数据源:akshare

策略:双均线策略购买股票,卖出50指数期货对冲

导包:

#导包

import akshare as ak

import pandas as pd

import numpy as np

import matplotlib

import matplotlib.pyplot as plt

import numpy as np

import matplotlib.pyplot as plot

import datetime

import talib #计算均线的库,随便学一下,几分钟就懂

matplotlib.rcParams['axes.unicode_minus']=False #调整图像,可以注释掉,一般还是可以运行

plt.rcParams['font.sans-serif']=['SimHei'] #用来正常显示中文标签

plt.rcParams['axes.unicode_minus']=False #用来正常显示负号获取50成分股票:

#股票列表

import akshare as ak

index_stock_info_df = ak.index_stock_cons('000016')根据每个股票数据构建策略,并计算策略收益率:

star='20170117'

end="20230810"

last = pd.DataFrame()

last['trade_date'] = 0

last['strategy'] = 0

for i in stock_list:

#print(i)

try:

df = ak.stock_zh_a_hist(symbol=i, period="daily", start_date=star, end_date=end, adjust="")

df.rename(columns={"日期":'trade_date',"开盘":'open',"收盘":'close',"最高":'high',"最低":'low',"涨跌幅":'change'},inplace = True)

df = df.sort_index() #建立索引

df['ma10'] = df['close'].rolling(5).mean()

df['ma20'] = df['close'].rolling(10).mean()

#计算股票收益,有两种计算收益率方法:1.离散收益率 2.连续收益率

df['position'] = np.where(df['ma10'] > df['ma20'], 1, 0) #当20日均线大于60日均线时记录1,反之记录-1

df['returns'] = df['close']/df['close'].shift(1)-1 #连续收益率计算

#data['returns_dis'] = data['close']/data['close'].shift(1) - 1 #离散收益率计算

df['strategy'] = df['position'].shift(1)*df['returns']

df['trade_date']=pd.to_datetime(df.trade_date,format="%Y-%m-%d")

#print(df.head())

#df['code'] = i

#下面需将得到的收益ret序列变成按日期由低到高排列

#cum=df['strategy']+cum#等权重配置一篮子股票,计算权重和

last = pd.merge(df[['trade_date','strategy']],last,on='trade_date',how= 'left')

#last = last.set_index('trade_date')

#print(cum)

#print(last)

except:

continue

#(cum/len(stock_list)).cumsum().apply(np.exp).plot(figsize=(10, 6))

last = last.set_index('trade_date')

last = last.fillna(0)

last['Row_sum'] = last.apply(lambda x: x.sum(), axis=1)/len(stock_list)

last = last.reset_index()

last获取期货数据,并计算收益:

#获取股指期货数据

df3 = ak.futures_main_sina(symbol="IF0")

df3.rename(columns={"日期":'trade_date',"开盘价":'open',"收盘价":'close',"最高价":'high',"最低价":'low'},inplace = True)

df3.sort_index()

#df3.index=pd.to_datetime(df3.trade_date,format="%Y-%m-%d")

df3 = df3[(df3['trade_date']>=datetime.date(2017,1,17))&(df3['trade_date']<=datetime.date(2023,8,13))]

df3['returns'] = df3['close']/df3['close'].shift(1)-1 #连续收益率计算

#data['returns_dis'] = data['close']/data['close'].shift(1) - 1 #离散收益率计算

df3['returns'].cumsum()

df3.trade_date=pd.to_datetime(df3.trade_date,format="%Y-%m-%d")

df3计算组合收益:

la = pd.merge(last,df3,on='trade_date')

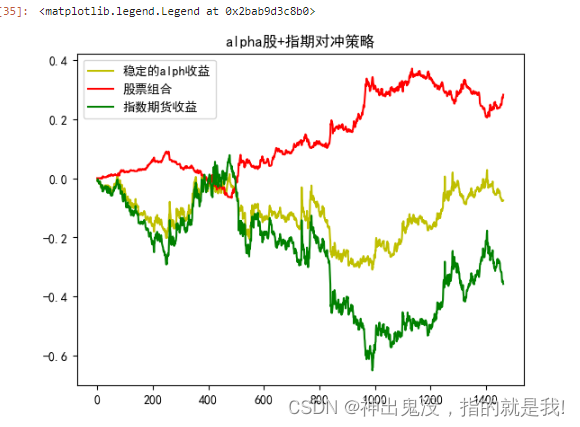

plt.plot(la.Row_sum.cumsum()-la.returns.cumsum(),label="稳定的alph收益",color="y")

plt.plot(la.Row_sum.cumsum(),label="股票组合",color='r')

plt.plot(-la.returns.cumsum(),label="指数期货收益",color='g')

plt.title("alpha股+指期对冲策略")

plt.legend()结果图:

9691

9691

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言