1.案例背景

-

数据说明:这一份数据是信用卡的消费使用数据,其中数据涉及到一些隐私的内容,里面的相关数据特征已经经过了处理,我们拿到的数据并不是最原始的数据。我们通过逻辑回归来预测信用卡异常的数据。

-

观察数据

代码:

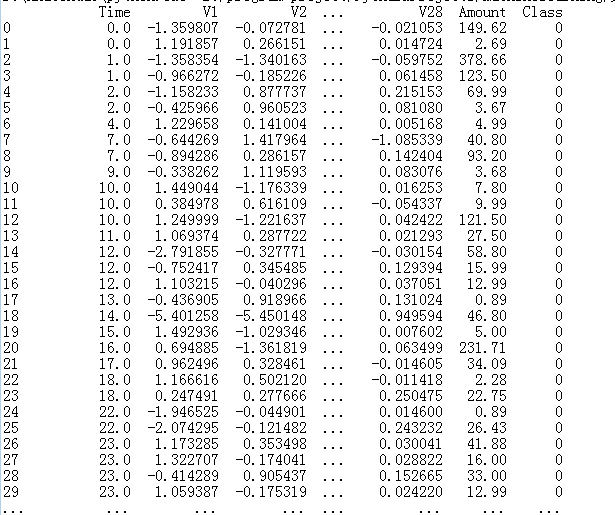

import pandas as pd import numpy as np import matplotlib.pyplot as plt data = pd.read_csv('data/creditcard.csv') data.head() print(data)

time 对我们来说是没有用的,我们待会会将这一部分去掉。amount代表着交易的金额。在V1~V28 的数据比较小,而amount数据都比较大,所以要对数据进行预处理操作。

属于0 这个类是正常的,属于1 这个类是异常的。我们的目的是进行分类任务。绝大多数样本是正样本,少数样本是负样本。

2.样本不平衡的解决方案

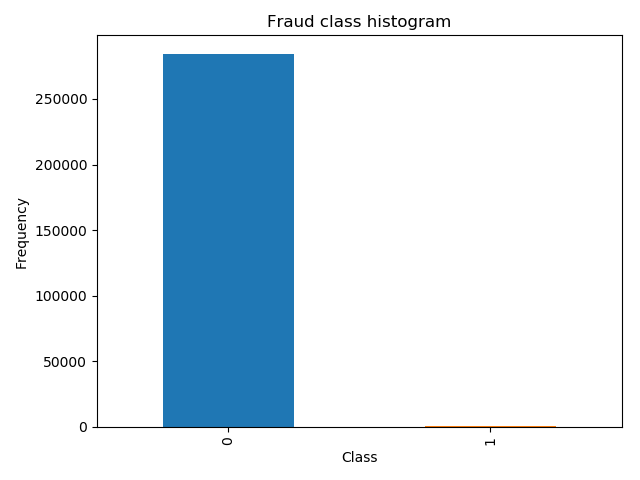

# 观察样本的分布规则 count_classes = pd.value_counts(data['Class'],sort=True) count_classes.plot(kind='bar') plt.title("Fraud class histogram") plt.xlabel("Class") plt.ylabel("Frequency") plt.show()

从中可以观察到,正负样本不均衡。

这里有两种解决方案:1.下采样 :让0和1 两个样本一样小 2. 过采样: 对1号 样本进行生成,让 0 和 1 这两个样本一样多。

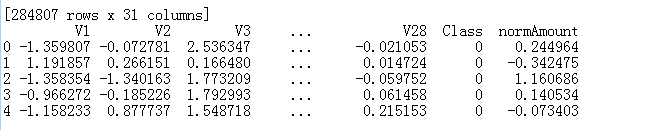

我们在这里并没有说amount特征比较重要,所以这里先进行归一化操作!

from sklearn.preprocessing import StandardScaler data['normAmount'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1, 1)) data = data.drop(['Time','Amount'],axis=1) print(data.head())

