写在前面:

1. 本文中提到的“K线形态查看工具”的具体使用操作请查看该博文;

2. K线形体所处背景,诸如处在上升趋势、下降趋势、盘整等,背景内容在K线形态策略代码中没有体现;

3. 文中知识内容来自书籍《K线技术分析》by邱立波。

目录

解说

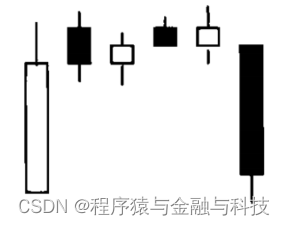

塔形顶是在上涨过程中收出一根大阳线或中阳线,接着再阳线顶部收出几根小阴线和小阳线,最后收出一根大阴线或中阴线。塔形顶因其形状像一个塔顶而得名。

技术特征

1)出现在上涨趋势中。

2)先是一根大阳线或中阳线,接着在阳线上方收出一连串小阴线、小阳线,最后出现一根大阴线或中阴线。

技术含义

塔形顶是见顶反转信号,后市看跌,卖出。

塔形顶是和塔形底相对的K线形态,表明多方已是强弩之末,无力继续推高股价。大阳线或中阳线之后出现的小阴线和小阳线横盘整理,逐步将多方仅剩的一点能量耗尽,最后一根大阴线或中阴线是空方拉开了大反攻的序幕,也确认了趋势由上涨转为下跌。交易者可在塔形顶收出大阴线或中阴线的当日或次日减仓或清仓。

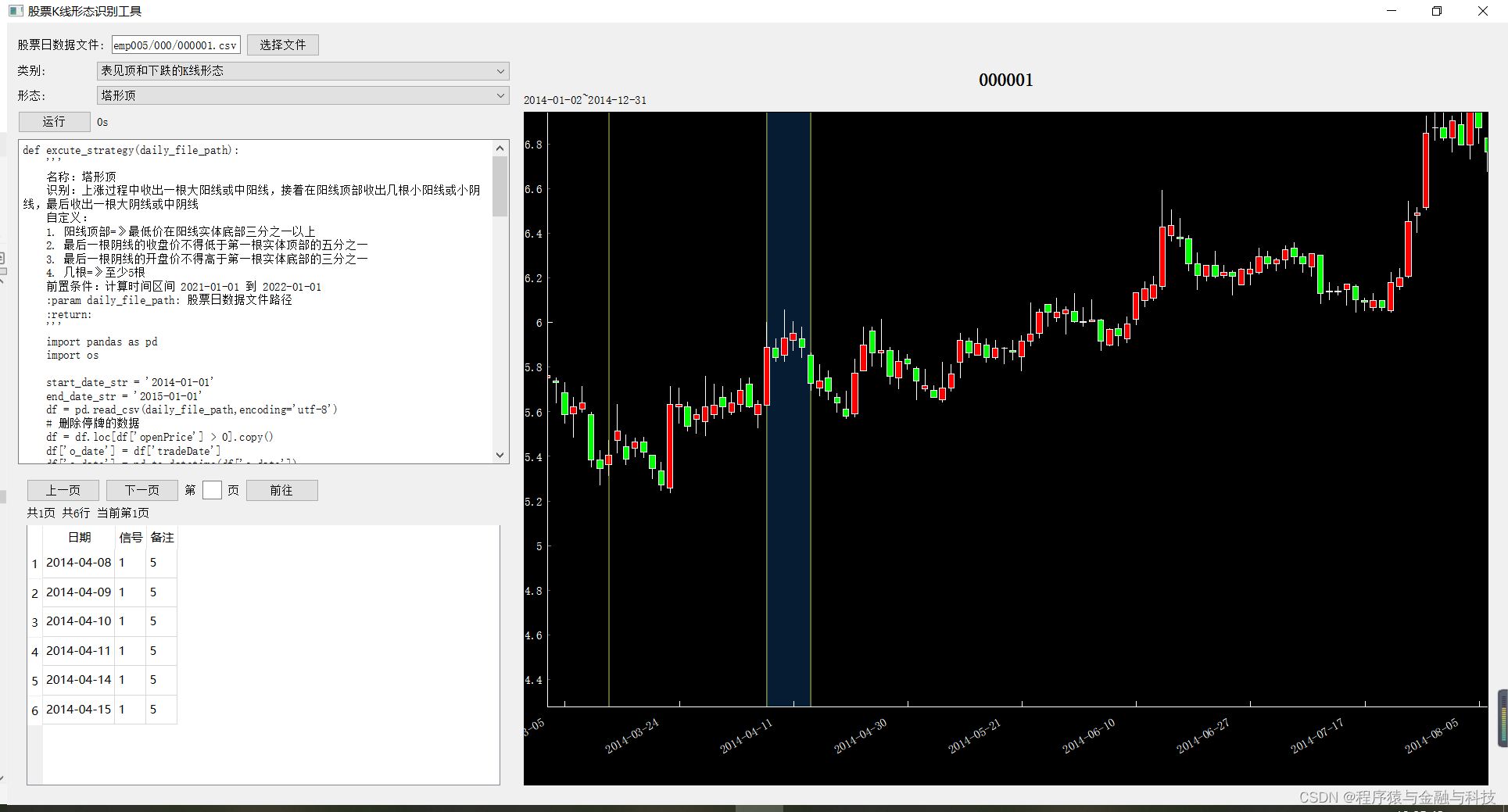

K线形态策略代码

def excute_strategy(daily_file_path):

