逻辑回归是一种应用非常广泛的分类算法,同时也广泛地用于排序场景。如果样本集是线性可分的,逻辑回归是一个效果比较好的分类器。对于非线性特征,可以通过特征工程将其线性化。这种算法本身不具有选择重要特征的功能,通常利用l2或l1正则化方法(关于l2和l1的对比参见)做特征选择。由于逻辑回归的计算简单,具有高效性,它可以用于大数据场景,也可以利用分布式计算来加速。

下面是利用MATLAB求解带有L1正则项逻辑回归的相关代码:

非分布式版本:

function [z, history] = logreg(A, b, mu, rho, alpha)

% logreg Solve L1 regularized logistic regression via ADMM

%

% [z, history] = logreg(A, b, mu, rho, alpha)

%

% solves the following problem via ADMM:

%

% minimize sum( log(1 + exp(-b_i*(a_i'w + v)) ) + m*mu*norm(w,1)

%

% where A is a feature matrix and b is a response vector. The scalar m is

% the number of examples in the matrix A.

%

% This solves the L1 regularized logistic regression problem. It uses

% a custom Newton solver for the x-step.

%

% The solution is returned in the vector x = (v,w).

%

% history is a structure that contains the objective value, the primal and

% dual residual norms, and the tolerances for the primal and dual residual

% norms at each iteration.

%

% rho is the augmented Lagrangian parameter.

%

% alpha is the over-relaxation parameter (typical values for alpha are

% between 1.0 and 1.8).

%

%

% More information can be found in the paper linked at:

% http://www.stanford.edu/~boyd/papers/distr_opt_stat_learning_admm.html

%

t_start = tic;

Global constants and defaults

QUIET = 0; MAX_ITER = 1000; ABSTOL = 1e-4; RELTOL = 1e-2;

Data preprocessing

[m, n] = size(A);

ADMM solver

x = zeros(n+1,1); z = zeros(n+1,1); u = zeros(n+1,1);

if ~QUIET fprintf('%3s\t%10s\t%10s\t%10s\t%10s\t%10s\n', 'iter', ... 'r norm', 'eps pri', 's norm', 'eps dual', 'objective');

end

for k = 1:MAX_ITER % x-update x = update_x(A, b, u, z, rho); % z-update with relaxation zold = z; x_hat = alpha*x + (1-alpha)*zold; z = x_hat + u; z(2:end) = shrinkage(z(2:end), (m*mu)/rho); u = u + (x_hat - z); % diagnostics, reporting, termination checks history.objval(k) = objective(A, b, mu, x, z); history.r_norm(k) = norm(x - z); history.s_norm(k) = norm(rho*(z - zold)); history.eps_pri(k) = sqrt(n)*ABSTOL + RELTOL*max(norm(x), norm(z)); history.eps_dual(k)= sqrt(n)*ABSTOL + RELTOL*norm(rho*u);

if ~QUIET fprintf('%3d\t%10.4f\t%10.4f\t%10.4f\t%10.4f\t%10.2f\n', k, ... history.r_norm(k), history.eps_pri(k), ... history.s_norm(k), history.eps_dual(k), history.objval(k));

end if history.r_norm(k) < history.eps_pri(k) && ... history.s_norm(k) < history.eps_dual(k)

break;

endend

if ~QUIET toc(t_start);

end

end

function obj = objective(A, b, mu, x, z) m = size(A,1); obj = sum(log(1 + exp(-A*x(2:end) - b*x(1)))) + m*mu*norm(z,1);

end

function x = update_x(A, b, u, z, rho, x0) % solve the x update % minimize [ -logistic(x_i) + (rho/2)||x_i - z^k + u^k||^2 ] % via Newton's method; for a single subsystem only. alpha = 0.1; BETA = 0.5; TOLERANCE = 1e-5; MAX_ITER = 50; [m n] = size(A); I = eye(n+1);

if exist('x0', 'var') x = x0; else x = zeros(n+1,1);

