本文介绍了Black-Scholes模型用于欧式期权(看涨和看跌)定价的原理,给出了数学公式,并提供了Python代码实现,展示了如何计算期权价格以及模拟股票价格路径。

本文介绍了Black-Scholes模型用于欧式期权(看涨和看跌)定价的原理,给出了数学公式,并提供了Python代码实现,展示了如何计算期权价格以及模拟股票价格路径。

欧式期权定价的一个常用模型是Black-Scholes模型。这个模型假设股票价格遵循几何布朗运动,并且无风险利率和股票的波动率都是已知的。

欧式看涨期权(Call Option)和欧式看跌期权(Put Option)的Black-Scholes定价模型:

对于欧式看涨期权的价格 ( C ),公式为:

对于欧式看跌期权的价格 ( P ),公式为:

其中:

S 是标的资产的当前价格,

X 是期权的执行价格,

r 是无风险利率,

T 是期权的到期时间(以年为单位),

是标的资产的波动率,

N(d) 是标准正态分布的累积分布函数,

和

是由以下公式定义的:

Python实现如下:

import math

import random

import matplotlib.pyplot as plt

def black_scholes(cp, s, k, t, v, r, q=0.0):

"""Price an option using the Black-Scholes model.

cp: +1/-1 for call/put

s: initial stock price

k: strike price

t: expiration time

v: volatility

r: risk-free rate

q: dividend rate

"""

d1 = (math.log(s / k) + (r - q + 0.5 * v ** 2) * t) / (v * math.sqrt(t))

d2 = d1 - v * math.sqrt(t)

if cp == 1: # Call option

price = math.exp(-r * t) * (s * math.exp((r - q) * t) * norm_cdf(d1) - k * norm_cdf(d2))

elif cp == -1: # Put option

price = math.exp(-r * t) * (k * norm_cdf(-d2) - s * math.exp((r - q) * t) * norm_cdf(-d1))

return price

def norm_cdf(x):

"""Cumulative distribution function for the standard normal distribution."""

# Abramowitz & Stegun approximation

# This is a simplified version that does not handle extreme values well.

# For production use, consider a more robust implementation.

a1 = 0.254829592

a2 = -0.284496736

a3 = 1.421413741

a4 = -1.453152027

a5 = 1.061405429

p = 0.3275911

# Save the sign of x

sign = 1.0 if x >= 0 else -1.0

x = abs(x)

# Abramowitz & Stegun formula 7.1.26

t = 1.0 / (1.0 + p * x)

y = (((((a5 * t + a4) * t) + a3) * t + a2) * t + a1) * t

return 0.5 * (1.0 + sign * (1.0 - y * math.exp(-x * x / 2.0)))