'''

名称:塔形顶

识别:上涨过程中收出一根大阳线或中阳线,接着在阳线顶部收出几根小阳线或小阴线,最后收出一根大阴线或中阴线

自定义:

1. 阳线顶部=》最低价在阳线实体底部三分之一以上

2. 最后一根阴线的收盘价不得低于第一根实体顶部的五分之一

3. 最后一根阴线的开盘价不得高于第一根实体底部的三分之一

4. 几根=》至少5根

前置条件:计算时间区间 2021-01-01 到 2022-01-01

:param daily_file_path: 股票日数据文件路径

:return:

'''

import pandas as pd

import os

start_date_str = '2014-01-01'

end_date_str = '2015-01-01'

df = pd.read_csv(daily_file_path,encoding='utf-8')

# 删除停牌的数据

df = df.loc[df['openPrice'] > 0].copy()

df['o_date'] = df['tradeDate']

df['o_date'] = pd.to_datetime(df['o_date'])

df = df.loc[(df['o_date'] >= start_date_str) & (df['o_date']<=end_date_str)].copy()

# 保存未复权收盘价数据

df['close'] = df['closePrice']

# 计算前复权数据

df['openPrice'] = df['openPrice'] * df['accumAdjFactor']

df['closePrice'] = df['closePrice'] * df['accumAdjFactor']

df['highestPrice'] = df['highestPrice'] * df['accumAdjFactor']

df['lowestPrice'] = df['lowestPrice'] * df['accumAdjFactor']

# 开始计算

df['type'] = 0

df.loc[df['closePrice'] >= df['openPrice'], 'type'] = 1

df.loc[df['closePrice'] < df['openPrice'], 'type'] = -1

df['body_length'] = abs(df['closePrice']-df['openPrice'])

df['m_body_type'] = 0

df.loc[(df['type']==1) & (df['body_length']/df['closePrice'].shift(1)>0.02),'m_body_type'] = 2

df.loc[(df['type']==-1) & (df['body_length']/df['closePrice'].shift(1)>0.02),'m_body_type'] = 4

df['small_type'] = 0

df.loc[df['body_length']/df['closePrice'].shift(1)<0.015,'small_type'] = 1

df.reset_index(inplace=True)

df['i_row'] = [i for i in range(0,len(df))]

df_m_n = df.loc[df['m_body_type']==2].copy()

df_m_p = df.loc[df['m_body_type']==4].copy()

i_row_n = df_m_n['i_row'].values.tolist()

i_row_p = df_m_p['i_row'].values.tolist()

i_row_two = i_row_n + i_row_p

i_row_two.sort()

n_list = []

p_list = []

for i in range(0,len(i_row_two)-1):

if i_row_two[i] in i_row_n and i_row_two[i+1] in i_row_p:

n_list.append(i_row_two[i])

p_list.append(i_row_two[i+1])

pass

df['signal'] = 0

df['signal_name'] = ''

for n,p in zip(n_list,p_list):

if p-n < 5:

continue

enter_yeah = True

for i in range(n+1,p):

if df.iloc[i]['small_type']!=1:

enter_yeah = False

break

pass

if enter_yeah:

final_yeah = False

target_body_length = df.iloc[n]['body_length']

if (df.iloc[n]['openPrice'] + target_body_length*0.1) > df.iloc[p]['closePrice']:

continue

if (df.iloc[n]['closePrice'] - target_body_length*0.1) < df.iloc[p]['openPrice']:

continue

for m_i in range(n+1,p):

if (df.iloc[n]['closePrice'] - target_body_length*0.33) > df.iloc[m_i]['lowestPrice']:

final_yeah = True

break

if final_yeah:

continue

df.loc[(df['i_row']>=n) & (df['i_row']<=p),'signal'] = 1

df.loc[(df['i_row']>=n) & (df['i_row']<=p),'signal_name'] = str(p-n)

pass

file_name = os.path.basename(daily_file_path)

title_str = file_name.split('.')[0]

line_data = {

'title_str':title_str,

'whole_header':['日期','收','开','高','低'],

'whole_df':df,

'whole_pd_header':['tradeDate','closePrice','openPrice','highestPrice','lowestPrice'],

'start_date_str':start_date_str,

'end_date_str':end_date_str,

'signal_type':'duration_detail',

'duration_len':[],

'temp':len(df.loc[df['signal']==1])

}

return line_data结果

2326

2326

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言