1. 书籍和文中所提到的数据会在文末提供百度云下载,所有数据都不会有加密,可以放心下载使用

2. 文中计算的结果与书中不同是由于数据使用的时间段不同

目录

1. 单期与多期简单收益率

在计算单个资产的收益率或者比较不同资产的收益率时,我们需要先确定资产的持有期间。单期指收益率计算的时间间隔是一期,这里的一期可以以天为单位,也可以以月、季度或者年为单位。多期是指时间跨度为2期或2期以上。

计算万科1期和2期收益率

import pandas as pd

import numpy as np

df = pd.read_csv('./000002.csv',encoding='utf-8')

df.head()

df['tradeDate'] = pd.to_datetime(df['tradeDate'])

df.sort_values(by='tradeDate',ascending=True,inplace=True)

df00 = df[df['tradeDate']>='2014-01-01']

df00 = df00.iloc[:311,:]

df00.head()

df00.set_index('tradeDate',inplace=True)

close = df00.closePrice

close.index.name='Date'

close.head()

# 将收盘价滞后一期

lagclose = close.shift(1)

lagclose.head()

# 合并close , lagclose 这两个收盘价数据

Calclose = pd.DataFrame({'close':close,'lagclose':lagclose})

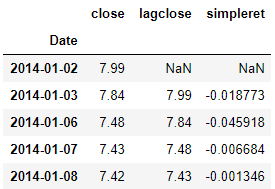

Calclose.head()

# 计算单期简单收益率

simpleret = (close-lagclose)/lagclose

simpleret.name = 'simpleret'

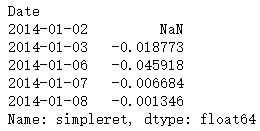

simpleret.head()

calret = pd.merge(Calclose,pd.DataFrame(simpleret),left_index=True,right_index=True)

calret.head()

# 计算2期简单收益率

simpleret2 = (close-close.shift(2))/close.shift(2)

simpleret2.name = 'simpleret2'

calret['simpleret2'] = simpleret2

calret.head()

# 查看1月9日的数据

calret.iloc[5,:]

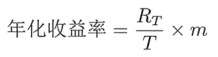

2. 年化收益率

年化收益率的计算与复利相关,假设投资人持有资产时间为T期,获得的(或将要获得的)收益率为RT, 一年一共有m个单期(比如以月为单期,一年有12个月),则该资产的年化收益率为:

或

# 假设一年有245个交易日

annualize = (1+simpleret).cumprod()[-1]**(245/311)-1

annualize

# out: 0.56606148743496413. 连续复利收益率

![]()

# 计算单期连续复利收益率

comporet = np.log(close/lagclose)

comporet.name = 'comporet'

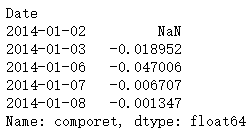

comporet.head()

comporet[5]

# out: 0.005376357036380496

4. 多期连续复利收益率

# 多期连续复利收益率

comporet2 = np.log(close/close.shift(2))

comporet2.name='comporet2'

comporet2.head()

comporet2[5]

# out: 0.0040295554860016425. 单期与多期连续复利收益率的关系

# 单期加总即得多期

comporet = comporet.dropna()

sumcomporet = comporet+comporet.shift(1)

sumcomporet.head()

6. 绘制收益图

simpleret.plot()

((1+simpleret).cumprod()-1).plot()

7. 资产风险的测度——方差

# 数据日期为2014年1月1日到2014年12月21日

# 600343 航天动力

# 600346 大橡塑

df_600343 = pd.read_csv('./600343.csv',encoding='utf-8')

df_600346 = pd.read_csv('./600346.csv',encoding='utf-8')

df_600343['tradeDate'] = pd.to_datetime(df_600343['tradeDate'])

df_600343.sort_values(by='tradeDate',ascending=True,inplace=True)

df_600343_00 = df_600343[(df_600343['tradeDate']>='2014-01-01') & (df_600343['tradeDate']<='2014-12-31')]

df_600343_00.set_index('tradeDate',inplace=True)

df_600346['tradeDate'] = pd.to_datetime(df_600346['tradeDate'])

df_600346.sort_values(by='tradeDate',ascending=True,inplace=True)

df_600346_00 = df_600346[(df_600346['tradeDate']>='2014-01-01') & (df_600346['tradeDate']<='2014-12-31')]

df_600346_00.set_index('tradeDate',inplace=True)

returnS = (df_600343_00['closePrice']-df_600343_00['closePrice'].shift(1))/df_600343_00['closePrice'].shift(1)

returnD = (df_600346_00['closePrice']-df_600346_00['closePrice'].shift(1))/df_600346_00['closePrice'].shift(1)

returnS.std()

# out: 0.04275196558069479

returnD.std()

# out: 0.020921776912917068. 资产风险的测度——下行风险

# 比较两只股票的下行风险

def cal_half_dev(returns):

mu = returns.mean()

temp = returns[returns<mu]

half_deviation=(sum((mu-temp)**2)/len(returns))**0.5

return (half_deviation)

cal_half_dev(returnS)

# out: 0.036604972076999705

cal_half_dev(returnD)

# out: 0.0140749478842890799. 资产风险的测度——风险价值

# 历史模拟法

returnS.quantile(0.05)

# out: -0.043239530438867156

returnD.quantile(0.05)

# out: -0.03457604701374094

# 协方差矩阵法

from scipy.stats import norm

norm.ppf(0.05,returnS.mean(),returnS.std())

# out: -0.06821340640140308

norm.ppf(0.05,returnD.mean(),returnD.std())

# out: -0.0337355404401935

10. 资产风险的测度——期望亏空

returnS[returnS<=returnS.quantile(0.05)].mean()

# out: -0.0337355404401935

returnD[returnD<=returnD.quantile(0.05)].mean()

# out: -0.04528445493770186

11. 资产风险的测度——最大回撤

# 最大回撤

valueS = (1+returnS).cumprod()

valueS_D = valueS.cummax()-valueS

valueS_d = valueS_D/(valueS_D + valueS)

MMD_S = valueS_D.max()

# 最大回撤

MMD_S

# out: 0.7353951890034371

# 最大回撤率

mmd_S = valueS_d.max()

mmd_S

# out: 0.5676392572944298PS:

书籍

链接:https://pan.baidu.com/s/1xJD85-LuaA9z-Jy_LU5nOw

提取码:ihsg

链接:https://pan.baidu.com/s/1tF2RVDrHWNeniCLoploUTg

提取码:1xmk

1019

1019

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言