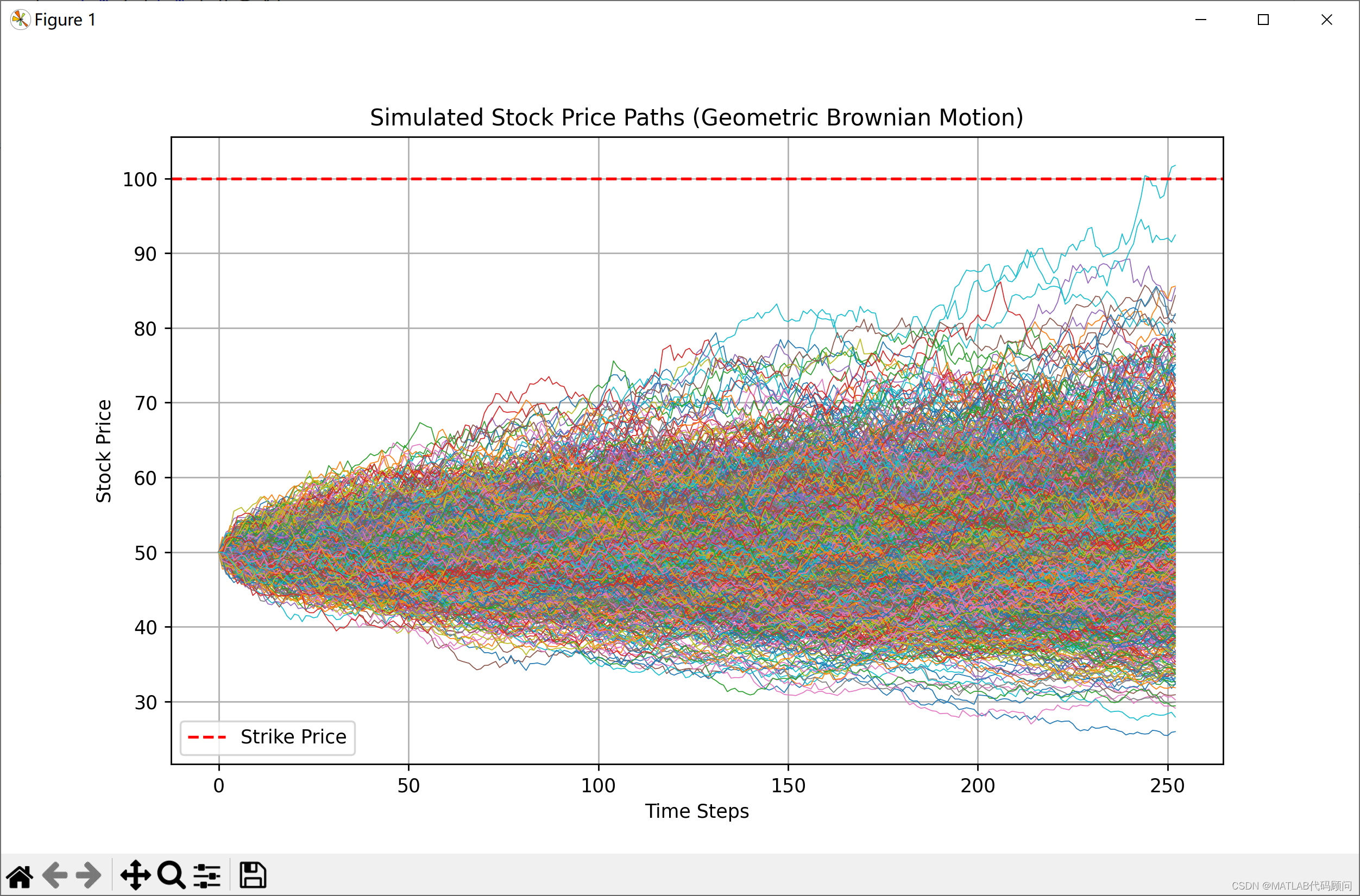

# Parameters for the option pricing and simulation

s = 50.0 # Initial stock price

k = 100.0 # Strike price

t = 1.0 # Expiration time (in years)

v = 0.2 # Volatility

r = 0.05 # Risk-free rate

q = 0.0 # Dividend rate

num_steps = 252 # Number of time steps for the simulation (e.g., 252 trading days in a year)

num_simulations = 1000 # Number of simulations to run (for plotting multiple paths)

dt = t / num_steps # Time increment for each step

# Calculate option prices

call_price = black_scholes(1, s, k, t, v, r, q)

put_price = black_scholes(-1, s, k, t, v, r, q)

print(f"Call Price: {call_price}")

print(f"Put Price: {put_price}")

# Simulate stock price paths

price_paths = []

for _ in range(num_simulations):

path = [s] # Start with the initial stock price

current_price = s

for _ in range(num_steps):

drift = r * current_price * dt

diffusion = v * current_price * math.sqrt(dt) * random.gauss(0, 1)

current_price += drift + diffusion

path.append(current_price)

price_paths.append(path)

# Plot the stock price paths

plt.figure(figsize=(10, 6))

for path in price_paths:

plt.plot(path, lw=0.5) # lw sets the line width

plt.axhline(y=k, color='r', linestyle='--', label='Strike Price')

plt.xlabel('Time Steps')

plt.ylabel('Stock Price')

plt.title('Simulated Stock Price Paths (Geometric Brownian Motion)')

plt.legend()

plt.grid(True)

plt.show()

755

755

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言