超级会员免费看

超级会员免费看

We're now going to go through the logic of how

the fixed rate on a plain vanilla swap is determined.

It also involves no-arbitrage logic,

but it's a little bit more complicated than what

we've done up to this point.

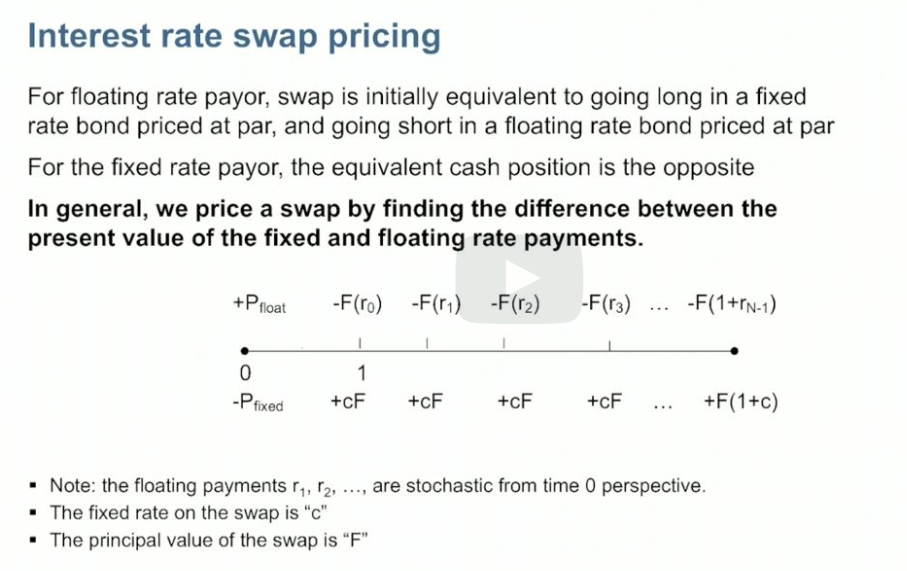

The diagram here represents the cash

flows in a swap from the perspective of the floating

rate payer.

Notice that the diagram is drawn as

if principal payments are exchanged, even though they're

not.

That is, the notional principal, denoted here by a capital F,

is assumed to be exchanged along with the final interest-based

payment at the final date, N. Th

订阅专栏 解锁全文

订阅专栏 解锁全文

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言