end C = [-b -A]; f = @(w) (sum(log(1 + exp(C*w))) + (rho/2)*norm(w - z + u).^2);

for iter = 1:MAX_ITER fx = f(x); g = C'*(exp(C*x)./(1 + exp(C*x))) + rho*(x - z + u); H = C' * diag(exp(C*x)./(1 + exp(C*x)).^2) * C + rho*I; dx = -H\g; % Newton step dfx = g'*dx; % Newton decrement if abs(dfx) < TOLERANCE

break;

end % backtracking t = 1;

while f(x + t*dx) > fx + alpha*t*dfx t = BETA*t;

end x = x + t*dx;

end

end

function z = shrinkage(a, kappa) z = max(0, a-kappa) - max(0, -a-kappa);

end

下面是分布式实现:

function [z, history] = distr_l1_logreg(A, b, mu, N, rho, alpha)

% distr_l1_logreg Solve distributed L1 regularized logistic regression

%

% [x, history] = distr_l1_logreg(A, b, mu, N, rho, alpha)

%

% solves the following problem via ADMM:

%

% minimize sum( log(1 + exp(-b_i*(a_i'w + v)) ) + m*mu*norm(w,1)

%

% where A is a feature matrix and b is a response vector. The scalar m is

% the number of examples in the matrix A.

%

% This solves the L1 regularized logistic regression problem. It uses

% a custom Newton solver for the x-step. This version solves a distributed

% version of L1 regularized logistic regression.

%

% The solution is returned in the vector x = (v,w).

%

% history is a structure that contains the objective value, the primal and

% dual residual norms, and the tolerances for the primal and dual residual

% norms at each iteration.

%

% N is the number of subsystems to use to split the examples. This code

% will (serially) solve N x-updates with m / N examples per subsystem.

% Therefore, the number of examples, m, should be divisible by N. No error

% checking is done.

%

% rho is the augmented Lagrangian parameter.

%

% alpha is the over-relaxation parameter (typical values for alpha are

% between 1.0 and 1.8).

%

% This example requires the "MATLAB Interface for L-BFGS-B" and L-BFGS-B

% installed. These can be acquiured at

% http://www.cs.ubc.ca/~pcarbo/lbfgsb-for-matlab.html.

%

%

% More information can be found in the paper linked at:

% http://www.stanford.edu/~boyd/papers/distr_opt_stat_learning_admm.html

%

t_start = tic;

Global constants and defaults

QUIET = 0; MAX_ITER = 1000; ABSTOL = 1e-4; RELTOL = 1e-2;

Preprocessing

[m, n] = size(A);

m = m / N; % should be divisible

ADMM solver

x = zeros(n+1,N); z = zeros(n+1,N); u = zeros(n+1,N);

if ~QUIET fprintf('%3s\t%10s\t%10s\t%10s\t%10s\t%10s\t%10s\n', 'iter', '# bfgs', ... 'r norm', 'eps pri', 's norm', 'eps dual', 'objective');

end

p = size(z,1); C = [-b -A]';

global BFGS_ITERS; % global variable to keep track of bfgs iterations

bfgs_iters = zeros(N,1);

for k = 1:MAX_ITER % serial x-update for i = 1:N, K = C(:,1+(i-1)*m:i*m)'; x(:,i) = bfgs_update(K, u(:,i), z(:,i), rho, N, x(:,i)); bfgs_iters(i) = BFGS_ITERS;

end % z-update with relaxation zold = z; x_hat = alpha*x + (1-alpha)*zold; ztilde = mean(x_hat + u,2); ztilde(2:end) = shrinkage( ztilde(2:end), (m*N)*mu/(rho*N) ); z = ztilde*ones(1,N); % u-update u = u + (x_hat - z); % diagnostics, reporting, termination checks history.objval(k) = objective(A, b, mu, x, z(:,1)); history.r_norm(k) = norm(x - z, 'fro'); history.s_norm(k) = norm(rho*(z - zold),'fro'); history.LBFGS_iters(:,k) = bfgs_iters; history.eps_pri(k) = sqrt(p*N)*ABSTOL + RELTOL*max(norm(x,'fro'), norm(z,'fro')); history.eps_dual(k)= sqrt(p*N)*ABSTOL + RELTOL*norm(rho*u,'fro');

