fontsize=14)

plt.ylabel('The interest rate$(R_t)$', fontsize=14)

plt.xlabel('the time t', fontsize=14)

plt.title('Brennan and Schwartz model', fontsize=14)

plt.show()

When K is 0.2, the speed of the mean reversion is fastest toward the long-term mean of 0.006.

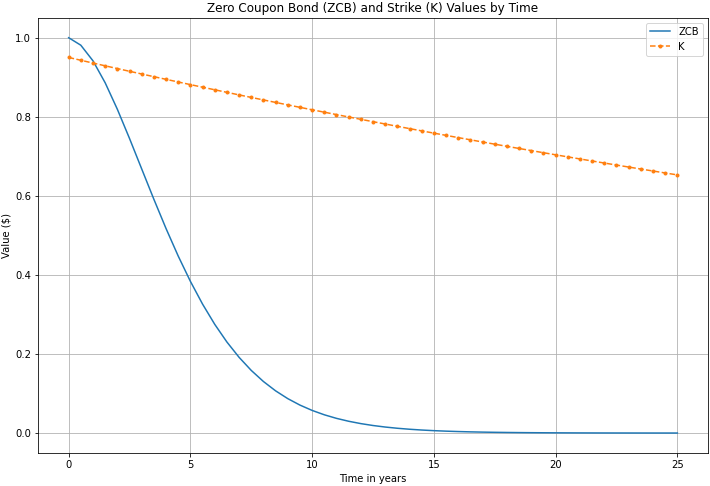

Bond options

When bond issuers, such as corporations, issue bonds, one of the risks they face is the interest rate risk.

- When interest rates(yields) decrease, bond prices increase.

- While existing bondholders will find their bonds more valuable,

- bond issuers, on the other hand, find themselves in a losing position, since they will be issuing higher-interest payments(Coupons) than the prevailing interest rate.

- Conversely, when interest rates increase,

- bond issuers are at an advantage, since they are able to continue issuing the same low-interest payments as agreed to on the bond-contract specifications.

To capitalize on利用 interest-rate changes, bond issuers may embed options within a bond. This allows the issuer the right, but not the obligation, to buy or sell the issued bond at a predetermined price during a specified period of time. An American type of bond option allows the issuer to exercise the rights of the option at any point in time during the lifetime of a bond. A European type of bond option allows the issuer to exercise the rights of the option on a specific date. The exact style of the date of exercise行使日期的确切样式 varies from bond option to bond option. Some issuers may choose to exercise the right of the bond option when the bond has been in circulation流通 in the market for over a year. Some issuers may choose to exercise the bond option on one of several specific dates. Regardless of the exercise dates of the bond, you may price the bond with an embedded option, as follows:

Price of bond = price of bond with no option - price of embedded option

The pricing of a bond with no option is fairly straightforward: the present value of the bond to be received at a future date, including all coupon payments. A number of assumptions are to be made about the theoretical interest rates in the future at which the coupon payments may be reinvested.

- One such assumption might be the movement of interest rates as implied by short-rate models, which we covered in the preceding section, Short-rate modeling.

- Another assumption might be the movement of interest rates within a binomial or trinomial tree. For simplicity, in bond-pricing studies, we will price zero-coupon bonds that will not issue coupons during the lifetime of the bond.

To price an option, one would have to determine available exercise dates. Starting from the future value of the bond, the bond price is compared against the exercise price of the option and traverses back to the present time using a numerical procedurehttps://blog.csdn.net/Linli522362242/article/details/125355166, such as a binomial tree. This price comparison is performed at time points when the bond option may be exercised. With the no-arbitrage theory, accounting for the present excess values of the bond when exercised, we obtain the price of the option. For simplicity, in bond-pricing studies in the later section of this chapter, Pricing callable bond options, we will treat the embedded option of zero-coupon bonds as an American option.

Callable bonds可赎回债券

In an economic condition where there are high interest rates, bond issuers are likely at risk of facing an interest-rate decrease( y![]() ,

,

- While existing bondholders will find their bonds more valuable(BP

),

),

) and having to continue to issue higher-interest payments(Coupons) than the prevailing interest rate. As such, they may choose to issue callable bonds. A callable bond contains an embedded agreement to redeem赎回(股票/债券等) the bond at agreed dates. Existing bond holders are considered to have sold a call option to the bond issuer.

In the event that interest rates fall(y![]() , BP

, BP![]() ) and the corporation has the right to exercise the option to buy back the bond during that period at a specific price(K, a call option's profit

) and the corporation has the right to exercise the option to buy back the bond during that period at a specific price(K, a call option's profit![]() =BP