本文所有代码基于windAPI,复现前先下载客户端并注册账号

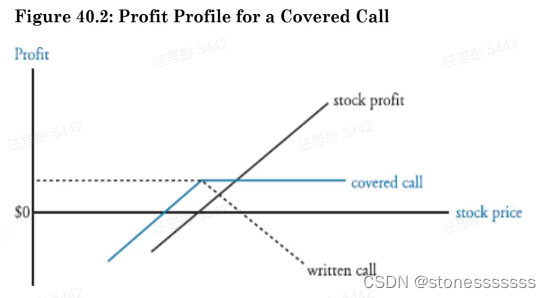

备兑看涨期权(Covered Call)

构成:标的资产的多头 + 欧式看涨期权空头

损益:当标的资产市场价格上涨时,标的资产多头获利,看涨期权空头不行权。

当标的资产价格下降时,标的资产多头亏损,看涨期权行权获利弥补多头方损失。

| 头寸 | 损益 |

|---|---|

| 标的资产多头 | S T − S 0 S_{T}-S_{0} ST−S0 |

| 看涨期权空头 | C − m a x ( S T − K , 0 ) C-max(S_{T}-K,0) C−max(ST−K,0) |

| 整体策略 | S T − S 0 − m a x ( S T − K , 0 ) + C S_{T}-S_{0}-max(S_{T}-K,0)+C ST−S0−max(ST−K,0)+C |

其中 S T S_{T} ST表示T时刻的市价,K表示执行价,C表示看涨期权价格。损益图如下所示。

代码实现:

def CoveredCall(UnderlyingCode, OptionCode,StartTime):

'''

UndelyingCode:标的资产代码

OptionCode:对冲期权的代码

StartTime:开始回测时间

'''

error_code, wsd_data = w.wsd(OptionCode, "exe_price,exe_enddate,close,exe_ratio", StartTime, StartTime, usedf=True)

StrikePrice = wsd_data['EXE_PRICE'][0]

StrikeTime = wsd_data['EXE_ENDDATE'][0]

OptionPrice = wsd_data['CLOSE'][0]

Ratio = wsd_data['EXE_RATIO'][0]

# 取当前系统时间

current_time = datetime.datetime.now()

# 比较行权日和当前,如果行权日晚于当前时间,只能回测到当前时间,否则可以回测到行权日。

if current_time > StrikeTime:

BacktestTime = StrikeTime

else:

BacktestTime = current_time

# 定义合约份数

N_ETF = 10000

N_option = 1

# 取行情数据

error_code, etf_data = w.wsd(UnderlyingCode, "close", StartTime, BacktestTime, usedf=True)

S0 = etf_data['CLOSE'][0]

Payoff = (etf_data - S0) * N_ETF + N_option * OptionPrice - np.max(etf_data - StrikePrice, 0) * Ratio

Payoff.plot(legend=None)

plt.xlabel('Time', fontsize=8)

plt.xticks(rotation=45)

plt.ylabel('Payoff', fontsize=8)

plt.show( 最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

876

876

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言