if ~QUIET fprintf('%3d\t%10d\t%10.4f\t%10.4f\t%10.4f\t%10.4f\t%10.2f\n', k, sum(bfgs_iters), ... history.r_norm(k), history.eps_pri(k), ... history.s_norm(k), history.eps_dual(k), history.objval(k));

end if history.r_norm(k) < history.eps_pri(k) && ... history.s_norm(k) < history.eps_dual(k)

break;

end

end

if ~QUIET toc(t_start);

end

z = z(:,1);

end

function obj = objective(A, b, mu, x, z) m = size(A,1); obj = sum(log(1 + exp(-A*z(2:end) -b*z(1)))) + m*mu*norm(z(2:end),1);

end

function [x t] = bfgs_update(C, u, z, rho, N, x0) % solve the x update % minimize [ -logistic(x_i) + (rho/2)||x_i - z^k + u^k||^2 ] % via L-BFGS [m n] = size(C); auxdata{1} = C; auxdata{2} = z; auxdata{3} = u; auxdata{4} = rho; x = lbfgsb(x0, -Inf*ones(n,1), +Inf*ones(n,1), 'l2_log', 'l2_log_grad', auxdata, 'record_bfgs_iters');

end

function z = shrinkage(a, kappa) z = max(0, a-kappa) - max(0, -a-kappa);

end

总结下logistic regression的优缺点。

优点:

实现简单,较多地应用于工业问题(如商品排序,商品推荐)上;

计算量比较小,速度快,所需存储资源低;

能够给出观测样本概率分数,方便排序;

可以利用L2正则化来解决多重共线性问题;

缺点:

当特征空间(样本维数)很大时,性能不是很好;

容易欠拟合,可能会导致准确度较低;

只能处理二分类问题(泛化版本softmax可用于多分类),需线性可分;

对于非线性特征,需要利用特诊工程方法进行转换,使其线性化;

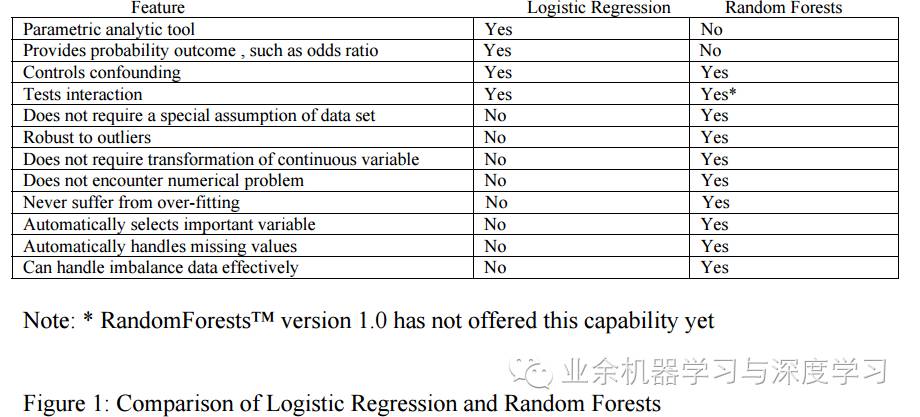

最后给出逻辑回归和随机森林的对比图,顺便预告一下下篇内容(什么内容呢,且听下回分解)

参考资料:

https://www.quora.com/What-are-the-advantages-of-different-classification-algorithms

http://d-scholarship.pitt.edu/7034/1/realfinalplus_ETD2006.pdf

代码来源:

https://web.stanford.edu/~boyd/papers/admm/logreg-l1/distr_l1_logreg.html

https://web.stanford.edu/~boyd/papers/admm/logreg-l1/logreg.html

4258

4258

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言