这里得到了我们可以直接使用的特征数据。

-

下采样策略

# 下采样,使得两个样本同样少 X = data.ix[:, data.columns != 'Class'] y = data.ix[:, data.columns == 'Class'] # Number of data points in the minority class number_records_fraud = len(data[data.Class == 1])# 计算异常样本的个数 fraud_indices = np.array(data[data.Class == 1].index) # 异常样本在原数据的索引值 # Picking the indices of the normal classes normal_indices = data[data.Class == 0].index # 获得原数据正常样本的索引值 # Out of the indices we picked, randomly select "x" number (number_records_fraud) random_normal_indices = np.random.choice(normal_indices, number_records_fraud, replace = False) # 通过索引进行随机的选择 random_normal_indices = np.array(random_normal_indices) # Appending the 2 indices under_sample_indices = np.concatenate([fraud_indices,random_normal_indices]) # 将class=1和class=0 的选出来的索引值进行合并 # Under sample dataset under_sample_data = data.iloc[under_sample_indices,:] X_undersample = under_sample_data.ix[:, under_sample_data.columns != 'Class'] y_undersample = under_sample_data.ix[:, under_sample_data.columns == 'Class'] # Showing ratio print("Percentage of normal transactions: ", len(under_sample_data[under_sample_data.Class == 0])/len(under_sample_data)) print("Percentage of fraud transactions: ", len(under_sample_data[under_sample_data.Class == 1])/len(under_sample_data)) print("Total number of transactions in resampled data: ", len(under_sample_data))Percentage of normal transactions: 0.5

Percentage of fraud transactions: 0.5

Total number of transactions in resampled data: 984

-

3.交叉验证

目的

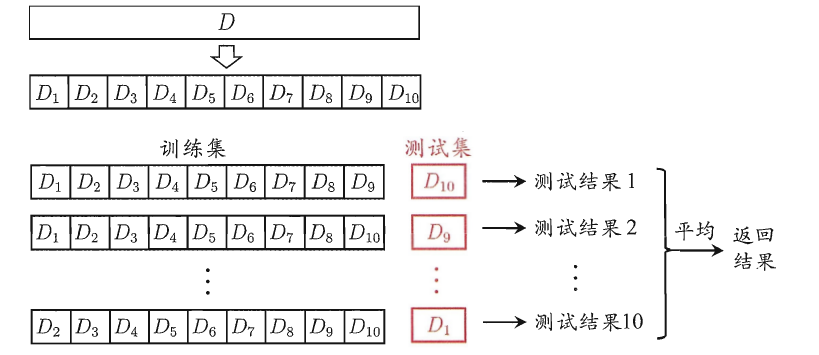

交叉验证法的作用就是尝试利用不同的训练集/验证集划分来对模型做多组不同的训练/验证,来应对单独测试结果过于片面以及训练数据不足的问题。(就像通过多次考试,才通知哪些学生是比较比较牛B的)

交叉验证的做法就是将数据集粗略地分为比较均等不相交的k份,然后取其中的一份进行测试,另外的k-1份进行训练,然后求得error的平均值作为最终的评价,具体算法流程如下:

-

在有监督(supervise)的机器学习中,数据集常被分成2~3个,即:训练集(train set),验证集(validation set),测试集(test set)

一个形象的比喻:

**训练集-----------**学生的课本;学生 根据课本里的内容来掌握知识。

验证集------------作业,通过作业可以知道 不同学生学习情况、进步的速度快慢。

测试集-----------考试,考的题是平常都没有见过,考察学生举一反三的能力。

传统上,一般三者切分的比例是:6:2:2,验证集并不是必须的。

为什么要测试集

a)训练集直接参与了模型调参的过程,显然不能用来反映模型真实的能力(防止课本死记硬背的学生拥有最好的成绩,即防止过拟合)

b)验证集参与了人工调参(超参数)的过程,也不能用来最终评判一个模型(刷题库的学生不能算是学习好的学生)。

c) 所以要通过最终的考试(测试集)来考察一个学(模)生(型)真正的能力**(期末考试)**

但是仅凭一次考试就对模型的好坏进行评判显然是不合理的,所以接下来就要介绍交叉验证法

from sklearn.model_selection import train_test_split # Whole dataset X_train, X_test, y_train, y_test = train_test_split(X,y,test_size = 0.3, random_state = 0) print("Number transactions train dataset: ", len(X_train)) print("Number transactions test dataset: ", len(X_test)) print("Total number of transactions: ", len(X_train)+len(X_test)) # Undersampled dataset X_train_undersample, X_test_undersample, y_train_undersample, y_test_undersample = train_test_split(X_u

最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

5030

5030

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言