本文介绍了如何使用Python中的statsmodels库来确定ARIMA模型的参数p、d、q。通过分析时间序列的自相关函数ACF和偏自相关函数PACF,确定了差分次数d,并探讨了ACF和PACF在模型构建中的作用。内容以历年美国消费者信心指数数据为例,展示了具体代码和分析过程。

本文介绍了如何使用Python中的statsmodels库来确定ARIMA模型的参数p、d、q。通过分析时间序列的自相关函数ACF和偏自相关函数PACF,确定了差分次数d,并探讨了ACF和PACF在模型构建中的作用。内容以历年美国消费者信心指数数据为例,展示了具体代码和分析过程。

参数d:

ARIMA 模型对时间序列的要求是平稳型。因此,当你得到一个非平稳的时间序列时,首先要做的即是做时间序列的差分,直到得到一个平稳时间序列。如果你对时间序列做d次差分才能得到一个平稳序列,那么可以使用ARIMA(p,d,q)模型,其中d是差分次数。

模型的参数p和q由ACF和PACF确定

如下表格

statsmodels介绍

statsmodels(http://www.statsmodels.org)是一个Python库,用于拟合多种统计模型,执行统计测试以及数据探索和可视化。statsmodels包含更多的“经典”频率学派统计方法,而贝叶斯方法和机器学习模型可在其他库中找到。

包含在statsmodels中的一些模型:

- 线性模型,广义线性模型和鲁棒线性模型

- 线性混合效应模型

- 方差分析(ANOVA)方法

- 时间序列过程和状态空间模型

- 广义的矩量法

我们使用其中的时间序列相关函数进行模型的构建。数据为历年美国消费者信心指数数据,代码如下:

%load_ext autoreload

%autoreload 2

%matplotlib inline

%config InlineBackend.figure_format='retina'

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

#Display and Plotting

import matplotlib.pylab as plt

import seaborn as sns

# pandas与numpy属性设置

pd.set_option('display.float_format',lambda x:'%.5f'%x)#pandas

np.set_printoptions(precision=5,suppress=True) #numpy

pd.set_option('display.max_columns',100)

pd.set_option('display.max_rows',100)

#seaborn.plotting style

sns.set(style='ticks',context='poster')

Sentiment='sentiment.csv'

Sentiment=pd.read_csv(Sentiment,index_col=0,parse_dates=[0])

Sentiment.head()

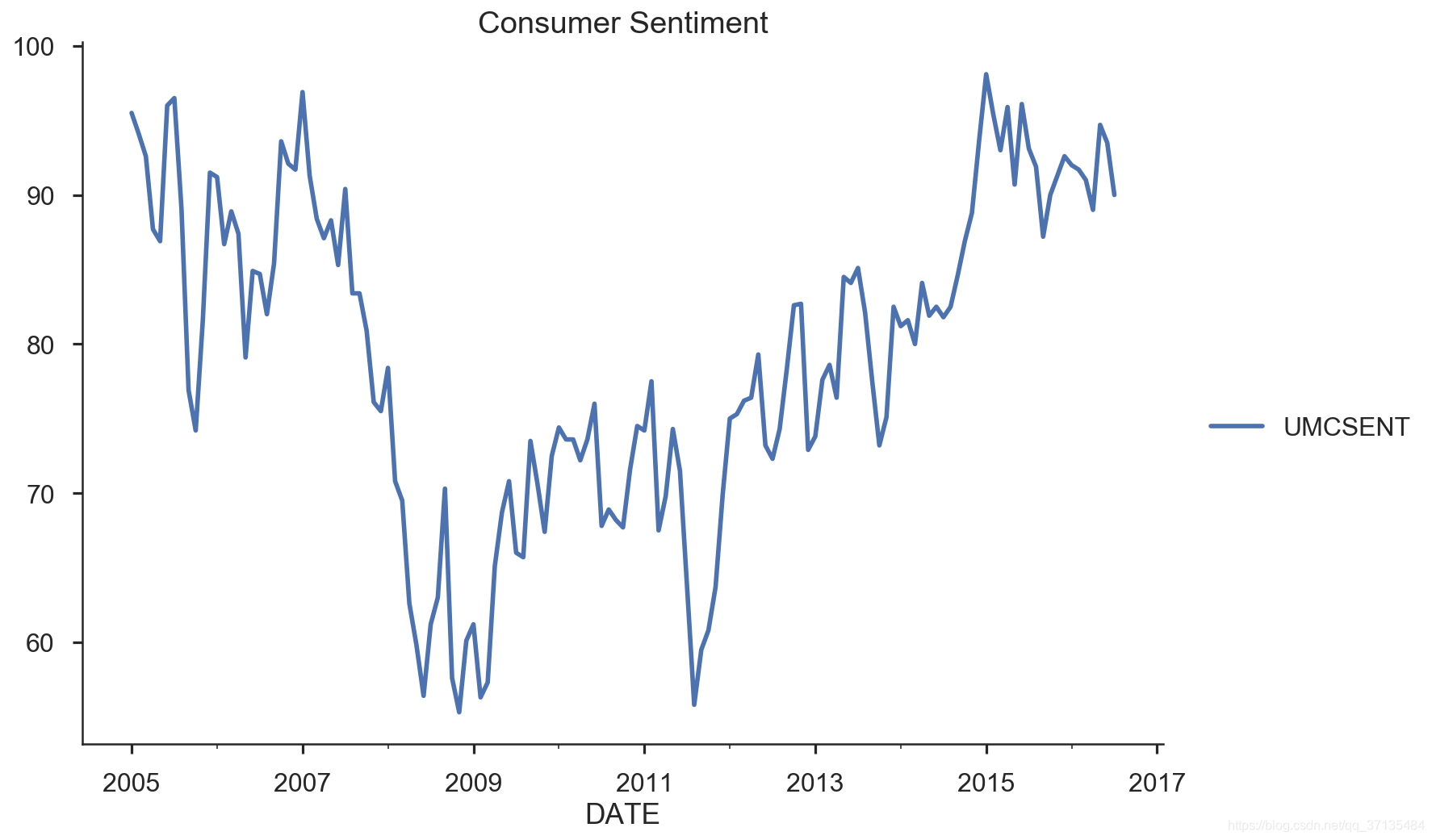

#选取时间断

sentiment_short=Sentiment.loc['2005':'2016']

sentiment_short.plot(figsize=(12,8))

plt.legend(bbox_to_anchor=(1.25,0.5))

plt.title('Consumer Sentiment')

sns.despine()

#help(sentiment_short['UMCSENT'].diff(1))

#函数diss()作用:https://blog.csdn.net/qq_32618817/article/details/80653841#

#https://blog.csdn.net/You_are_my_dream/article/details/700 最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

2812

2812

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言